Is Entravision Communications (EVC) Fully Valued Following Its Russell Index Removal?

Entravision Communications Corporation Class A EVC | 0.00 |

Index removal brings Entravision Communications into focus

Entravision Communications (EVC) was recently removed from several Russell value indices, including the Russell 2000 Value and Russell 3000 Value benchmarks. This type of event can influence fund flows and trading activity.

Despite being dropped from several Russell value indices, Entravision Communications has seen strong recent momentum, with a 44.18% 1 month share price return and a 343.05% 3 month share price return, alongside a 493% 1 year total shareholder return. Together, these figures paint a picture of building enthusiasm and shifting risk perceptions around the stock.

If this kind of sharp move has you thinking about where else capital is flowing, it could be a good moment to size up 20 top founder-led companies

With Entravision Communications now outside key value indices but posting sharp recent gains and an indicated intrinsic value above the current US$13.38 share price, should you see upside still on the table, or assume markets are already pricing in future growth?

Preferred Price-to-Sales multiple of 2.2x: Is it justified?

On the latest figures, Entravision Communications is trading on a P/S ratio of 2.2x, which screens as expensive relative to both its closest peers and the broader US Media industry.

The P/S ratio compares a company’s share price to its revenue per share, so it is often used when a company is unprofitable and earnings based ratios do not apply. For Entravision Communications, where the business reports a loss of $18.263m on revenue of $552.714m, the P/S multiple is effectively a shorthand for how much investors are willing to pay today for each dollar of sales across its Media and Advertising Technology & Services segments.

According to Simply Wall St’s checks, the 2.2x P/S for Entravision Communications is higher than the peer average of 1.7x and also above the US Media industry average of 1.1x. That positions the stock at a clear premium to sector revenue multiples, even as the company remains unprofitable and interest payments are not well covered by earnings.

Result: Price-to-Sales of 2.2x (OVERVALUED)

However, Entravision Communications still reports a US$18.263m loss and carries interest costs that are not well covered. As a result, any pressure on revenue or financing could quickly challenge bullish expectations.

Another view on Entravision Communications valuation

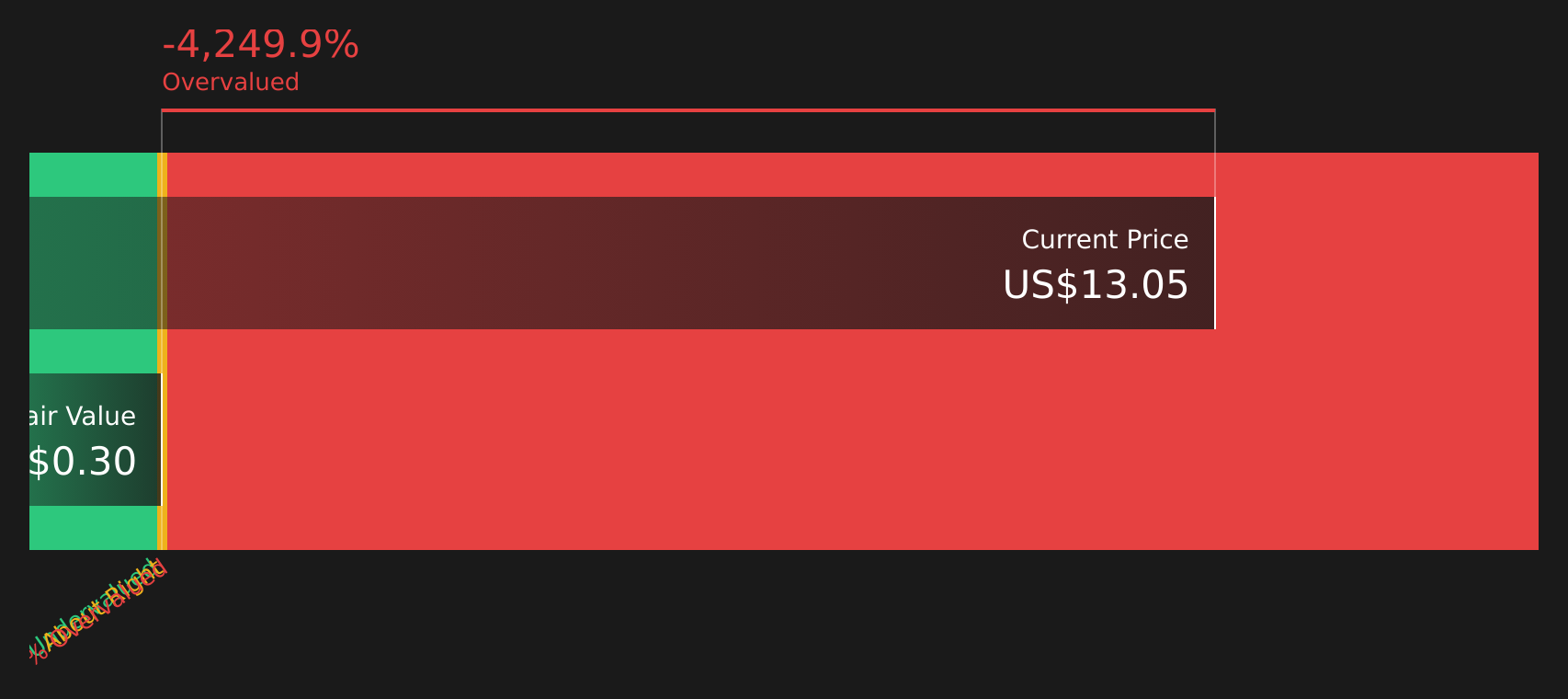

While the 2.2x P/S ratio makes Entravision Communications look expensive next to peers, the SWS DCF model points in the same direction. With the share price at $13.38 versus an estimated future cash flow value of $0.30, this framework also flags rich pricing based on current assumptions. The key question is whether the recent rally is leaning too far ahead of the fundamentals.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Entravision Communications for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals around Entravision Communications leave you uncertain, move quickly to review the underlying data and pressure test the risk picture yourself using the 5 important warning signs.

Looking for more investment ideas beyond Entravision Communications?

If Entravision Communications has your attention, do not stop here. A broader watchlist of ideas can help you compare risks, valuations and business quality more clearly.

- Target potential mispricings by scanning for companies trading below intrinsic value using the 41 high quality undervalued stocks.

- Strengthen your income stream by reviewing companies offering sustained payouts through the 8 dividend fortresses.

- Limit unnecessary surprises by focusing on companies with steadier profiles using the 73 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.