Is Expanding Scorpio Adoption Among AI Providers Changing the Investment Case for Astera Labs (ALAB)?

Astera Labs ALAB | 0.00 |

- Earlier this week, Needham analyst Quinn Bolton reiterated a positive outlook on Astera Labs, highlighting robust demand for the Scorpio, Aries, and Taurus product lines, with the Scorpio X series achieving adoption from over ten AI and cloud service providers and Scorpio P switches contributing more than 10% of revenue in volume production.

- This analyst recognition comes as Astera Labs reported a strong second quarter and prepares for increased visibility through presentations at upcoming Deutsche Bank and Citi financial conferences, signaling continued market momentum in advanced connectivity solutions for AI infrastructure.

- We'll explore how Astera Labs' expanding Scorpio product adoption among AI and cloud providers could influence its investment narrative moving forward.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

Astera Labs Investment Narrative Recap

To be a shareholder in Astera Labs, you need to believe in the long-term expansion of AI infrastructure and the critical role of high-speed connectivity solutions. The latest analyst recognition reinforces optimism around demand for Scorpio switches, but does not significantly change the biggest near-term catalyst, wider adoption by major AI and cloud customers, or address the ongoing risk of customer concentration, which remains a key vulnerability to revenue stability.

Among recent developments, Astera Labs’ upcoming presentations at the Deutsche Bank and Citi financial conferences are particularly relevant, offering potential for greater investor engagement just as its Scorpio product family gains momentum within AI and cloud infrastructure markets. This exposure may support short-term excitement, but sustained performance will rely on continued product wins across a broader customer base.

By contrast, investor attention should not overlook the persistent risk that heavy reliance on a concentrated group of hyperscale customers…

Astera Labs' outlook anticipates $1.4 billion in revenue and $364.6 million in earnings by 2028. This projection is based on a 33.7% annual revenue growth rate and a $264.4 million increase in earnings from the current $100.2 million.

Uncover how Astera Labs' forecasts yield a $166.47 fair value, a 7% downside to its current price.

Exploring Other Perspectives

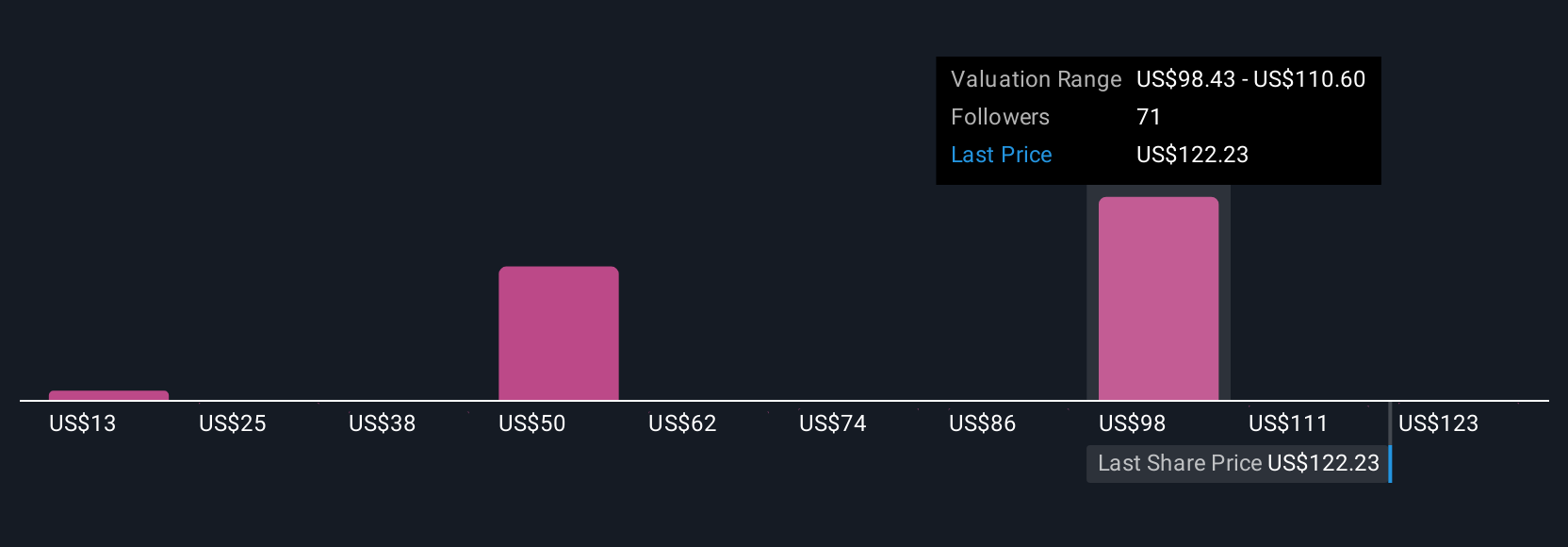

The Simply Wall St Community includes 27 member valuations with fair value estimates for Astera Labs ranging widely from US$13.25 to US$250. As you weigh these perspectives, keep in mind that customer concentration continues to be a major risk with consequences for revenue stability and operational momentum.

Explore 27 other fair value estimates on Astera Labs - why the stock might be worth less than half the current price!

Build Your Own Astera Labs Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Astera Labs research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Astera Labs research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Astera Labs' overall financial health at a glance.

Seeking Other Investments?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 20 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.