Is It Too Late To Consider Alliant Energy (LNT) After Strong Five-Year Share Gains?

Alliant Energy Corporation LNT | 72.85 | +1.26% |

- If you are wondering whether Alliant Energy's current share price still offers value or if most of the opportunity is already priced in, this article walks through the key pieces you need to consider.

- The stock last closed at US$70.81, with returns of 5.8% over 30 days, 8.0% year to date, 17.5% over 1 year, 47.7% over 3 years, and 61.0% over 5 years. This performance may have shifted how investors think about its risk and return profile.

- Recent coverage of Alliant Energy has focused on its role as a regulated utility and how investors are weighing its longer term prospects and income profile against current pricing. These themes help frame why the recent share price performance is getting more attention from investors who follow steady, dividend focused companies.

- On Simply Wall St's valuation checks, Alliant Energy currently scores 1 out of 6 for being undervalued. Next, we will look at how standard valuation approaches line up for the stock and then finish with a broader way to think about what that score really means for you.

Alliant Energy scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

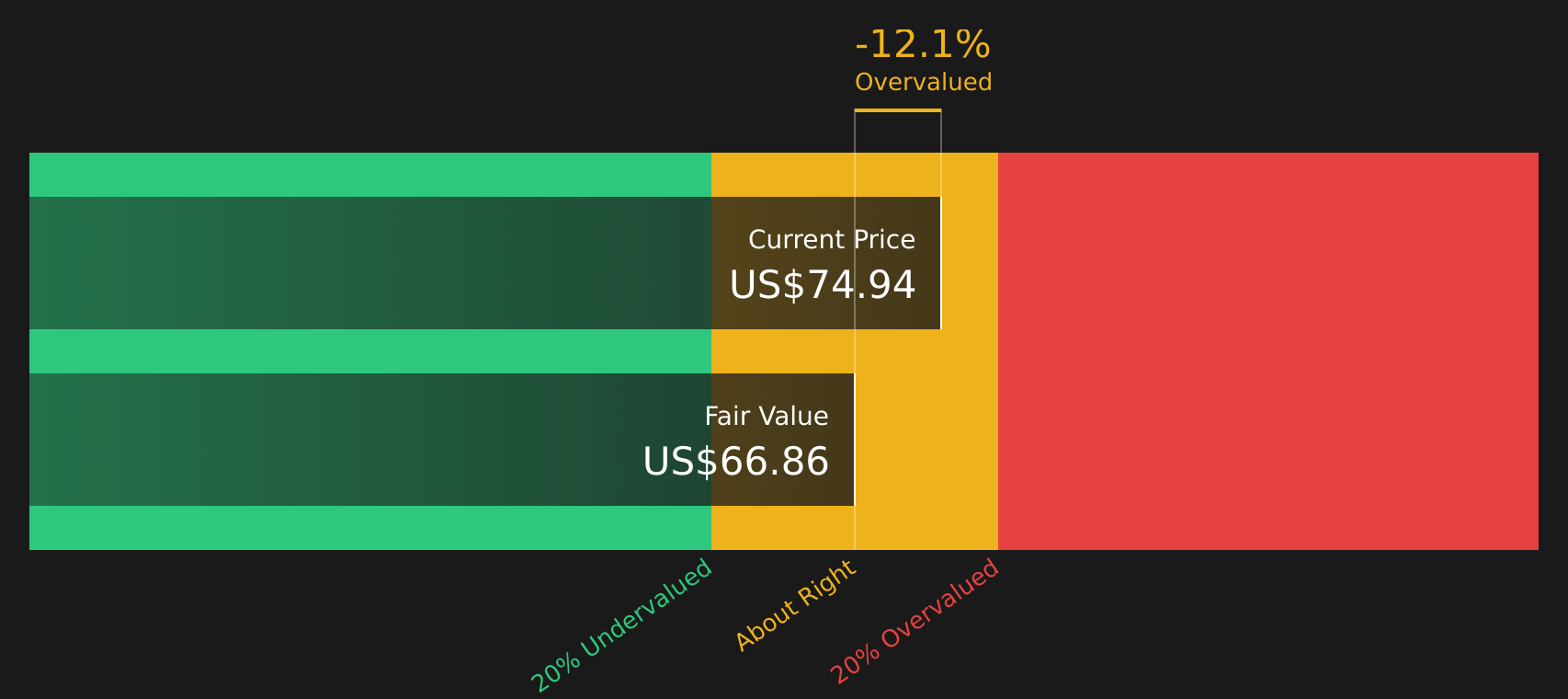

Approach 1: Alliant Energy Dividend Discount Model (DDM) Analysis

The Dividend Discount Model looks at the dividends a company is expected to pay over time, then discounts those cash flows back to today to estimate what the shares might be worth.

For Alliant Energy, Simply Wall St uses a recent annual dividend per share of about US$2.40, a return on equity of 10.62% and a payout ratio of roughly 66%. The model applies a long term dividend growth rate of 3.41%, which is capped from an initial 3.60%, and an expected growth rate of 3.60% to keep the assumptions on the conservative side.

Using these dividend and growth inputs, the DDM output suggests an intrinsic value of US$67.14 per share. Compared with the recent share price of US$70.81, that implies the stock is about 5.5% richer than the model’s estimate, which sits in a fairly tight range rather than a glaring mispricing.

Result: ABOUT RIGHT

Alliant Energy is fairly valued according to our Dividend Discount Model (DDM), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Alliant Energy Price vs Earnings

The price to earnings, or P/E ratio, is a common way to think about value for profitable companies because it links what you pay for each share to the earnings that back it. In general, higher expected growth and lower perceived risk can support a higher P/E, while lower growth or higher risk usually mean a lower, more cautious P/E feels appropriate.

Alliant Energy is currently trading on a P/E of 22.48x. That sits above the Electric Utilities industry average of 21.22x and above the peer group average of 17.09x, so the stock is priced at a premium compared with both its sector and similar companies.

Simply Wall St also calculates a proprietary “Fair Ratio” of 24.17x. This is designed to reflect what P/E might make sense for Alliant Energy once you account for factors such as its earnings profile, industry, profit margins, market value and key risks. Because it is tailored to the company, the Fair Ratio can be more informative than a simple comparison with peers or the broad industry.

Put side by side, the Fair Ratio of 24.17x is higher than the current P/E of 22.48x, indicating the shares are somewhat below that modelled level.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Alliant Energy Narrative

Earlier we mentioned that there is an even better way to understand valuation. Narratives let you pair your own story about Alliant Energy with the numbers you believe are reasonable for future revenue, earnings and margins. You can then link that story to a forecast and a fair value, and compare that fair value with the current price to help you decide when to buy or sell. All of this happens inside Simply Wall St’s Community page, where millions of investors share their views. Each Narrative updates automatically when new information like earnings or news arrives. For example, one investor might build a Narrative that leans toward the higher US$74.50 fair value based on confidence in data center demand and earnings guidance, while another might lean toward the lower US$60.00 view because they place more weight on risks around regulation, capital needs and project execution.

Do you think there's more to the story for Alliant Energy? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.