Is Coterra Energy an Opportunity After a 10.5% Drop in 2025?

Coterra Energy CTRA | 0.00 |

- Ever wondered if Coterra Energy is trading at a bargain, or if the market knows something you don't? You're in the right place to find out what is really driving its value.

- After a solid 83.8% gain over the last five years, the stock has cooled off recently, down 1.4% in the past week and 10.5% year-to-date. This illustrates how quickly sentiment and risk perceptions can shift.

- Recent headlines about shifting global energy demand and volatility in commodity prices have fueled both optimism and caution around oil and gas producers. Coterra has been especially visible as analysts weigh in on its capital spending strategy and the broader outlook for natural gas markets.

- On our proprietary valuation checks, Coterra Energy scores an impressive 6 out of 6, suggesting strong all-round value. However, as we explore different valuation approaches in a moment, you will see why the real story might be even more nuanced by the end of this article.

Approach 1: Coterra Energy Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company’s value by projecting its future cash flows and discounting them back to today’s value using a required rate of return. This approach helps investors gauge whether a stock's market price reflects its potential to generate cash over time.

For Coterra Energy, the most recent reported Free Cash Flow stands at $1.50 Billion. Analysts provide detailed cash flow forecasts out to 2029, with projected Free Cash Flow rising to $2.60 Billion by that year. Over the full 10-year model horizon, which includes both analyst forecasts and methodical extrapolations, the company’s cash flows remain strong and show healthy growth. The pace moderates in later years as projections move beyond analyst coverage and rely on broader industry assumptions.

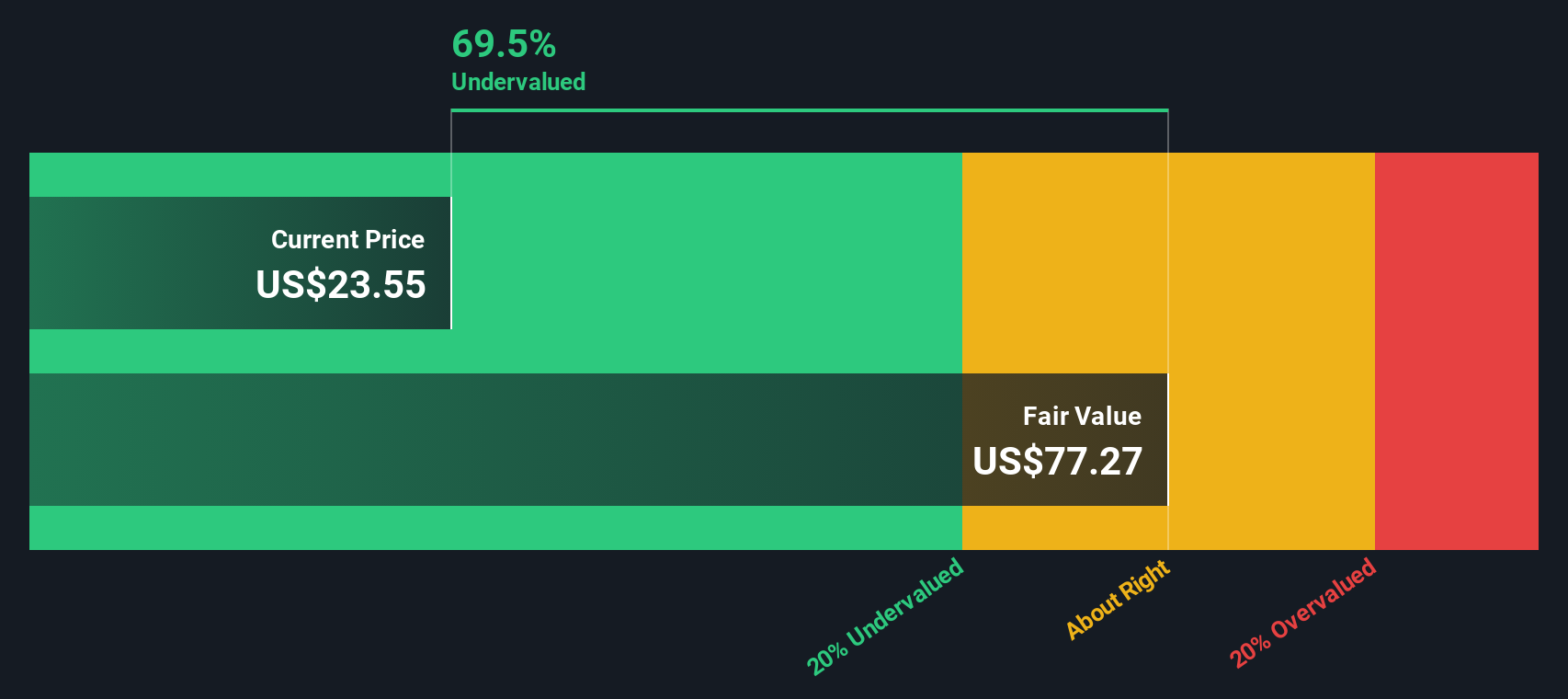

According to this DCF model, Coterra’s intrinsic value is estimated at $65.90 per share. This implies the stock is trading at a 64.5% discount to its calculated fair value, suggesting that it is significantly undervalued based on projected future cash generation.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Coterra Energy is undervalued by 64.5%. Track this in your watchlist or portfolio, or discover 838 more undervalued stocks based on cash flows.

Approach 2: Coterra Energy Price vs Earnings

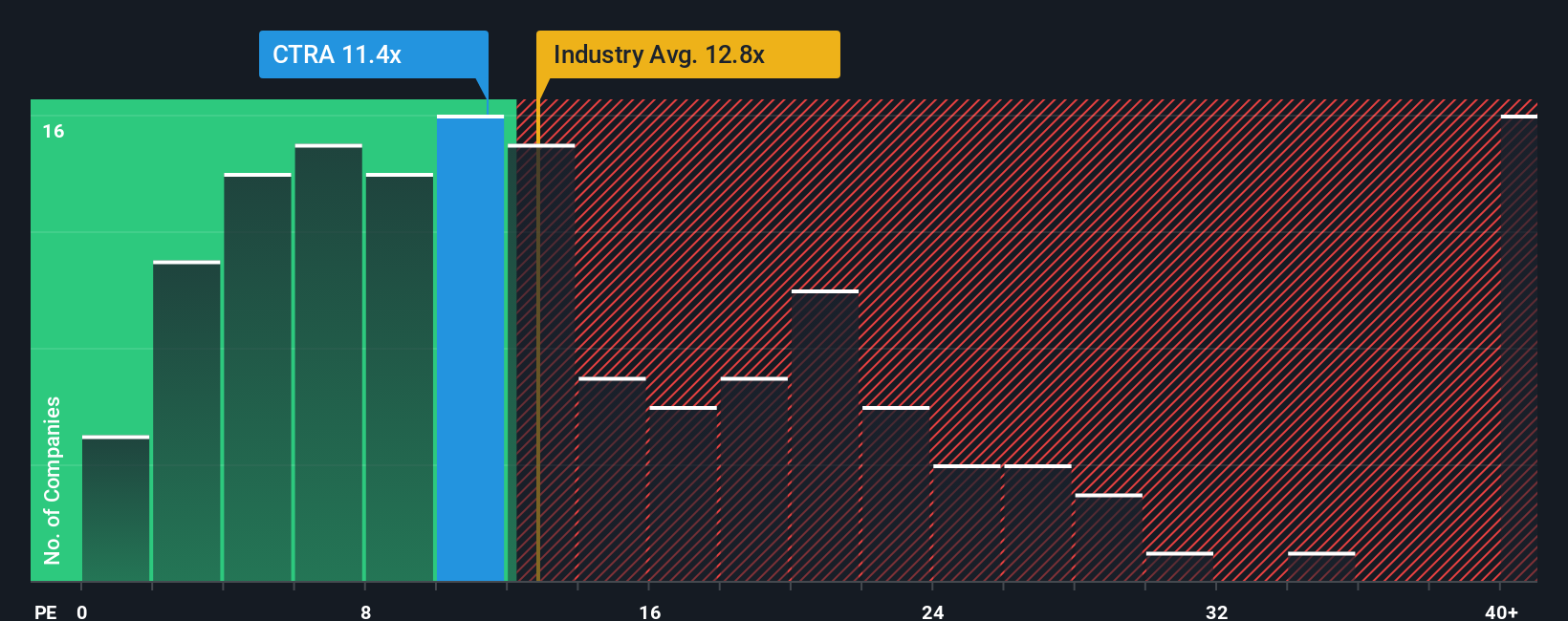

The Price-to-Earnings (PE) ratio is a widely used valuation gauge for profitable companies like Coterra Energy. It helps investors assess how much the market is willing to pay for a dollar of earnings. Since earnings influence long-term shareholder returns, the PE ratio is especially useful for comparing companies within the same industry or across the broader market.

A company's fair PE ratio depends on more than just profits. Growth expectations play a significant role; faster-growing companies often command higher multiples, while uncertainties or heightened risk can result in lower valuations. Stable profit margins and larger market capitalizations also tend to increase what is considered a “normal” or “fair” PE.

Coterra Energy is currently trading on an 11.33x PE multiple. This is below the Oil and Gas industry average of 12.59x and also comfortably under the peer group average of 16.72x. To provide a fuller picture, Simply Wall St calculates a proprietary "Fair Ratio" for each company that blends key factors such as expected earnings growth, industry trends, company size, profit margins, and risk. For Coterra, the Fair Ratio is 18.33x, indicating the stock is valued well below what would be expected given its underlying fundamentals.

By using the Fair Ratio, investors gain a more tailored sense of value rather than relying solely on industry or peer averages. This approach adjusts for the nuances that make Coterra unique, capturing both upside growth and risk factors in a way that broad benchmarks cannot.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1391 companies where insiders are betting big on explosive growth.

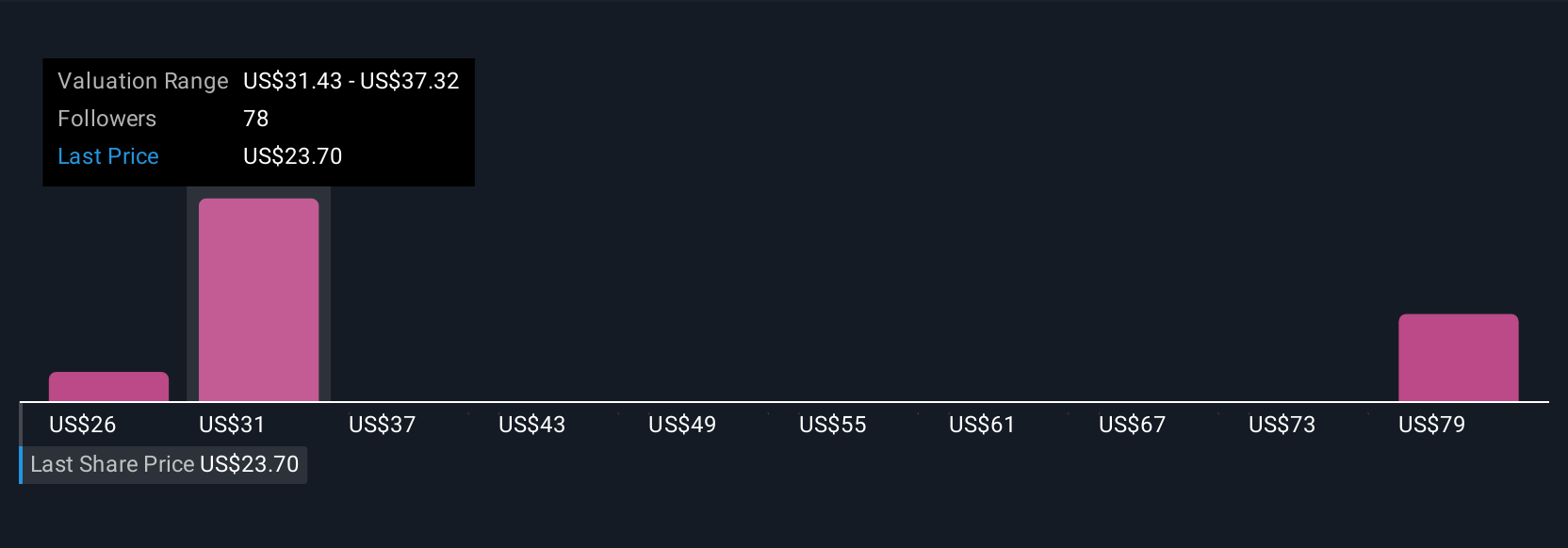

Upgrade Your Decision Making: Choose your Coterra Energy Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is a practical way for investors to tie together their view of a company's story, like Coterra's growth drivers or risks, with their forecasts for future revenue, earnings, and profit margins. This approach ultimately helps determine what they believe to be a fair value for the stock.

Narratives connect the dots between "what's happening at the company" and "what the numbers mean," allowing you to set your own assumptions and see the financial impact. On the Simply Wall St platform, Narratives are easy for anyone to create or follow within the Community page, empowering millions of users to document their perspectives and update them as news or earnings releases come in.

With Narratives, you can quickly see if your Fair Value signals a buy, hold, or sell opportunity compared to today's Price. Because these are updated dynamically with new information, they help you make timely, better-informed decisions.

For example, one investor might build a Narrative assuming robust LNG-driven revenue growth and land at a Fair Value of $40. Another investor, more cautious on gas prices and regulatory risks, may set their Fair Value closer to $25. This demonstrates how your story shapes your strategy.

Do you think there's more to the story for Coterra Energy? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.