Is ESAB (ESAB) A Bargain On Its Board Changes?

ESAB Corporation ESAB | 0.00 |

Why ESAB’s New Board Roles Matter for Investors

ESAB (ESAB) recently reshaped its board leadership, appointing Mitchell P. Rales as Executive Chair and Rhonda Jordan as Lead Independent Director. These moves focus attention on the company’s governance and ongoing transformation.

For investors tracking ESAB stock, these appointments highlight how the board intends to organize oversight, clarify leadership roles, and support the existing management team as it pursues the company’s growth and transformation plans.

ESAB’s latest governance changes come after a mixed period for the stock, with a 1-day share price return of 2.03% to US$98.82, a 30-day share price return of 4.54%, and a 1-year total shareholder return that declined 18.23%, while the 3-year total shareholder return is up 50.66%.

If this kind of governance story has you thinking about longer term opportunities, it can be useful to also look at companies with stronger balance sheets and fundamentals by checking the solid balance sheet and fundamentals stocks screener (48 results)

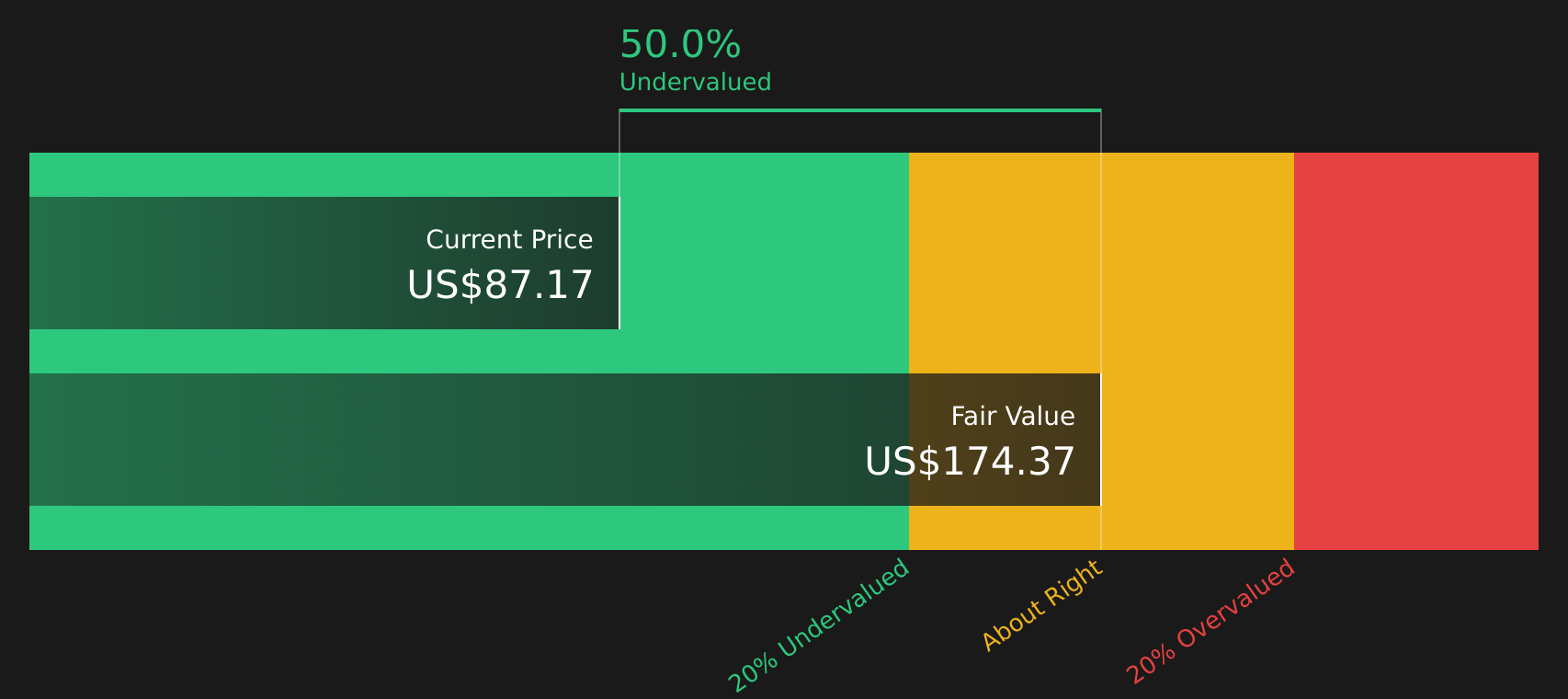

With ESAB trading at US$98.82 and showing an indicated 39% intrinsic discount alongside a sizeable gap to analyst targets, you have to ask: is the stock mispriced today, or is the market already baking in future growth?

Preferred P/E of 26x: Is it justified?

At a last close of $98.82, ESAB is being assessed as trading at good value relative to both its own estimated fair valuation and to peers, with a P/E of 26x that screens as lower than several comparison points.

The P/E multiple compares ESAB’s share price to its earnings per share, so a 26x P/E effectively reflects what investors are currently paying for each dollar of earnings. For a company operating across welding, cutting, and gas control equipment, earnings-based metrics are often a key reference point because cash generation and profitability can matter more than asset values.

On that basis, ESAB is described as good value versus the Machinery industry average P/E of 27.5x, and even more so against the peer average of 70.9x. Compared to an estimated fair P/E of 30.4x, the current 26x level also sits meaningfully lower, which indicates a valuation that could move closer to that fair ratio if the market re rates the stock in line with those benchmarks.

Result: Price-to-earnings of 26x (UNDERVALUED)

However, ESAB’s recent 1 year shareholder return decline and its exposure across multiple regions could quickly challenge this valuation story if sentiment or demand weakens.

Another View: ESAB Through a Cash Flow Lens

While ESAB looks inexpensive on a 26x P/E against peers and its fair ratio of 30.4x, the SWS DCF model suggests an even larger gap. The model estimates a future cash flow value of $163.03 versus the current $98.82 share price, which implies the stock screens as undervalued on cash flows too. That raises a key question: are earnings or cash flows giving you the clearer signal here?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ESAB for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 43 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Given the mixed signals around ESAB, it can help to move quickly, review the underlying data, and test your own thesis against the 4 key rewards and 1 important warning sign.

Looking for more ESAB investment ideas?

If ESAB has sharpened your focus on valuation and governance, do not stop here. Use the Simply Wall Street Screener to surface fresh, data driven stock ideas.

- Target opportunities with solid fundamentals by checking the solid balance sheet and fundamentals stocks screener (48 results).

- Hunt for potential value candidates that the market may be overlooking through the 43 high quality undervalued stocks.

- Prioritize stability and capital preservation by reviewing the 67 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.