Is Carnival (CCL) Quietly Rewiring Its Profit Mix Around Onboard Retail And Lower Fuel Costs?

Carnival Corporation Ltd. CCL | 0.00 |

- Earlier this year, Global Travel Retail Holdings’ Starboard announced a collaboration with Carnival Cruise Line and Diageo to offer a limited-edition, single-barrel Bulleit Bourbon, priced at US$59.99 and sold exclusively in retail stores across 14 Carnival ships as part of America’s 250th anniversary celebrations.

- This partnership highlights how Carnival is using exclusive onboard products and branded experiences to deepen guest engagement and enhance higher-margin retail spending at sea.

- We’ll now examine how easing fuel-cost pressures after the Strait of Hormuz peace deal may influence Carnival’s existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Carnival Investment Narrative Recap

Carnival’s investment case still hinges on steady demand for cruise vacations, improving onboard monetization, and disciplined balance sheet repair. The Strait of Hormuz peace deal primarily affects the short term by easing fuel cost fears, which is supportive for margins but does not change the core story. The largest near term risk remains Carnival’s high debt load, which continues to limit financial flexibility even as investors focus on fuel and geopolitical headlines.

Among recent updates, the board’s authorization of up to US$2,500,000,000 in share repurchases stands out beside easing fuel pressures. For existing shareholders, buybacks can magnify the impact of any improvement in earnings per share, but they also raise questions about how management balances cash returns against debt reduction and ongoing fleet investment. Together, these moves sit at the heart of the current catalyst debate around Carnival.

Yet beneath the optimism on fuel and buybacks, investors should also be aware that Carnival’s elevated debt and refinancing needs could...

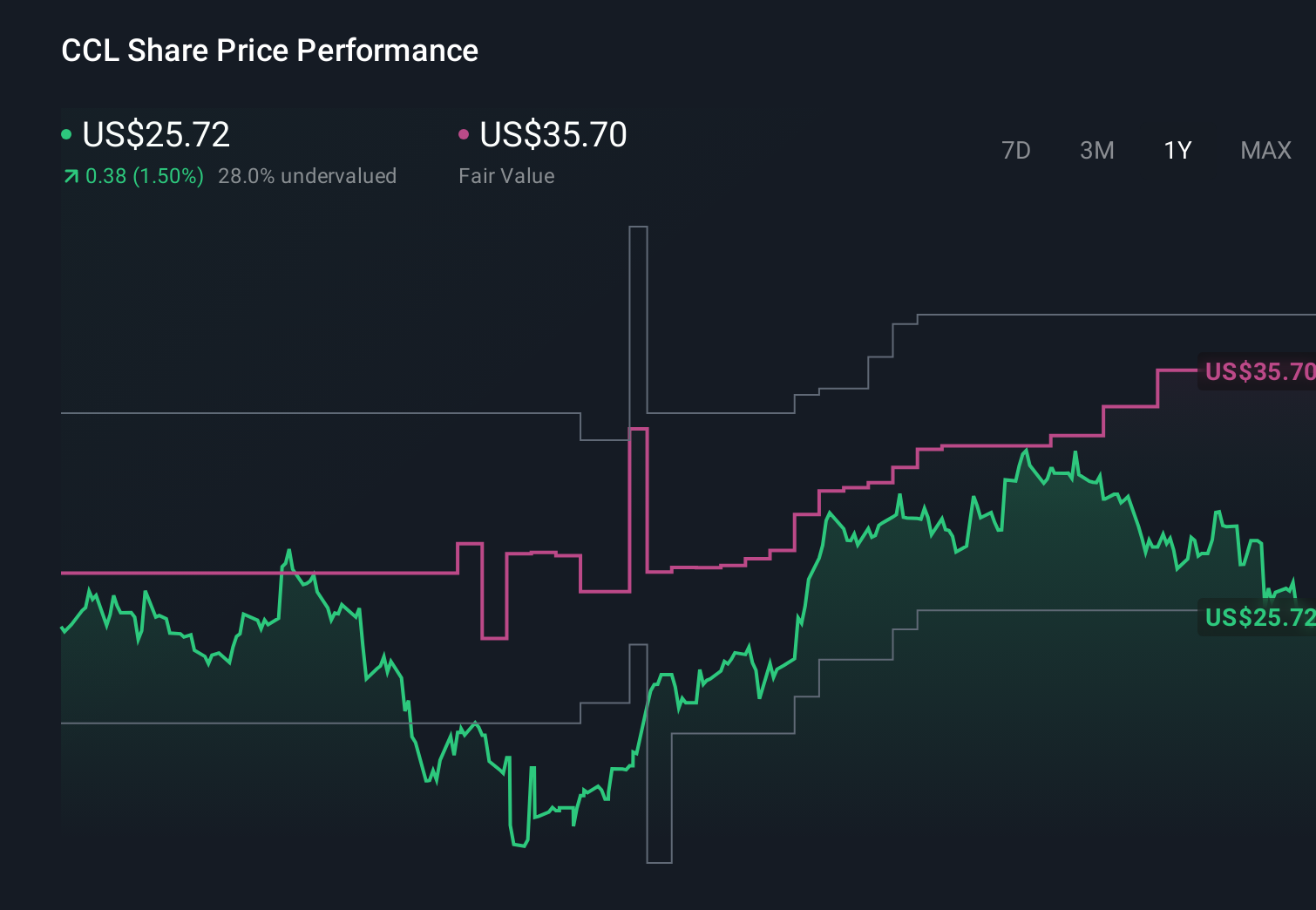

Carnival's narrative projects $29.0 billion revenue and $3.7 billion earnings by 2028. This requires 3.8% yearly revenue growth and a $1.2 billion earnings increase from $2.5 billion today.

Uncover how Carnival's forecasts yield a $37.70 fair value, a 26% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already penciling in about US$31,000,000,000 of revenue and US$4,400,000,000 of earnings by 2029, which is far more upbeat than consensus on both growth and margin potential. That view leans heavily on faster deleveraging and stronger structural earnings, while the recent fuel and geopolitical news may either support or challenge those assumptions once it is fully reflected in forecasts.

Explore 10 other fair value estimates on Carnival - why the stock might be worth as much as 73% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Carnival research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Carnival research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carnival's overall financial health at a glance.

Ready For A Different Approach?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.