Is Embedding Climate Analytics Into Broking Workflows Altering The Investment Case For Willis Towers Watson (WTW)?

Willis Towers Watson WTW | 0.00 |

- On 15 June 2026, Willis, a WTW business, launched an enhanced version of its Climate Diagnostic model within the Risk IQ platform to help risk managers and brokers quantify climate-driven risks such as floods and windstorms across global asset portfolios and supply chains.

- A key insight is that Climate Diagnostic is now embedded directly into WTW’s broking and risk engineering workflows, turning climate hazard analytics into an operational tool that can influence day-to-day risk transfer and adaptation decisions for clients.

- We’ll now examine how integrating Climate Diagnostic’s forward-looking climate hazard analytics into core broking workflows could influence Willis Towers Watson’s investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 15 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Willis Towers Watson Investment Narrative Recap

To own Willis Towers Watson, you need to believe in its ability to use data and technology to keep advisory and broking services differentiated in a competitive, fee-sensitive market. The enhanced Climate Diagnostic tool looks directionally helpful for reinforcing that differentiation in property risk and climate analytics, but it does not materially change the most immediate catalysts around execution on earnings growth and the key risk of service commoditization from broader AI and automation.

The recent launch of WTW’s AI workforce transformation solution on 2 June 2026 is especially relevant here, because it underlines how the firm is positioning technology at the core of its consulting and risk solutions. Taken together with Climate Diagnostic’s integration into broking workflows, these product moves may influence how investors think about WTW’s ability to defend pricing and maintain revenue quality if automation pressure in insurance broking accelerates.

Yet while these tools can strengthen WTW’s value proposition, investors should still be aware of the risk that accelerating AI adoption could...

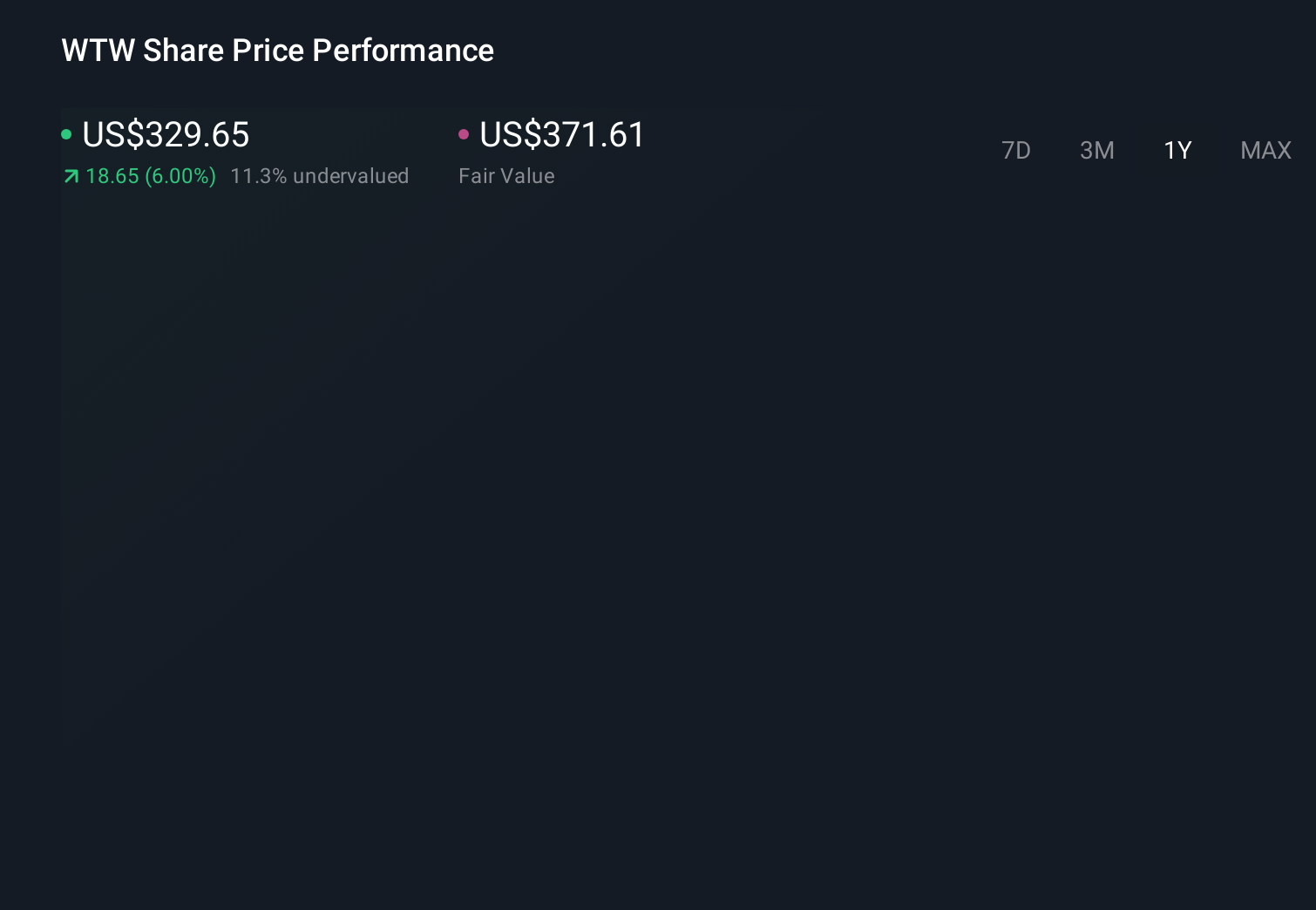

Willis Towers Watson's narrative projects $11.8 billion revenue and $1.9 billion earnings by 2029. This requires 6.1% yearly revenue growth and about a $0.2 billion earnings increase from $1.7 billion today.

Uncover how Willis Towers Watson's forecasts yield a $334.32 fair value, a 26% upside to its current price.

Exploring Other Perspectives

Two members of the Simply Wall St Community currently see WTW’s fair value between US$334 and US$446 per share, underlining how far opinions can differ. Against that wide range, the key question is whether technology led offerings like Climate Diagnostic really help WTW resist fee compression, which could have important implications for how its earnings profile evolves over time.

Explore 2 other fair value estimates on Willis Towers Watson - why the stock might be worth as much as 68% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Willis Towers Watson research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Willis Towers Watson research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Willis Towers Watson's overall financial health at a glance.

Curious About Other Options?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Capitalize on the AI infrastructure supercycle with our selection of the 51 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.