Is Citigroup’s (C) Latest Capital Moves Quietly Redefining Its Simplification Story?

Citigroup Inc. C | 131.94 | +1.82% |

- In recent days, Citigroup issued new long-dated zero-coupon senior unsecured notes due April 2056, completed a US$50,000,000 senior note offering, and declared quarterly dividends on both its common and multiple series of preferred stock, all following a period of strong operating execution and corporate activity.

- These funding moves, leadership changes in its Australasian natural resources franchise, and continued use of AI to streamline operations underscore how Citigroup is aligning its balance sheet, talent, and technology with its ongoing transformation plan.

- We’ll now examine how Citigroup’s renewed capital raising and dividend decisions influence its existing investment narrative built around simplification.

Find 58 companies with promising cash flow potential yet trading below their fair value.

Citigroup Investment Narrative Recap

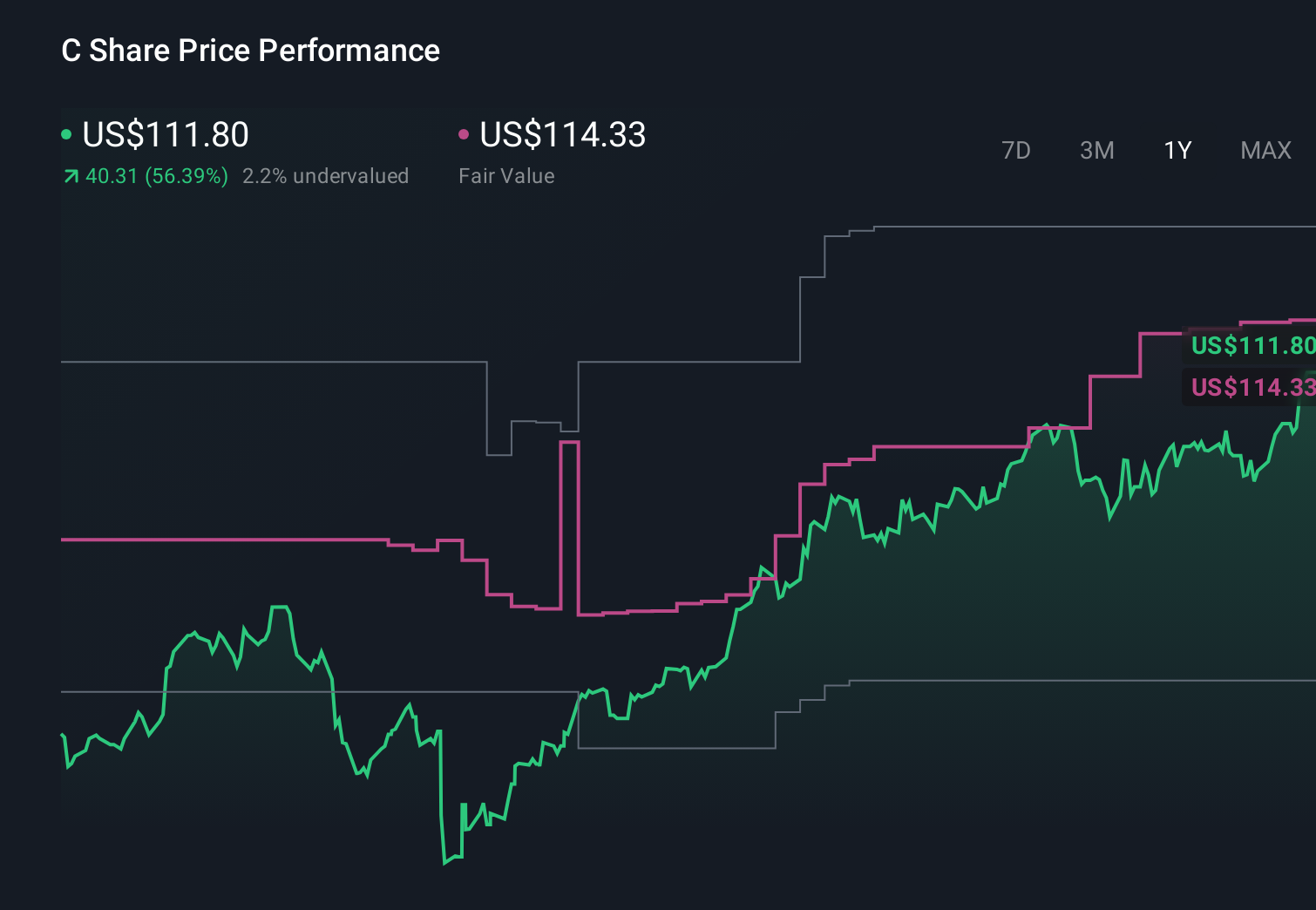

To own Citigroup, you need to believe its simplification plan can translate record 2025 execution and a sharp share-price re‑rating into steadier returns on tangible equity, even as revenue growth expectations remain modest. The most important near term catalyst is whether earnings can support both ongoing buybacks and the current dividend. The biggest risk remains high, variable transformation and regulatory costs. The latest funding and dividend moves do not materially change that near term risk reward balance.

Among the latest developments, Citi’s decision to issue long dated zero coupon senior unsecured notes due 2056 and complete a US$50,000,000 4.00% senior note offering sits squarely in this capital story. These actions add to its funding flexibility while it continues heavy spending on technology and AI and maintains a US$0.60 common dividend. For investors watching catalysts, the question is how this additional funding interacts with future buybacks and expense control.

But against this progress, investors also need to be aware of the risk that elevated transformation costs and regulatory demands could still...

Citigroup's narrative projects $88.8 billion revenue and $17.2 billion earnings by 2028. This requires 6.8% yearly revenue growth and a $4.3 billion earnings increase from $12.9 billion today.

Uncover how Citigroup's forecasts yield a $134.32 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Some of the most cautious analysts, who were assuming earnings of about US$18.9 billion by 2029 and a lower 10.8x PE, see heavy macro and expense pressures as offsetting benefits from Citi’s automation push, so you should weigh these more pessimistic expectations against the recent funding and dividend news and consider how your own view might change as new information emerges.

Explore 11 other fair value estimates on Citigroup - why the stock might be worth 9% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Citigroup research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Citigroup research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Citigroup's overall financial health at a glance.

Looking For Alternative Opportunities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Rare earth metals are the new gold rush. Find out which 27 stocks are leading the charge.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.