هل حان الوقت لإعادة تقييم شركة وينغ ستوب (WING) بعد الانخفاض الحاد في سعر سهمها هذا العام؟

Wingstop, Inc. WING | 0.00 |

- قد يتساءل المستثمرون عما إذا كان سهم Wingstop بسعر حوالي 134.88 دولارًا أمريكيًا قد بدأ يبدو مثيرًا للاهتمام مرة أخرى، أو ما إذا كان تقييم السهم لا يزال يبدو غير متوافق مع أساسياته.

- شهد سعر السهم تقلبات حادة مؤخراً، حيث انخفض بنسبة 17.8% خلال الأيام السبعة الماضية، وبنسبة 18.8% خلال الثلاثين يوماً الماضية، وبنسبة 47.5% منذ بداية العام. سيؤثر هذا على نظرة بعض المستثمرين إلى كل من إمكانات الربح والمخاطر.

- ركزت التغطية الإعلامية الأخيرة على مكانة وينغ ستوب في قطاع الخدمات الاستهلاكية، وكيف يمكن أن تتغير توجهات المستثمرين تجاه أسهم المطاعم بسرعة عند تغير التوقعات، سواءً فيما يتعلق بالنمو أو هوامش الربح أو خطط التوسع. وبالنظر إلى أداء سعر السهم، يُعد هذا السياق أساسيًا لفهم سبب إعادة السوق تقييم السعر الذي يرغب في دفعه مقابل السهم.

- حالياً، يبلغ تقييم أسهم وينغ ستوب 3 من 6 ، مما يشير إلى أن الأسهم مقومة بأقل من قيمتها الحقيقية في نصف المعايير المستخدمة هنا. ستقارن الأقسام التالية بين طرق التقييم المختلفة قبل أن نختتم بنظرة أشمل لمفهوم "القيمة العادلة".

النهج الأول: تحليل التدفقات النقدية المخصومة (DCF) لسلسلة مطاعم وينغ ستوب

يعتمد نموذج التدفقات النقدية المخصومة على حساب التدفقات النقدية المستقبلية المتوقعة، ثم خصمها إلى قيمتها الحالية لتقدير قيمة الشركة في الوقت الراهن. بمعنى آخر، يسأل هذا النموذج عن قيمة تلك الدولارات المستقبلية بالقيمة الحالية.

بالنسبة لشركة وينغ ستوب، يستخدم النموذج منهجية التدفق النقدي الحر إلى حقوق الملكية على مرحلتين. يبلغ التدفق النقدي الحر خلال الاثني عشر شهرًا الماضية حوالي 130.5 مليون دولار. يقدم المحللون تقديرات للتدفق النقدي الحر حتى عام 2030، بينما يقوم موقع سيمبلي وول ستريت باستقراء البيانات لما بعد فترة التحليل المحددة لإكمال مسار توقعات مدته عشر سنوات، بما في ذلك توقعات بتدفق نقدي حر قدره 292.5 مليون دولار في عام 2030. يتم خصم كل رقم من هذه الأرقام المستقبلية إلى قيمته الحالية ثم جمعها.

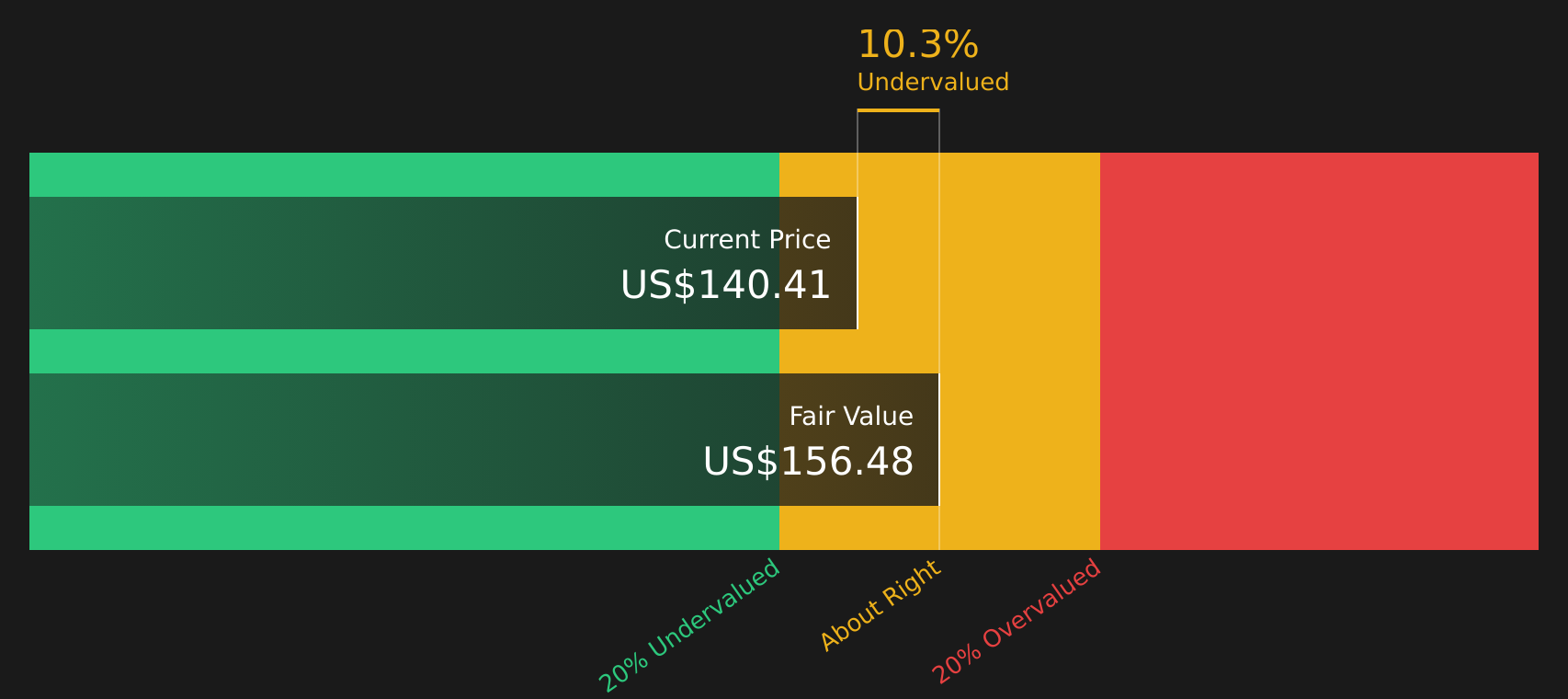

بناءً على ذلك، توصل نموذج التدفقات النقدية المخصومة إلى قيمة جوهرية تقديرية تبلغ حوالي 185.90 دولارًا أمريكيًا للسهم الواحد. وبالمقارنة مع سعر السهم الحالي البالغ حوالي 134.88 دولارًا أمريكيًا، فإن هذا يشير إلى خصم جوهري بنسبة 27.4% تقريبًا، مما يدل على أن السهم يُعتبر مقومًا بأقل من قيمته الحقيقية وفقًا لهذه المنهجية.

النتيجة: مُقَيَّم بأقل من قيمته الحقيقية

تشير تحليلاتنا للتدفقات النقدية المخصومة (DCF) إلى أن أسهم وينغ ستوب مقومة بأقل من قيمتها الحقيقية بنسبة 27.4%. تابع هذا السهم في قائمة مراقبتك أو محفظتك الاستثمارية ، أو اكتشف 51 سهماً آخر عالي الجودة ومقوم بأقل من قيمته الحقيقية .

النهج الثاني: سعر وينغ ستوب مقابل الأرباح

بالنسبة للشركات المربحة، يُعدّ مُضاعف الربحية (P/E) وسيلةً مفيدةً لمعرفة المبلغ الذي يدفعه المستثمرون حاليًا مقابل كل دولار من الأرباح. فهو يربط سعر السهم مباشرةً بالأرباح، وهو ما يدعم في نهاية المطاف قيمة الشركة على المدى الطويل.

يعتمد تحديد نسبة السعر إلى الأرباح "الطبيعية" أو "العادلة" على سرعة نمو الأرباح المتوقعة ومستوى المخاطرة المتوقعة. فارتفاع معدل النمو المتوقع أو انخفاض مستوى المخاطرة المتصورة قد يبرر دفع المستثمرين نسبة أعلى، بينما يشير تباطؤ النمو أو ارتفاع مستوى المخاطرة عادةً إلى نسبة أقل.

تُتداول أسهم وينغ ستوب حاليًا بنسبة سعر إلى ربحية تبلغ 32.83 ضعفًا، مقارنةً بمتوسط قطاع الضيافة البالغ حوالي 20.58 ضعفًا، ومتوسط مجموعة الشركات النظيرة البالغ 46.03 ضعفًا. كما يوفر موقع Simply Wall St نسبة "القيمة العادلة" الخاصة به لوينغ ستوب، والتي تبلغ 22.99 ضعفًا. صُممت هذه النسبة لتعكس المضاعف المتوقع للسهم بالنظر إلى معدل نمو أرباحه، وقطاعه، وهوامش ربحه، وقيمته السوقية، والمخاطر الرئيسية التي يواجهها.

لأن نسبة السعر العادلة تجمع بين عوامل خاصة بالشركة وسياق قطاعها، فإنها توفر رؤية أكثر دقة من مجرد مقارنة السهم بنظرائه أو متوسط القطاع. وبمقارنة نسبة السعر إلى الأرباح الحالية لشركة وينغ ستوب البالغة 32.83 ضعفًا بنسبة السعر العادلة البالغة 22.99 ضعفًا، يتضح أن السهم مُبالغ في تقييمه وفقًا لهذا المعيار.

النتيجة: مبالغ في تقييمها

نسبة السعر إلى الأرباح لا تعكس الصورة كاملة، ولكن ماذا لو كانت الفرصة الحقيقية تكمن في مكان آخر؟ ابدأ بالاستثمار في الشركات العريقة، لا في المديرين التنفيذيين. اكتشف أفضل 19 شركة يقودها مؤسسوها .

حسّن عملية اتخاذ قراراتك: اختر روايتك الخاصة عن وينغ ستوب

وقد ذكرنا سابقاً أن هناك طريقة أفضل لفهم التقييم، لذلك يتم تقديم السرديات هنا كأداة بسيطة تتيح لك ربط قصة واضحة حول Wingstop بالأرقام التي تهمك، مثل القيمة العادلة، وتوقعاتك الخاصة للإيرادات والأرباح وهوامش الربح المستقبلية.

في صفحة مجتمع Simply Wall St، تساعدك التحليلات على ربط قصة الشركة بمجموعة من التوقعات، ثم بقيمتها العادلة. هذا يعني أنه يمكنك مقارنة هذه القيمة العادلة بسرعة مع سعر السهم الحالي، وتحديد ما إذا كان السهم أقرب إلى الشراء أو الاحتفاظ أو البيع بالنسبة لك.

لأن السرديات على المنصة يتم تحديثها تلقائيًا عند ظهور معلومات جديدة، مثل تقارير الأرباح الجديدة أو الأخبار أو مراجعات المحللين، فإن وجهة نظرك حول Wingstop يمكن أن تظل متوافقة مع أحدث البيانات دون الحاجة إلى إعادة بناء النماذج من الصفر.

بالنسبة لشركة وينغ ستوب، قد يتبنى أحد المستثمرين رؤية أكثر تفاؤلاً تفترض قيمة عادلة تقارب 386.52 دولارًا أمريكيًا. بينما قد يفضل آخر رؤية أكثر حذرًا تقترب من 237.28 دولارًا أمريكيًا. إن مقارنة هذه القيم العادلة المختلفة جنبًا إلى جنب مع السعر الحالي توفر إطارًا أوضح لاتخاذ قرارك.

هل تعتقد أن هناك المزيد من التفاصيل حول قصة وينغ ستوب؟ توجه إلى مجتمعنا لترى ما يقوله الآخرون!

هذا المقال من Simply Wall St ذو طبيعة عامة. نقدم تعليقاتنا بناءً على البيانات التاريخية وتوقعات المحللين فقط، باستخدام منهجية محايدة، ولا يُقصد بمقالاتنا أن تكون نصائح مالية. لا يُشكل هذا المقال توصيةً بشراء أو بيع أي سهم، ولا يأخذ في الاعتبار أهدافك أو وضعك المالي. نهدف إلى تزويدك بتحليلات طويلة الأجل مدفوعة بالبيانات الأساسية. يُرجى ملاحظة أن تحليلنا قد لا يأخذ في الاعتبار آخر إعلانات الشركات الحساسة للسعر أو المعلومات النوعية. لا تمتلك Simply Wall St أي أسهم في أي من الشركات المذكورة.