هل تُوازن شركة دلتا (DAL) بين حقوق المساهمين واستراتيجية الأقساط المميزة وسط الاضطرابات وارتفاع التكاليف؟

دلتا إيرلينز DAL | 0.00 |

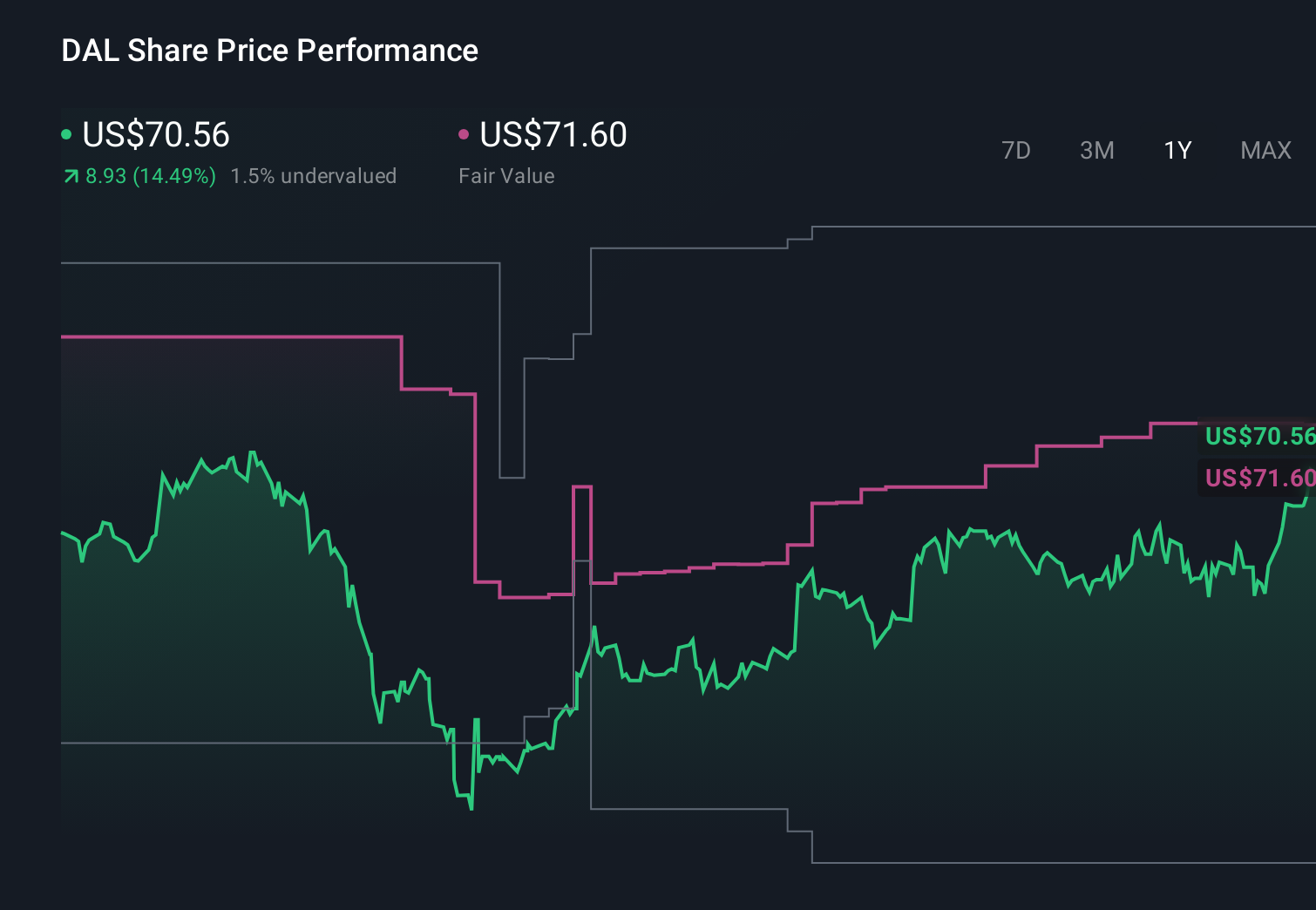

- في أواخر أبريل 2026، واجهت شركة دلتا إير لاينز نشاطًا من جانب المساهمين حيث تم تقديم مقترحات لإدخال حقوق التصويت التراكمي وحقوق الموافقة الكتابية، في حين حثت الشركة المستثمرين على التصويت ضد هذه التغييرات في الحوكمة في توكيلها النهائي قبل الاجتماع السنوي المقرر عقده في 18 يونيو 2026، كما أعلنت أيضًا عن توزيع أرباح ربع سنوية قدرها 0.19 دولار أمريكي للسهم الواحد تُدفع في 4 يونيو 2026.

- في الوقت نفسه، واجهت شركة دلتا إلغاءات واسعة النطاق للرحلات الجوية، وارتفاع تكاليف وقود الطائرات، وتقليص الخدمات على الطرق القصيرة، مما يسلط الضوء على الضغط الواقع على عملياتها وتجربة عملائها.

- سندرس الآن كيف تتقاطع الاضطرابات التشغيلية الأخيرة لشركة دلتا وخطوات خفض التكاليف مع سردها الاستثماري الحالي حول الطلب المتميز.

اكتشف الفرصة الكبيرة القادمة مع 24 سهمًا رخيصًا من النخبة، والتي توازن بين المخاطرة والعائد.

ملخص سرد استثمار شركة دلتا إيرلاينز

لامتلاك أسهم دلتا اليوم، يجب أن تؤمن بقدرة أعمالها المتميزة في مجال خدمات الدرجة الأولى والولاء والرحلات الدولية على تعويض الضغوط الناجمة عن ضعف الطلب المحلي، وارتفاع تكاليف وقود الطائرات، والاضطرابات التشغيلية. ويتمثل العامل الحاسم على المدى القريب في قدرة دلتا على استعادة موثوقية رحلاتها والحفاظ على ولاء عملائها المميزين بعد عمليات الإلغاء الأخيرة وتخفيض الخدمات. ويكمن الخطر الأكبر حاليًا في أن يؤدي التضخم المستمر في التكاليف والاضطرابات إلى تآكل هوامش الربح بوتيرة أسرع مما تستطيع استراتيجيتها في مجال خدمات الدرجة الأولى تحمله. وتؤثر آخر الأخبار بشكل مباشر على كلا الجانبين.

يُمثل القرار الأخير بإلغاء الوجبات الخفيفة والمشروبات المجانية على الرحلات التي تقل مسافتها عن 350 ميلاً لمعظم الدرجات، مع الإبقاء على خدمة الدرجة الأولى دون تغيير، نقطة التقاء في هذا التوتر. قد يُساهم هذا القرار في ضبط التكاليف وحماية التدفق النقدي الحر، ولكنه يختبر أيضاً مدى قدرة دلتا على الاعتماد على خفض التكاليف قبل أن تبدأ في تقويض مكانتها المتميزة القائمة على الخدمة، والتي يعوّل عليها العديد من المساهمين.

لكن وراء قصة التميز والأرباح الموزعة، يكمن خطر حقيقي يتمثل في أن المشكلات التشغيلية المستمرة وارتفاع تكاليف الوقود قد تعيد تشكيل هوامش ربح دلتا بهدوء بطرق يجب على المستثمرين أن يكونوا على دراية بها...

تتوقع شركة دلتا إيرلاينز تحقيق إيرادات بقيمة 72.9 مليار دولار وأرباح بقيمة 5.5 مليار دولار بحلول عام 2029. ويتطلب ذلك نموًا سنويًا في الإيرادات بنسبة 4.8٪ وزيادة في الأرباح بمقدار 0.5 مليار دولار من 5.0 مليار دولار اليوم.

اكتشف كيف أن توقعات شركة دلتا إيرلاينز تُنتج قيمة عادلة قدرها 79.89 دولارًا ، أي بزيادة قدرها 9٪ عن سعرها الحالي.

استكشاف وجهات نظر أخرى

كان بعض المحللين ذوي التصنيف الأدنى حذرين بالفعل، حيث افترضوا إيرادات تبلغ حوالي 66.7 مليار دولار أمريكي وأرباحًا تقارب 5.2 مليار دولار أمريكي بحلول عام 2029، ويركزون بشكل كبير على ارتفاع تكاليف الوحدة غير المتعلقة بالوقود، وهو ما قد يبدو أكثر إثارة للقلق في ضوء اضطرابات الرحلات الجوية الأخيرة لشركة دلتا وتخفيضات الخدمات.

استكشف 10 تقديرات أخرى للقيمة العادلة لأسهم شركة دلتا إيرلاينز - لماذا قد تصل قيمة السهم إلى 47% أكثر من السعر الحالي!

كوّن رأيك الخاص

هل تختلف مع الروايات السائدة؟ نادراً ما تأتي عوائد الاستثمار الاستثنائية من اتباع القطيع، لذا اتبع حدسك.

- تُعد تحليلاتنا التي تسلط الضوء على 3 مكافآت رئيسية وعلامتين تحذيريتين مهمتين قد تؤثران على قرارك الاستثماري نقطة انطلاق رائعة لأبحاثك حول شركة دلتا إيرلاينز.

- يقدم تقريرنا البحثي المجاني عن شركة دلتا إيرلاينز تحليلاً أساسياً شاملاً مُلخصاً في رسم بياني واحد - ندفة الثلج - مما يسهل تقييم الوضع المالي العام لشركة دلتا إيرلاينز بنظرة سريعة.

هل تبحث عن استثمارات أخرى؟

بدأ المستثمرون الأوائل يلاحظون ذلك بالفعل. تعرف على الأسهم التي يستهدفونها قبل أن تغادر السوق:

- استكشف 26 شركة رائدة في مجال الحوسبة الكمومية تقود ثورة تكنولوجيا الجيل القادم وتشكل المستقبل من خلال تحقيق اختراقات في الخوارزميات الكمومية، والبتات الكمومية فائقة التوصيل، والأبحاث المتطورة.

- المعادن الأرضية النادرة هي بمثابة حمى الذهب الجديدة. اكتشف أي 31 سهماً تقود هذا التوجه .

- استثمر في النهضة النووية من خلال قائمتنا التي تضم 91 مشروعاً رائداً في مجال البنية التحتية للطاقة النووية، والتي تدعم ثورة الذكاء الاصطناعي العالمية.

هذا المقال من Simply Wall St ذو طبيعة عامة. نقدم تعليقاتنا بناءً على البيانات التاريخية وتوقعات المحللين فقط، باستخدام منهجية محايدة، ولا يُقصد بمقالاتنا أن تكون نصائح مالية. لا يُشكل هذا المقال توصيةً بشراء أو بيع أي سهم، ولا يأخذ في الاعتبار أهدافك أو وضعك المالي. نهدف إلى تزويدك بتحليلات طويلة الأجل مدفوعة بالبيانات الأساسية. يُرجى ملاحظة أن تحليلنا قد لا يأخذ في الاعتبار آخر إعلانات الشركات الحساسة للسعر أو المعلومات النوعية. لا تمتلك Simply Wall St أي أسهم في أي من الشركات المذكورة.