Is Booz Allen Hamilton (BAH) Still Attractive After Recent Share Price Weakness?

Booz Allen Hamilton Holding Corporation Class A BAH | 0.00 |

- Wondering if Booz Allen Hamilton Holding is priced attractively or if the value story has already played out? This breakdown focuses squarely on what you are paying versus what you might be getting.

- The stock last closed at US$80.01, with the share price down 1.3% over the past week, up 4.9% over the past month, and down 5.7% year to date and 19.7% over the last year.

- Recent coverage of Booz Allen Hamilton has focused on its position as a major government and commercial consulting contractor, including contracts and programs that keep it closely tied to long term defense and technology spending. These themes help frame how investors are reassessing both the risks and the potential resilience behind those recent price moves.

- Booz Allen Hamilton currently scores a 5 out of 6 valuation score, which points to several areas where the stock screens as undervalued. The next sections will unpack how different valuation methods arrive at that view, while also pointing to an even deeper way to think about value at the end of the article.

Approach 1: Booz Allen Hamilton Holding Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a stock could be worth by projecting its future cash flows and discounting them back to today’s dollars, then comparing that value to the current share price.

For Booz Allen Hamilton Holding, the model uses a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The company’s last twelve month Free Cash Flow is about $956.5 million. Analyst and extrapolated projections suggest Free Cash Flow stays in the hundreds of millions over the coming decade, with Simply Wall St extending estimates beyond the analyst window. For example, projected Free Cash Flow for 2029 is $979.05 million, and by 2035 the extrapolated figure used in the model is $1.09b, all in $.

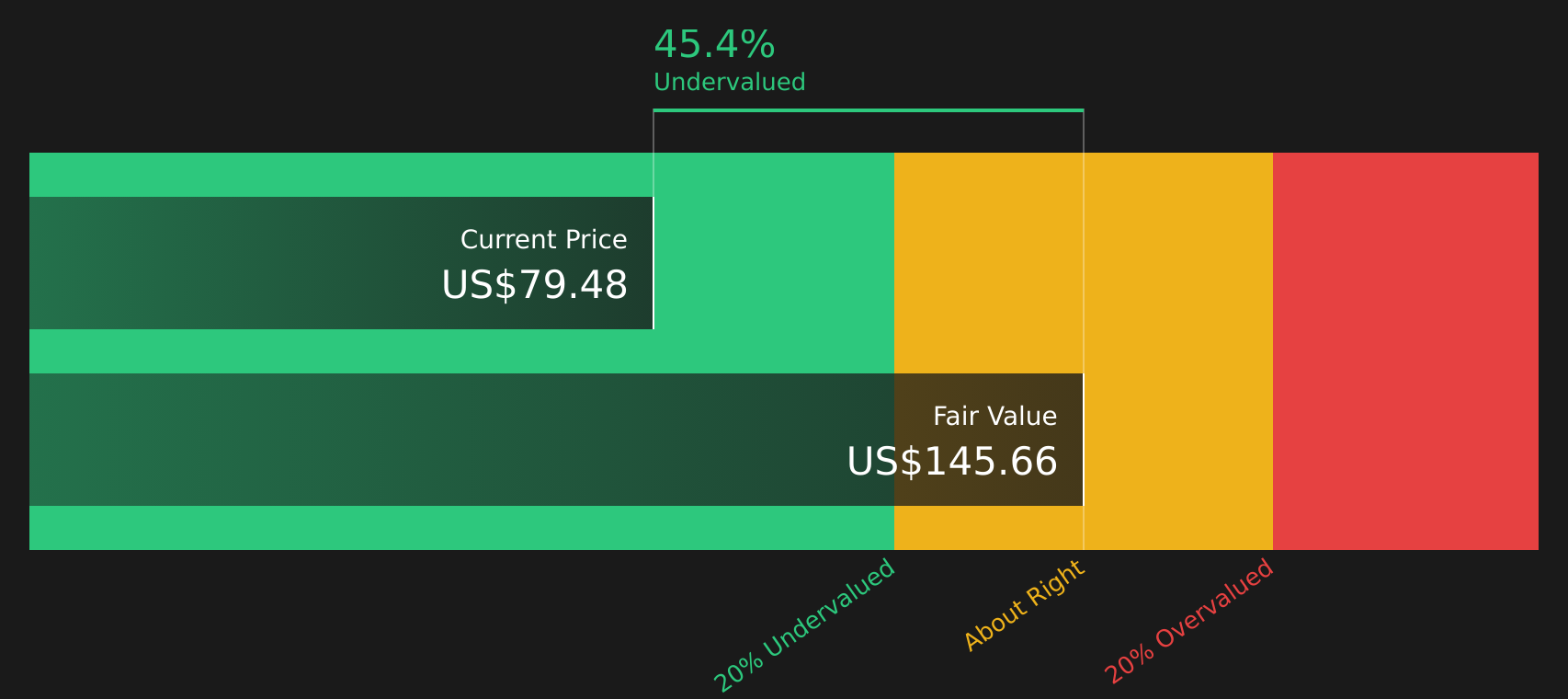

When all those projected cash flows are discounted back, the DCF model arrives at an estimated intrinsic value of about $145.60 per share. Compared with the recent share price of $80.01, this indicates the stock screens as roughly 45.0% undervalued under these assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Booz Allen Hamilton Holding is undervalued by 45.0%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Approach 2: Booz Allen Hamilton Holding Price vs Earnings

For profitable companies, the P/E ratio is a useful shortcut because it links what you pay per share directly to the earnings the business is already generating. It helps you see how many dollars investors are willing to pay today for each dollar of current earnings.

What counts as a “normal” P/E depends on how fast earnings are expected to grow and how risky those earnings are. Higher expected growth and lower perceived risk usually justify a higher multiple, while slower growth or higher risk often come with a lower one.

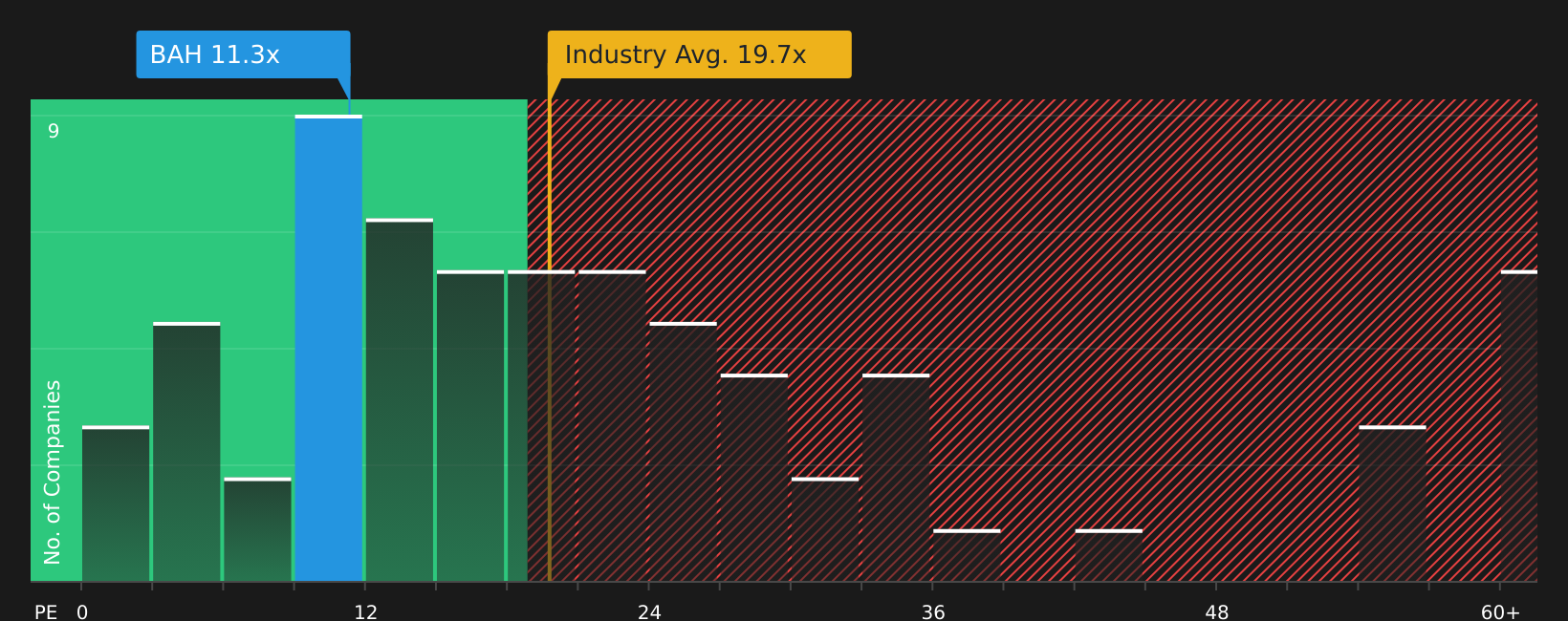

Booz Allen Hamilton Holding currently trades on a P/E of 11.34x. That sits below the Professional Services industry average P/E of 19.26x and also below the peer average of 20.20x. Simply Wall St’s Fair Ratio for the stock is 16.00x, which is an estimate of what a suitable P/E might be once factors such as earnings growth, profit margins, industry, market cap and risk profile are all considered.

This Fair Ratio approach offers a more tailored yardstick than a simple comparison with industry or peer averages, because it adjusts for the company’s own characteristics rather than assuming all stocks deserve the same multiple.

Comparing the current P/E of 11.34x with the Fair Ratio of 16.00x suggests the stock screens as undervalued on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 21 top founder-led companies.

Upgrade Your Decision Making: Choose your Booz Allen Hamilton Holding Narrative

Earlier it was mentioned that there is an even better way to think about valuation, and that is where Narratives come in. Narratives let you connect your view of Booz Allen Hamilton Holding’s story to a set of revenue, earnings and margin assumptions, which then translate into a Fair Value that you can compare directly with today’s price. On Simply Wall St’s Community page, Narratives are an easy tool to use, available to millions of investors, and they update automatically when fresh information such as earnings reports or contract news is added. This means your story and Fair Value stay aligned with the latest data. For Booz Allen Hamilton Holding, one investor might lean toward a cautious Narrative that lines up with a Fair Value around US$74.00, while another might prefer a more optimistic Narrative closer to US$140.29. A third may sit near the consensus view at about US$97.83, which shows how the same stock can support very different but clearly quantified stories.

For Booz Allen Hamilton Holding however, we will make it really easy for you with previews of two leading Booz Allen Hamilton Holding Narratives:

Think of these as bookend views around the current price so you can see which story feels closer to your own expectations and risk tolerance.

Fair Value: US$140.29

Implied discount to this Fair Value versus the latest close of US$80.01: about 43.0% undervalued.

Revenue growth assumption in this bullish view: 6.26% a year.

- Bullish analysts tie a Fair Value of about US$140.29 to Booz Allen Hamilton Holding by assuming revenue of US$13.7b and earnings of US$792.1m by 2029, followed by a P/E of 24.8x on those earnings, using an 8.2% discount rate.

- The story leans heavily on VoLT execution, deep federal relationships, a US$38b backlog and commercial tech partnerships to support ongoing contract wins in areas such as cyber, AI and space.

- Key watchpoints in this view are Booz Allen Hamilton Holding's reliance on U.S. government budgets, potential pressure from automation and AI on traditional consulting work and the need to keep pace with new technologies to protect margins.

Fair Value: US$74.00

Implied premium to this Fair Value versus the latest close of US$80.01: about 7.5% overvalued.

Revenue growth assumption in this cautious view: 2.07% a year.

- The bearish cohort anchors on a Fair Value of about US$74.00, which assumes revenue of US$11.9b and earnings of US$764.2m by 2029, with the stock on a P/E of 13.5x and an 8.2% discount rate.

- This narrative is more focused on the risk that automation, tighter U.S. federal budgets, outcome based contracts and heavier compliance costs compress margins and make earnings less predictable.

- Even here, the analysis still allows for growth in AI, cyber and defense related work, but treats these positives as offsets against contract concentration risk and the possibility that Booz Allen Hamilton Holding earns a lower valuation multiple over time.

Seeing both ends of the range side by side makes it easier to decide which assumptions feel more realistic and how much upside or downside you are comfortable underwriting at the current price.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Booz Allen Hamilton Holding on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Booz Allen Hamilton Holding? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.