Is It Time To Reassess Honeywell (HON) After Recent Share Price Pullback?

Honeywell International Inc. HON | 0.00 |

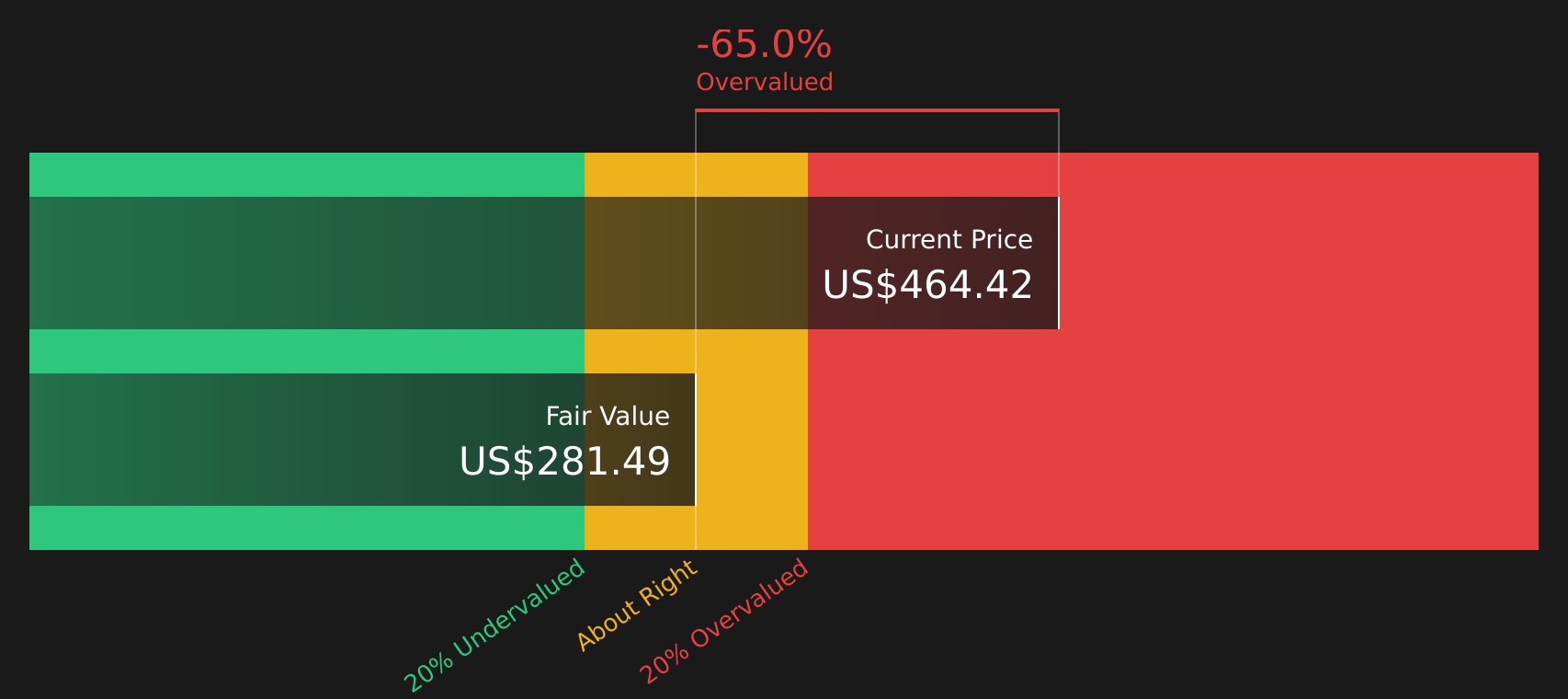

- Investors may be wondering if Honeywell International at around US$205.88 is offering good value right now, or if the price already reflects its strengths.

- The stock is up 5.1% year to date, but has fallen 7.8% over the past week and 6.0% over the past month. The return over the last year is down 1.1%, and up 16.2% and 10.7% over the past 3 and 5 years respectively.

- Recent coverage has focused on how Honeywell fits into long term themes such as industrial automation, aerospace exposure and energy efficiency. This helps frame how investors think about its future cash flows and risk profile. These themes often influence how much investors are willing to pay for each dollar of earnings or sales.

- Right now Honeywell scores 3 out of 6 on Simply Wall St's valuation checks, which you can see in detail at this valuation scorecard. The rest of this article will walk through different ways to look at that value and finish with a broader framework that can help you judge the stock beyond any single model.

Approach 1: Honeywell International Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes the cash that a company is expected to generate in the future and then discounts those amounts back to today to estimate what the business might be worth now.

For Honeywell International, the latest twelve month Free Cash Flow is about $4.15b. Analysts provide detailed estimates for the next few years, and Simply Wall St extends those projections further. By 2030, projected Free Cash Flow is $7.71b, with interim yearly projections between 2026 and 2035 ranging from roughly $5.07b to $9.36b before discounting.

Using a 2 Stage Free Cash Flow to Equity model built on these projections, the estimated intrinsic value for the stock is $247.61 per share. Compared with the recent share price of about $205.88, this suggests the stock trades at a 16.9% discount to that DCF estimate on this model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Honeywell International is undervalued by 16.9%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Approach 2: Honeywell International Price vs Earnings

For profitable companies, the P/E ratio is a useful way to think about what you are paying for each dollar of earnings. It links directly to today’s share price and current profitability, which is usually the starting point for many investors.

The “right” or “fair” P/E level depends on what the market expects for future growth and how risky those earnings are perceived to be. Higher expected growth and lower perceived risk often justify a higher P/E, while slower growth or higher risk usually point to a lower multiple.

Honeywell International currently trades on a P/E of 32.88x. This is above the broader Industrials sector average of 12.80x and slightly above the peer group average of 30.72x. Simply Wall St’s Fair Ratio for Honeywell is 35.59x. This is its proprietary estimate of what the P/E “should” be based on the company’s earnings growth profile, profit margins, industry, market cap and risk factors.

Compared with simple peer or industry comparisons, the Fair Ratio aims to be more tailored because it incorporates those company specific drivers rather than relying on broad averages alone. Here, the current P/E of 32.88x sits below the Fair Ratio of 35.59x. This points to the stock being undervalued on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Honeywell International Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are introduced here as a simple way for you to attach a clear story to your numbers by linking Honeywell International’s business outlook, your assumptions for future revenue, earnings and margins, and your view of fair value into one connected picture.

On Simply Wall St’s Community page, Narratives are presented as accessible tools that let you compare your own fair value to the current share price and to other investors’ views, with each Narrative effectively saying, “here is the story I believe, and here is what that story implies this stock is worth.”

Because Narratives update automatically when new information appears, such as Honeywell’s guidance for sales of US$38.8b to US$39.8b in 2026 or new data on its aerospace spin and automation focus, your fair value view can move with the story rather than staying frozen in an old spreadsheet.

For Honeywell International, one investor might build a more optimistic Narrative anchored around a fair value near US$296.00 that leans into themes like energy efficiency, automation and higher margins. Another might prefer a more cautious Narrative closer to US$200.84 that stresses tariff exposure, separation costs and execution risk. Narratives make those different perspectives transparent so you can decide which story, and which fair value range, best matches your own view.

For Honeywell International, however, we’ll make it really easy for you with previews of two leading Honeywell International Narratives:

On Simply Wall St you can see these Narratives in full, compare their assumptions line by line and decide which one feels closer to how you see the Honeywell story playing out.

Fair value in this bullish Narrative: about US$320.19 per share.

Implied discount to that fair value at the recent US$205.88 share price: about 36%.

Revenue growth assumption used in this Narrative: 16.65%.

- Frames Honeywell RemainCo as an automation and energy technology business tied closely to AI data center build outs, LNG projects and sustainable aviation fuel, supported by about US$19.4b of contracted backlog.

- Argues that the current share price still reflects a conglomerate structure, while the planned separation and Honeywell Forge software mix could support a higher P/E multiple over time.

- Highlights risks around execution, macro sensitivity and tariffs, but suggests these sit against a large installed base and a shift toward higher margin, recurring revenue.

Fair value in this more cautious Narrative: about US$200.84 per share.

Implied premium to that fair value at the recent US$205.88 share price: about 3%.

Revenue growth assumption used in this Narrative: 4.74%.

- Focuses on tariff exposure, separation costs of about US$1.5b to US$2b and restructuring within Industrial Automation as factors that could pressure margins and earnings.

- Builds a Fair Value based on lower revenue growth and a reduced future P/E of about 22.6x, even while assuming margins improve and earnings rise over time.

- Points out that analyst targets span a wide range, which reflects different views on how much value the aerospace spin, portfolio reshaping and capital returns can ultimately create.

Together these two Narratives bracket a wide fair value range and spell out exactly which assumptions need to be true for Honeywell International stock to look cheap or full at today’s price. If you want to see how the rest of the community is joining the dots between valuation, risks and long term themes like automation, aerospace and energy efficiency, it is worth spending a few minutes with the full set of investor Narratives. See what the community is saying about Honeywell International

Do you think there's more to the story for Honeywell International? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.