Is ATI's Expanded US$500 Million Buyback a Clear Signal on Capital Priorities and EPS Focus?

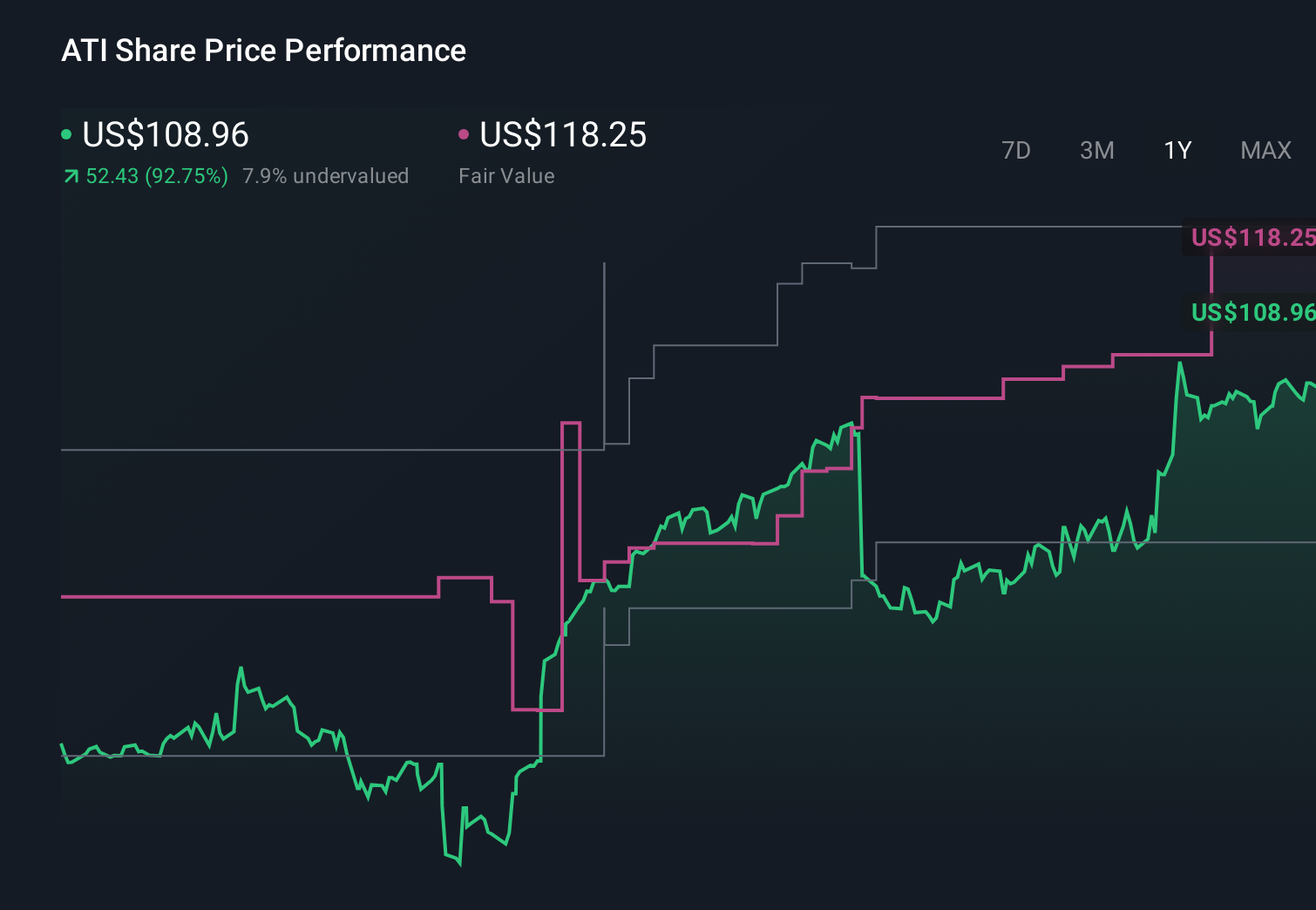

ATI Inc. ATI | 140.57 | +3.74% |

- ATI Inc. recently expanded its share repurchase program, with the board approving an additional US$500 million authorization that can be executed in the open market or through privately negotiated transactions without timing restrictions.

- This larger buyback pool, coming on top of prior repurchases that have already helped earnings per share grow faster than revenue, underscores management’s confidence in ATI’s long-term performance and capital return priorities.

- Next, we’ll examine how ATI’s expanded US$500 million share repurchase authorization could influence its investment narrative and longer-term earnings profile.

AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

ATI Investment Narrative Recap

To own ATI, you have to believe its specialty materials will stay essential for aerospace and other high-performance uses, and that management will keep converting that demand into solid earnings. The expanded US$500 million buyback may support earnings per share in the near term, but it does not change the key near-term catalyst, which is execution on existing aerospace and defense contracts, or the biggest risk, which remains exposure to weaker non-aerospace end markets and concentrated aerospace customers.

The buyback expansion sits alongside ATI’s recent long-term contract wins with Boeing and Airbus, which underpin volume and pricing for its titanium and nickel products. Those contracts are central to the stock’s catalyst story, because they tie directly into utilization of ATI’s upgraded capacity and its ability to sustain higher margins, while the larger repurchase authorization mainly affects how much of those earnings accrue on a per-share basis.

Yet, against this positive setup, ATI’s reliance on a concentrated group of large aerospace OEMs is a risk investors should be aware of if...

ATI's narrative projects $5.5 billion revenue and $635.6 million earnings by 2028.

Uncover how ATI's forecasts yield a $145.62 fair value, in line with its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already penciling in ATI earnings of about US$740 million by 2028, and the expanded buyback could either reinforce or challenge that view, depending on how you weigh those growth assumptions against the risk that heavy capital needs might pressure free cash flow if end markets soften.

Explore 5 other fair value estimates on ATI - why the stock might be worth less than half the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your ATI research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free ATI research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ATI's overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- This technology could replace computers: discover 24 stocks that are working to make quantum computing a reality.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 87 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.