Is It Time To Reassess UPS (NYSE:UPS) After Its Recent Share Price Recovery

United Parcel Service, Inc. Class B UPS | 0.00 |

- Wondering if United Parcel Service (UPS) stock at around US$108.67 still offers value, or if the easy gains are already behind it.

- The share price has moved 4.0% over the last week, 12.8% over the last month, 7.6% year to date, while the past 1 year return sits at 17.9% and the stock is still down 25.3% over 3 years and 32.3% over 5 years.

- Those mixed returns sit against a backdrop of ongoing focus on parcel volumes, cost efficiency and broader logistics demand, with investors weighing how these factors might influence longer term expectations for UPS. Recent coverage has concentrated on how large logistics groups position themselves for changing shipping patterns and capital spending. This helps set the scene for assessing what a fair price for the stock might be today.

- UPS currently scores 4/6 on Simply Wall St's valuation checks. The next sections will walk through what that means using different valuation approaches and then finish with a way of looking at value that can tie all of those methods together.

Approach 1: United Parcel Service Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes expected future cash flows, then discounts them back to what they might be worth in today’s dollars. It is essentially asking what someone might reasonably pay today for the cash that United Parcel Service could generate in the future.

UPS has reported last twelve month free cash flow of about $4.0b. Based on analyst inputs for the next few years and then extrapolations by Simply Wall St, free cash flow is projected at $7.46b in 2029 and continues to be projected further out to 2035 using the 2 Stage Free Cash Flow to Equity approach. Those later year figures are all expressed in $, and the model discounts each year’s projected cash flow back to today using a required rate of return.

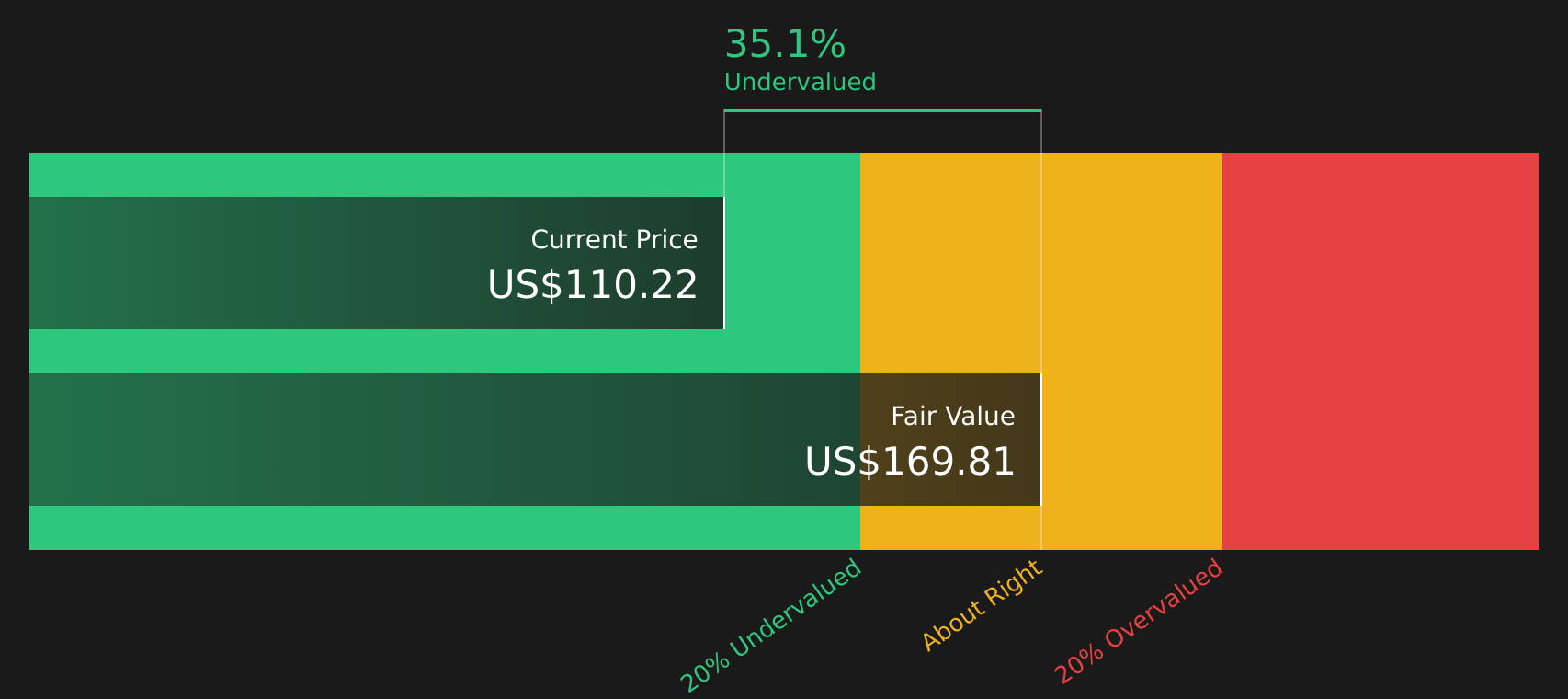

Putting all of those discounted projections together produces an estimated intrinsic value of about $168.75 per share. Against a current share price around $108.67, the model points to an implied discount of 35.6%, which indicates that the stock appears undervalued on this DCF view.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests United Parcel Service is undervalued by 35.6%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Approach 2: United Parcel Service Price vs Earnings

For a consistently profitable company, the P/E ratio is a straightforward way to link what you pay for the stock to the earnings it generates. It tells you how many dollars investors are currently willing to pay for each dollar of earnings.

What counts as a “normal” P/E often reflects how the market views a company’s growth potential and risk. Higher expected growth or lower perceived risk can justify a higher multiple, while slower expected growth or higher risk can point to a lower one.

United Parcel Service currently trades on a P/E of 17.60x. This sits above the Logistics industry average of about 14.99x, but below the peer group average of 22.50x. To move beyond simple comparisons, Simply Wall St uses a proprietary “Fair Ratio” which estimates what a reasonable P/E could be, given factors such as earnings growth, profit margins, industry, market cap and company specific risks.

The Fair Ratio for UPS is 24.12x, which is higher than the current 17.60x. On this basis, the stock screens as undervalued relative to what the model suggests might be a fair P/E for the business today.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your United Parcel Service Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so this is where Narratives come in. They let you attach a clear story about United Parcel Service to numbers like your fair value estimate, expected revenue, earnings and margins. You can then compare that fair value with the current price in a simple view on Simply Wall St’s Community page that updates automatically when new news or earnings arrive. This view can span very different perspectives. For example, one cautious UPS Narrative on the platform currently anchors fair value around US$84.58, while a more optimistic UPS Narrative anchors fair value around US$135, giving you a structured way to decide where your own view sits on that spectrum.

For United Parcel Service, however, we will make it really easy for you with previews of two leading United Parcel Service Narratives:

Fair value in this bullish Narrative: US$135.00 per share

Implied discount to that fair value at the recent US$108.67 price: about 19.5% below the Narrative fair value

Revenue growth assumption used in this Narrative: 4.38% per year

- Sees UPS’s physical network, automation and facility rationalisation as core strengths that can support earnings recovery once current pressures ease.

- Highlights healthcare logistics, cold chain and international trade lanes as important contributors to higher quality, recurring revenue.

- Accepts risks around competition, labour, regulation and sustainability costs, but assumes these are manageable within a higher long term earnings and margin profile.

Fair value in this cautious Narrative: US$95.21 per share

Implied premium to that fair value at the recent US$108.67 price: about 14.1% above the Narrative fair value

Revenue growth assumption used in this Narrative: 1.75% per year

- Focuses on higher costs, new debt, union disputes and governance concerns that could weigh on profitability and limit financial flexibility.

- Views the Efficiency Reimagined plan as important but still unproven, with execution risk around facility closures, job cuts and automation spending.

- Assumes only modest revenue and margin improvement and applies a lower P/E than the industry, leading to a fair value below the current share price.

Once you have a sense of which Narrative feels closer to your own expectations for UPS, you can adjust the assumptions and build a version that matches your view, then track how that story evolves alongside future earnings, news and valuation updates. To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for United Parcel Service on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for United Parcel Service? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.