Is It Time To Reconsider A. O. Smith (AOS) After Recent Share Price Softness?

A. O. Smith Corporation AOS | 0.00 |

- With A. O. Smith trading at around US$64.82, this article focuses on what the numbers say about value to help readers consider whether the price suggests opportunity or caution.

- The stock has had a mixed run recently, with a 1.7% decline over the last 7 days, a 1.2% gain over 30 days, and returns of 4.8% over 1 year, compared with a 5.1% decline year to date and a 0.5% decline over 3 years.

- These moves have come as investors reassess the company in the context of ongoing coverage and analysis, which keeps attention on how the current share price lines up with fundamentals. This backdrop makes it especially useful to step back and focus on what different valuation frameworks suggest about the stock today.

- On Simply Wall St's valuation checks, A. O. Smith has a score of 6 out of 6. The next sections will walk through those valuation approaches, followed by a broader way to think about what the stock may be worth.

Approach 1: A. O. Smith Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting the cash the business might generate in the future and discounting those amounts back to today.

For A. O. Smith, the model used is a 2 Stage Free Cash Flow to Equity approach. The company’s latest twelve month free cash flow is about $533.08 million. Analyst and extrapolated estimates point to free cash flow of $663.00 million in 2029, with a set of projections running out to 2035. Figures beyond the initial analyst window are extrapolated by Simply Wall St rather than coming directly from analyst reports.

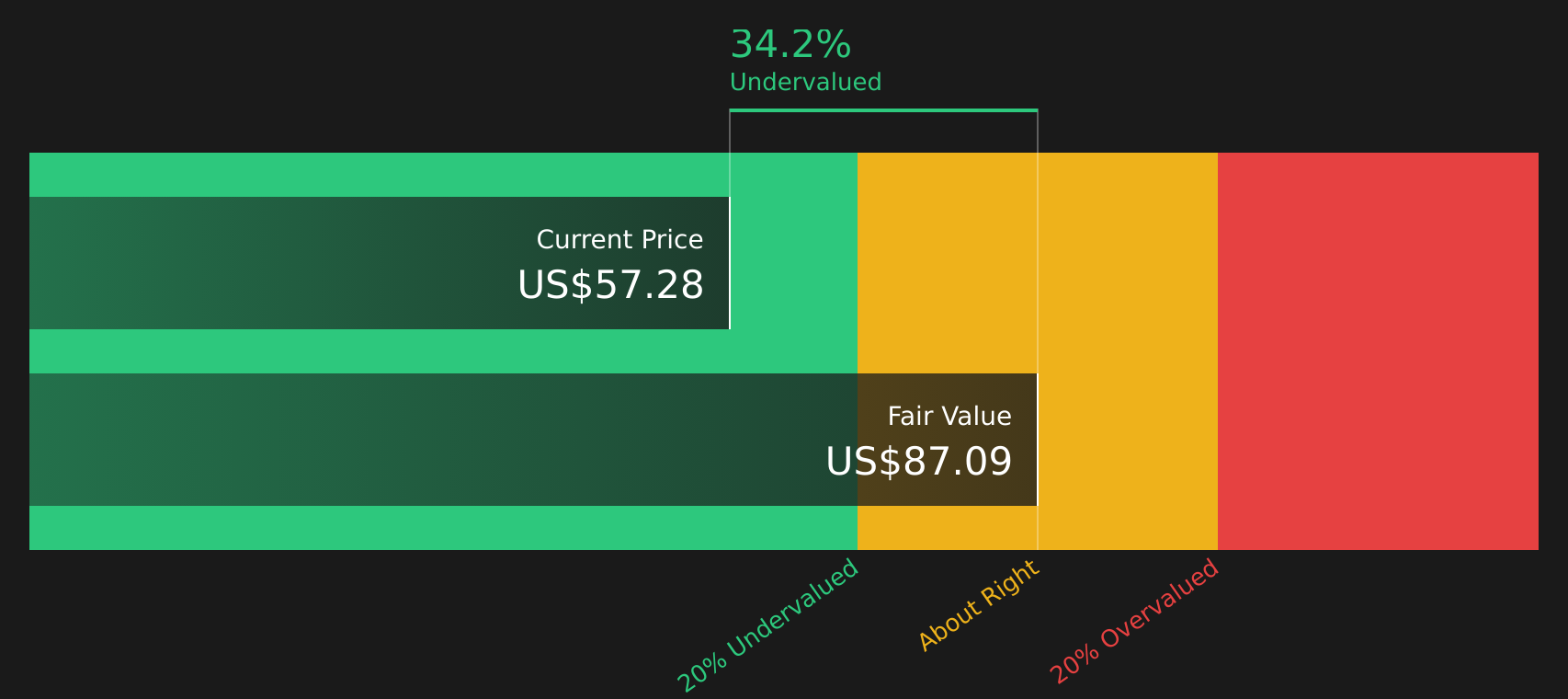

Bringing all these projected cash flows back to today’s dollars results in an estimated intrinsic value of about $87.71 per share. Compared with the recent share price of roughly $64.82, this DCF output suggests the stock trades at about a 26.1% discount, which indicates it may be undervalued based on this model alone.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests A. O. Smith is undervalued by 26.1%. Track this in your watchlist or portfolio, or discover 59 more high quality undervalued stocks.

Approach 2: A. O. Smith Price vs Earnings

For a profitable company like A. O. Smith, the P/E ratio is a practical way to think about value because it ties the share price directly to current earnings. Investors typically expect higher P/E ratios when they see stronger growth potential and lower perceived risk, and lower P/E ratios when growth expectations are muted or risks are higher.

A. O. Smith currently trades on a P/E of about 16.4x. This sits below the Building industry average of roughly 21.0x and also below the peer group average of about 27.5x, so the stock is priced at a lower earnings multiple than many comparable names. Simply Wall St’s Fair Ratio for A. O. Smith is 19.0x, which is the P/E level suggested by its earnings growth profile, industry, profit margins, market cap and risk characteristics.

The Fair Ratio is more tailored than a simple comparison with peers or the broad industry because it blends company specific factors, rather than assuming all businesses in the group deserve similar multiples. Setting the current P/E of 16.4x against the Fair Ratio of 19.0x indicates that the shares are trading below that model derived benchmark.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your A. O. Smith Narrative

Earlier it was mentioned that there is an even better way to think about valuation. Narratives let you attach your own story about A. O. Smith to the numbers by linking views on its future revenue, earnings and margins to a financial forecast, a fair value, and then a simple Fair Value versus Price comparison that updates automatically when new information arrives. This all happens within the Simply Wall St Community page where millions of investors share views. One investor might lean toward a higher fair value near US$100 if they focus on growth in high efficiency products and water treatment, while another might anchor closer to US$61 if they emphasise risks around mature markets and cost pressures. Narratives help you see clearly what assumptions would need to be true before deciding whether the current price looks high or low against your own fair value range.

For A. O. Smith however, we will make it really easy for you with previews of two leading A. O. Smith Narratives:

Fair value in this bullish narrative: US$78.30

Implied discount to this fair value at the recent US$64.82 share price: about 17.2%.

Revenue growth assumption: 3.71%.

- Focus on higher efficiency and smart products, digital capabilities, and new R&D investment that are expected to support margins and premium product positioning.

- Greater exposure to India and other emerging markets, together with shifts in North America water treatment channels, is aimed at reducing reliance on mature markets and improving overall mix.

- Analysts modelling this case build in share repurchases, steady margins and modest revenue growth to arrive at a fair value of US$78.30, with risks concentrated around China demand, input costs and macro uncertainty in key regions.

Fair value in this bearish narrative: US$62.00

Implied premium to this fair value at the recent US$64.82 share price: about 4.6%.

Revenue growth assumption: 3.81%.

- This view leans on a lower fair value of US$62.00, using a future P/E of 15.7x that sits below the Building industry level and below the current multiple used in the bullish case.

- Even with revenue growth of 3.81% and a margin uplift to 14.8%, the lower assumed P/E multiple and discount rate of 8.37% keep the implied value closer to the bottom end of analyst targets.

- Supportive factors such as high efficiency products, operational efficiency programs and capital returns are acknowledged, but the narrative treats these as already reflected in the price or not sufficient to justify a higher multiple.

Both narratives use the same current share price and similar growth ranges, yet arrive at different fair values by changing assumptions around margins, P/E multiples and perceived risk. Your job is to decide which set of assumptions feels closer to how you see A. O. Smith today and in the years ahead, then size any position accordingly and keep an eye on how the story and numbers move over time.

Do you think there's more to the story for A. O. Smith? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.