Is It Time To Reconsider V.F (VFC) After A 19% One-Year Share Price Rebound?

V.F. Corporation VFC | 0.00 |

- Wondering whether V.F at around US$17.28 is a bargain or a value trap? This article breaks down what the current price might be implying about the stock.

- The share price is down 9.3% over the past week and 8.1% over the past month. Over the last year it has delivered a 19.1% return, which may leave you questioning whether sentiment or fundamentals are in the driving seat.

- Recent coverage around V.F has focused on its long term share price record, including a 5 year period where the stock has fallen 75.9%. There is also interest in how management is repositioning the business and whether the balance sheet and dividend policy can support that shift. Together, these themes help explain why short term moves sit against a much more mixed multi year experience for shareholders.

- On Simply Wall St’s 6 point valuation framework V.F scores 3 out of 6. Next you will see how different valuation approaches line up and, at the very end, a way to get an even richer picture than price multiples alone can offer.

Approach 1: V.F Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock might be worth by projecting future cash flows and discounting them back to today’s value in $.

For V.F, the model uses a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is about $303.7 million. Analysts provide explicit forecasts for several years, and Simply Wall St then extends those projections further out. By 2029, free cash flow is projected at $843.4 million, with additional extrapolated estimates reaching into the early 2030s, all expressed and discounted back to today in $.

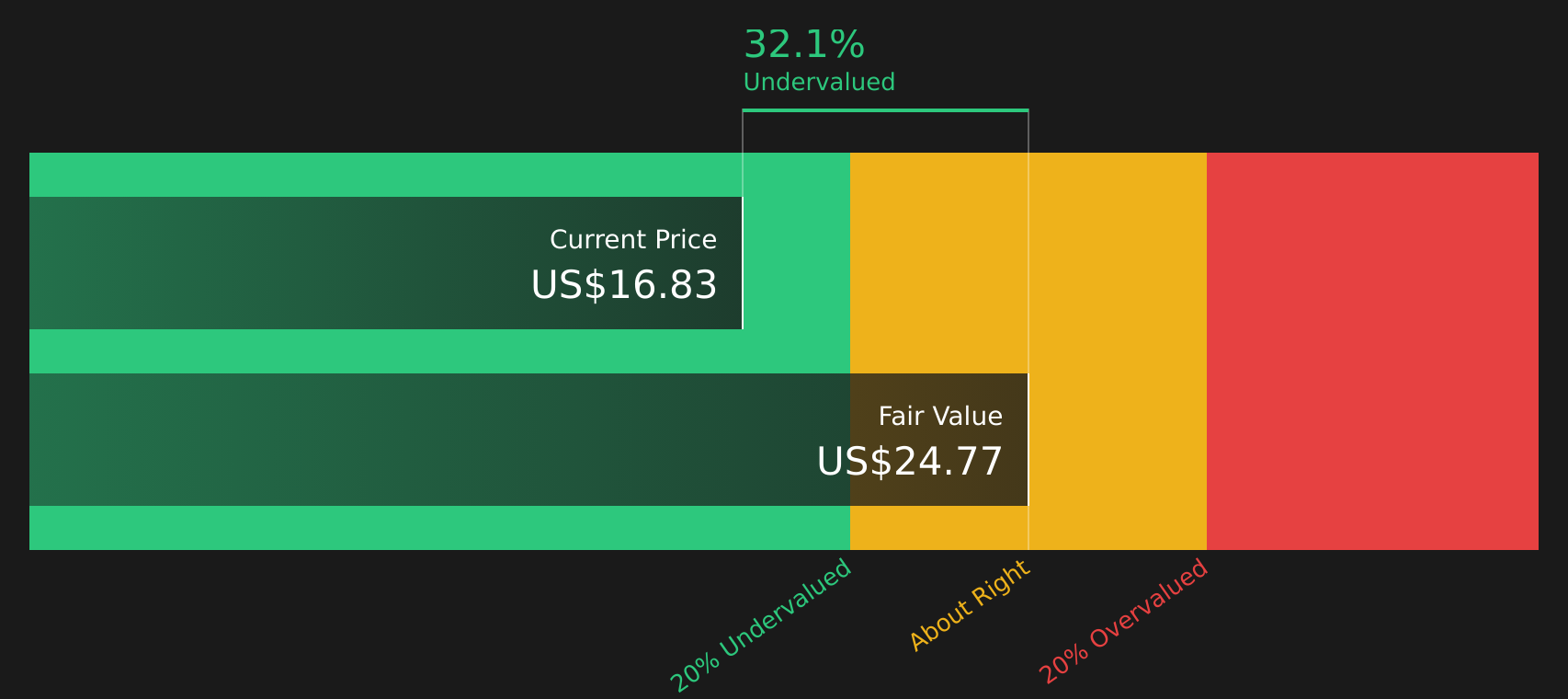

Pulling this together, the DCF model arrives at an intrinsic value of about $30.00 per share. Against a current share price of roughly $17.28, this implies the stock trades at a 42.4% discount to that estimate. On this cash flow view, V.F appears to be materially undervalued according to the model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests V.F is undervalued by 42.4%. Track this in your watchlist or portfolio, or discover 48 more high quality undervalued stocks.

Approach 2: V.F Price vs Earnings

For profitable companies, the P/E ratio is a useful shorthand for how much investors are currently paying for each dollar of earnings. It links directly to what the business is earning today, which many investors find easier to relate to than long range forecasts.

What counts as a “normal” or “fair” P/E depends on how fast earnings are expected to grow and how risky those earnings are perceived to be. Higher expected growth or lower perceived risk can justify a higher multiple, while slower growth or higher risk usually point to a lower one.

V.F currently trades on a P/E of about 30.19x. That sits above the Luxury industry average P/E of roughly 21.86x, but below the 48.11x average of its peer group. Simply Wall St also calculates a proprietary “Fair Ratio” for V.F of 27.49x, which reflects factors such as its earnings growth profile, industry, profit margin, market cap and company specific risks.

This Fair Ratio is more tailored than a simple comparison with peers or the sector because it blends those company specific drivers with industry context. When compared with the current P/E of 30.19x, the Fair Ratio suggests V.F may be slightly overvalued on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your V.F Narrative

Earlier it was mentioned that there is an even better way to understand valuation. This is where Narratives come in, a simple way for you to attach a clear story about V.F to the numbers you think are reasonable for its future revenue, earnings, margins and fair value, then see how that stacks up against the current price.

A Narrative links three things together in one place: the story you believe about the company, the forecast that flows from that story and the fair value that those assumptions imply.

On Simply Wall St, Narratives sit inside the Community page and are available to anyone. You can quickly see different fair values, compare them with today’s share price and use that gap between Fair Value and Price to help decide whether V.F looks more like an opportunity or something to be cautious about on your own terms.

These Narratives automatically refresh when new information appears, such as earnings reports or news. For example, if analysts lift their fair value for V.F to around US$31.42 at the optimistic end or keep it closer to US$14.00 at the cautious end, you can see how your own view compares and which story you feel more comfortable relying on.

For V.F however we'll make it really easy for you with previews of two leading V.F Narratives:

Fair value: US$20.70

Upside to this fair value vs last close at US$17.28: about 16.5%

Revenue growth assumption: 2.68%

- Analysts expect a gradual revenue lift supported by premiumization, digital channels and a tighter focus on higher margin brands.

- Margin improvement and free cash flow are tied to supply chain changes, inventory discipline and a leaner brand portfolio.

- This view lines up with an analyst consensus fair value around US$20.70, with investors asked to judge whether Vans recovery and execution can support those inputs.

Fair value: US$14.00

Downside to this fair value vs last close at US$17.28: about 23.4%

Revenue growth assumption: 2.23%

- More cautious analysts highlight pressure on legacy brands, especially Vans, and question how much turnaround efforts can offset demand and margin headwinds.

- This view frames higher environmental, promotional and competitive costs as lasting forces that could keep profitability under strain.

- On this narrative, a fair value of US$14.00 assumes V.F eventually earns more but at a much lower P/E multiple than today, as expectations for brand recovery and valuation are reset.

If you want to go beyond these previews and see how other investors are joining the dots between stories, assumptions and fair values, it is worth spending time with the full set of Narratives on V.F, including different risk and valuation angles in one place.To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for V.F on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for V.F? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.