Is It Time To Reconsider Advance Auto Parts (AAP) After Its Sharp Share Price Rebound

Advance Auto Parts, Inc. AAP | 51.83 | -4.72% |

- If you are wondering whether Advance Auto Parts is a bargain or a value trap, its recent share price and fundamentals give you plenty to think about.

- The stock last closed at US$56.60, with returns of 11.6% over 7 days, 29.1% over 30 days, 45.5% year to date and 23.2% over 1 year, set against a 3 year return of negative 59.8% and a 5 year return of negative 59.0%.

- Recent news coverage has focused on how the company is repositioning itself in the competitive auto parts retail space and what that means for its long term profitability. Commentators have also discussed how these business updates relate to the stock’s sharp rebound over shorter periods compared with its weaker multi year track record.

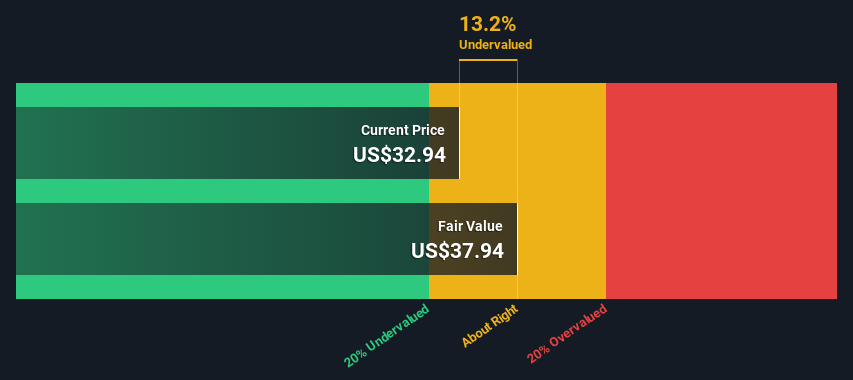

- On our valuation checks, Advance Auto Parts scores 2 out of 6, which you can see in more detail via this valuation score. Next we will walk through the main valuation methods investors often use, before coming to an even more helpful way to think about what the stock might be worth.

Advance Auto Parts scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Advance Auto Parts Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes projected future cash flows and discounts them back to today to estimate what the business might be worth right now. It is essentially asking what all future cash generated for shareholders is worth in today’s dollars.

For Advance Auto Parts, the latest twelve month free cash flow is a loss of $398.6 million. Analysts have a free cash flow estimate of $58.6 million for 2026, and Simply Wall St extends this with a 2 Stage Free Cash Flow to Equity model. This projects annual free cash flows out to 2035 using a mix of analyst input and extrapolated trends.

On this basis, the model arrives at an estimated intrinsic value of about $7.15 per share. Compared with the recent share price of $56.60, the DCF output suggests the stock is trading at a very large premium to this estimate. This implies it is very significantly overvalued using these cash flow assumptions.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Advance Auto Parts may be overvalued by 691.8%. Discover 51 high quality undervalued stocks or create your own screener to find better value opportunities.

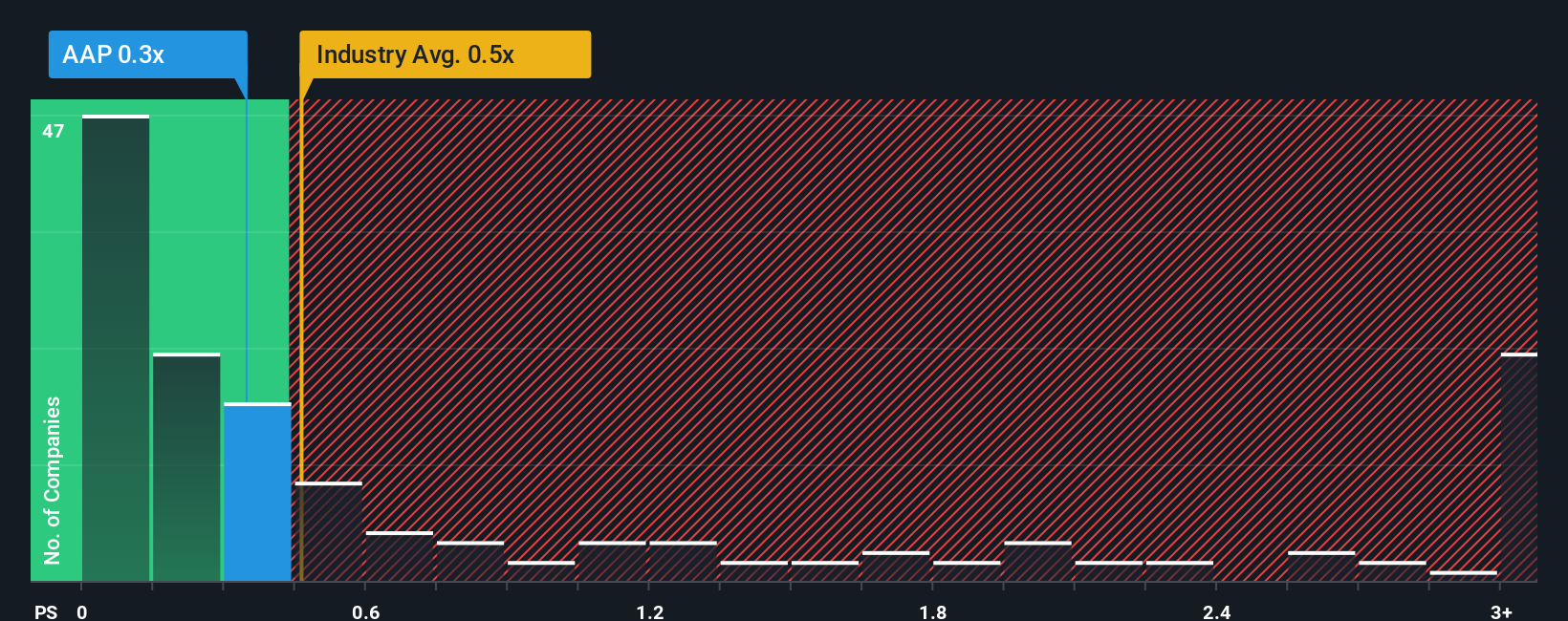

Approach 2: Advance Auto Parts Price vs Sales

For many established retailers, the P/S ratio is a useful cross check on value because it looks at what investors are paying for each dollar of revenue, which tends to be more stable than earnings in periods of weaker profitability.

In practice, investors usually expect higher growth and lower risk companies to justify a higher P/S multiple, while slower growing or higher risk businesses are often assessed at lower P/S levels. So what counts as a "normal" multiple often depends on expectations around growth, margins and earnings stability.

Advance Auto Parts currently trades on a P/S ratio of 0.39x. This sits below the Specialty Retail industry average of 0.48x, but above the peer group average of 0.20x. Simply Wall St’s Fair Ratio for the stock is 0.54x, which is its own estimate of an appropriate P/S taking into account factors such as the company’s earnings profile, industry, profit margins, market value and risk indicators.

Because the Fair Ratio blends these company specific inputs, it can be more informative than a simple comparison with peers or the overall industry. With the Fair Ratio of 0.54x sitting above the current 0.39x P/S, this framework points to the shares looking undervalued on a sales basis.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your Advance Auto Parts Narrative

Earlier we mentioned that there is an even better way to understand valuation. On Simply Wall St’s Community page you can use Narratives, where you write the story you believe about Advance Auto Parts, link that story to specific forecasts for revenue, earnings, margins and a fair value, then compare that fair value with the current price. As new information such as earnings or ARGOS product updates arrive, the platform refreshes the numbers. This allows you to see, for example, how one investor who thinks Advance Auto Parts is worth US$65.00 a share with revenue growth of about 2.29%, a 4.02% profit margin and a 14.91x future P/E might reach very different conclusions from another investor who sees fair value closer to US$34.51 with slower revenue growth of roughly 0.36%, a 3.42% margin and a 9.89x future P/E, even though both are looking at the same business.

For Advance Auto Parts, however, we will make it really easy for you with previews of two leading Advance Auto Parts Narratives:

Fair value: US$65.00 per share

Implied discount to this fair value at the last close of US$56.60: about 13%

Assumed annual revenue growth: 2.29%

- Focuses on automation, supply chain optimization and a shift to larger distribution centers as key drivers for higher margins and efficiency over several years.

- Assumes steady revenue growth supported by an ageing vehicle fleet, higher miles driven, a stronger Pro channel and an expanded private label offer such as ARGOS.

- Sees fair value at US$65.00 based on improved profit margins, higher earnings by 2028 and a future P/E of 14.91x. It also flags risks from electric vehicle adoption, digital underinvestment and competition.

Fair value: about US$51.29 per share

Implied premium to this fair value at the last close of US$56.60: about 10%

Assumed annual revenue growth: 1.77%

- Centers on a measured outlook where asset optimization, distribution consolidation and vendor partnerships are expected to lift margins, but only gradually.

- Works with more cautious assumptions for revenue growth and profit margins, taking into account store closures, weaker sales trends and the costs tied to restructuring.

- Arrives at a fair value of roughly US$51.29 per share using trimmed forecasts for earnings and a future P/E of about 15.40x. It also highlights risks from softer consumer demand, tariffs and lower gross margins during the transition.

Taken together, these previews show you how different assumptions about revenue, margins and risk can lead to very different views of what the same stock may be worth. If you want to see the full reasoning, including the detailed forecasts behind each view, you can jump straight into the community narratives for Advance Auto Parts using the bull and bear links above.

Do you think there's more to the story for Advance Auto Parts? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.