Is Huntsman (HUN) Cheap After Its Sharp Share Price Pullback?

Huntsman Corporation HUN | 0.00 |

Huntsman (HUN) has been drawing attention after a steep share price decline of about 26% over the past month and roughly 14% over the past 3 months, prompting fresh questions about the stock.

At a latest share price of $11.41, Huntsman’s recent 30 day share price return of down 25.67% and 90 day return of down 14.27% contrast with a year to date share price gain of 11.97%. The 1 year total shareholder return of 14.42% sits against a 3 year total shareholder return that has fallen 52.22%, suggesting recent momentum has weakened after a stronger spell.

If Huntsman’s recent swing has you reassessing your watchlist, this could be a useful moment to broaden your search and check out 20 top founder-led companies

With Huntsman now trading at $11.41 after a sharp pullback, the key question is whether this chemicals stock is being overly punished or if the recent weakness simply reflects a fair reset. Is there a genuine buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 19.9% Undervalued

Huntsman’s most followed narrative sets a fair value of $14.25 per share, compared with the recent $11.41 close. This frames the current weakness as a discount to that view.

The company is actively transforming its portfolio away from lower margin, commodity chemicals toward specialty chemicals (e.g., adhesives, elastomers, aerospace composites). It is aiming to further improve EBITDA margins and overall profitability in future cycles. Cost optimization, working capital discipline, and strategic asset closures (e.g., the maleic anhydride facility in Europe) are expected to enhance free cash flow generation and support improved net margins and earnings resilience during the next macro upturn.

Want to see what sits behind that shift toward specialty chemicals and tighter cost control? The narrative hinges on specific revenue growth, margin improvement and valuation assumptions that materially shape the $14.25 fair value.

Result: Fair Value of $14.25 (UNDERVALUED)

However, Huntsman’s story could change quickly if prolonged overcapacity in key polyurethane markets, or continued high European energy and raw material costs, keep margins under pressure.

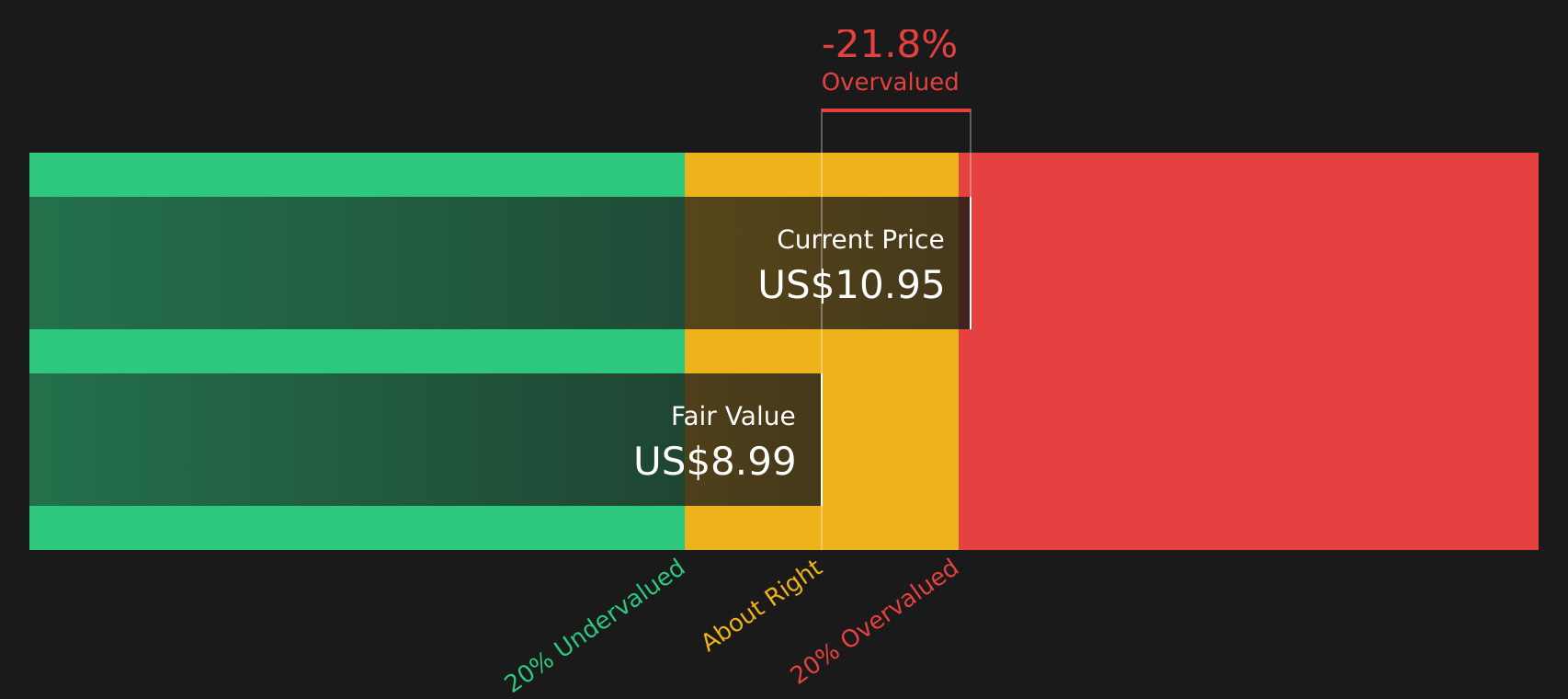

Another View: Huntsman And The SWS DCF Model

The narrative around Huntsman being about 19.9% undervalued sits awkwardly next to our DCF model, which puts future cash flows at $8.99 per share, below the recent $11.41 price. That points to the stock trading above this fair value estimate. Which story do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Huntsman for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of concerns and positives around Huntsman leaves you unsure, quickly review the data, compare different perspectives, and weigh up the 2 key rewards and 3 important warning signs.

Looking for more investment ideas beyond Huntsman?

If Huntsman has sharpened your focus on pricing and risk, do not stop here. Broaden your watchlist with stocks that match your own investing style.

- Target quality at a discount by scanning companies that combine strong fundamentals with appealing valuations using the 44 high quality undervalued stocks.

- Build a sturdier core portfolio by focusing on businesses with reliable balance sheets through the solid balance sheet and fundamentals stocks screener (48 results).

- Spot potential future leaders early by searching for underfollowed companies with solid fundamentals in the screener containing 19 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.