Is Intuitive Surgical (ISRG) Pricing Too High After Recent Share Price Weakness

Intuitive Surgical, Inc. ISRG | 0.00 |

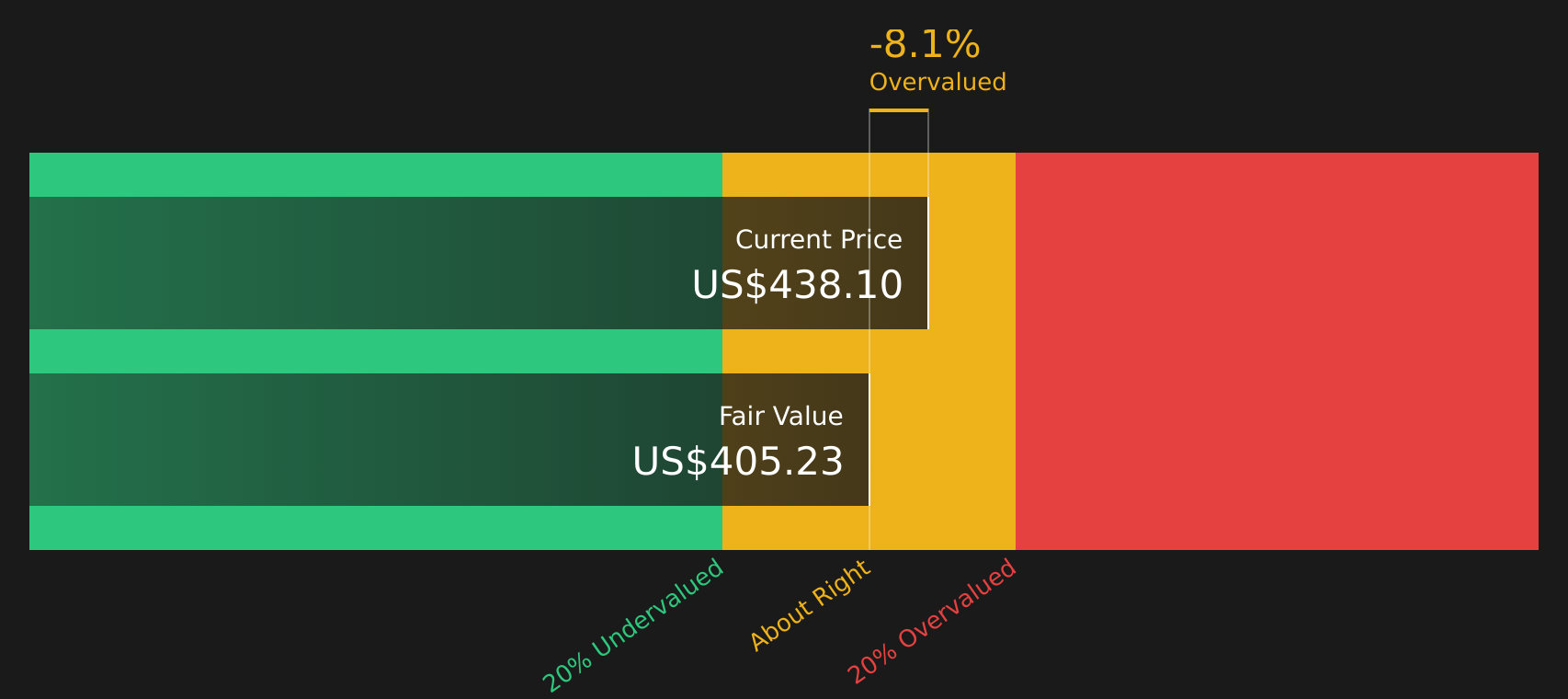

- For investors considering whether Intuitive Surgical at around US$457.78 is a fair deal, expensive, or potentially mispriced, this article walks through key clues in the valuation story.

- The stock has seen mixed recent returns, with a 5.1% decline over the last 7 days, a 1.3% gain over the last 30 days, and year to date and 1 year returns of 18.5% and 13.5% declines, while the 3 and 5 year returns sit at 50.2% and 60.2% respectively.

- Recent coverage has continued to focus on Intuitive Surgical as a leading name in robotic assisted surgery and the broader medical equipment space, keeping attention on how the company is positioned within its industry. At the same time, ongoing discussion among analysts and investors has centered on whether the current share price reflects expectations already built into the stock or leaves room for further upside or downside.

- Simply Wall St currently gives Intuitive Surgical a valuation score of 1 out of 6. Next up is a closer look at how different valuation methods assess the stock today and, at the end of the article, a more comprehensive way to think about valuation beyond any single model.

Intuitive Surgical scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Intuitive Surgical Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model projects a company’s future cash flows and then discounts them back to today’s value, aiming to estimate what the entire business might be worth in today’s dollars.

For Intuitive Surgical, the latest twelve month Free Cash Flow (FCF) is about $2.32b. Analysts have supplied a series of FCF estimates that are combined with further projections, using a 2 Stage Free Cash Flow to Equity model. Under this framework, Simply Wall St extrapolates FCF out to 2035, with projected FCF for 2030 of $6.14b and a set of discounted cash flows over the 2026 to 2035 period that all remain in the multi billion dollar range.

Bringing all of those projected cash flows back to today, the DCF model arrives at an estimated intrinsic value of about $372.55 per share, compared with the current share price of around $457.78. That gap implies the stock is about 22.9% overvalued based on this cash flow based approach.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Intuitive Surgical may be overvalued by 22.9%. Discover 50 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Intuitive Surgical Price vs Earnings

For a profitable company, the P/E ratio is a straightforward way to connect what you pay for the stock with the earnings it currently produces. It helps you see how many dollars of share price you are paying for each dollar of earnings.

What counts as a “normal” P/E depends on how quickly earnings are expected to grow and how much risk investors see in those earnings. Higher expected growth or lower perceived risk tends to justify a higher P/E, while slower growth or higher risk usually points to a lower, more conservative multiple.

Intuitive Surgical currently trades on a P/E of 54.42x. That sits well above the Medical Equipment industry average of 23.56x and the peer average of 26.14x. Simply Wall St’s proprietary Fair Ratio for Intuitive Surgical is 32.14x. This Fair Ratio aims to be more tailored than a simple peer or industry comparison because it factors in the company’s earnings growth profile, profit margins, size and risk characteristics, alongside its sector.

Comparing the current P/E of 54.42x with the Fair Ratio of 32.14x suggests the shares trade at a richer multiple than the model would indicate.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 17 top founder-led companies.

Upgrade Your Decision Making: Choose your Intuitive Surgical Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St let you attach a clear story about Intuitive Surgical to the numbers by linking your view on its patents, da Vinci platform, growth drivers, risks and margins to a specific forecast and Fair Value. You can then compare that Fair Value with the current price. Each Narrative lives on the Community page and updates automatically when fresh news or earnings arrive. This is why one investor might reasonably see Intuitive Surgical as worth about US$325.55 per share, while another, using different assumptions about future revenue growth, profit margins, discount rates and P/E, arrives at a Fair Value closer to US$750 per share.

For Intuitive Surgical, however, we will make it really easy for you with previews of two leading Intuitive Surgical Narratives:

Fair value: US$532.46 per share

Implied pricing gap vs last close: about 14.1% below this fair value

Revenue growth assumption: 12%

- The author frames Intuitive Surgical as a long established pioneer in robotic assisted surgery, with the da Vinci platform evolving over several hardware generations into a broad surgical ecosystem.

- Key focus sits on the installed base of 9,539 systems and high procedure volumes, with a large share of revenue coming from recurring instruments, services and software that support cash flow and margins.

- Even with a fair value estimate close to the current share price, the author sees the stock as usually richly valued and treats new purchases as a matter of patience and required return rather than enthusiasm alone.

Fair value: US$325.55 per share

Implied pricing gap vs last close: about 40.7% above this fair value

Revenue growth assumption: 12%

- The bear leaning narrative still recognises strong adoption drivers for robotic surgery, including new procedures, subscriptions on instruments and services, and potential digital tools around surgery.

- At the same time, it highlights headwinds such as high system costs, regulatory and reimbursement uncertainty, competition and reliance on the da Vinci platform.

- Given these points, the author judges the shares as overvalued relative to the risks and growth assumptions, and flags that any disappointment against high expectations could have a material impact on returns.

If these two viewpoints help clarify your own stance on Intuitive Surgical, it can be useful to see how they compare with other angles on growth, risks and pricing across the rest of the community, starting with To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Intuitive Surgical on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Intuitive Surgical? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.