Is It Too Late To Consider CRH (NYSE:CRH) After Its Recent Share Price Jump?

CRH public limited company CRH | 0.00 |

- If you are wondering whether CRH at around US$115 a share still offers value, or if most of the easy gains are already behind it, this article focuses squarely on what the current price might mean for you.

- The stock has delivered a 10.3% return over the past 30 days and 18.4% over the last year, while also showing a 2.2% decline over the past week and an 8.7% decline year to date.

- Recent headlines around CRH have focused on its position as a major player in construction materials and on how investors are reassessing large infrastructure related names in the sector. This backdrop has helped shape sentiment around the stock and provides important context for the recent moves in its share price.

- CRH currently has a valuation score of 3 out of 6. This suggests that some checks point to undervaluation while others do not. Next comes a closer look at traditional valuation approaches, followed by a different way to think about what the market might be pricing in.

Approach 1: CRH Discounted Cash Flow (DCF) Analysis

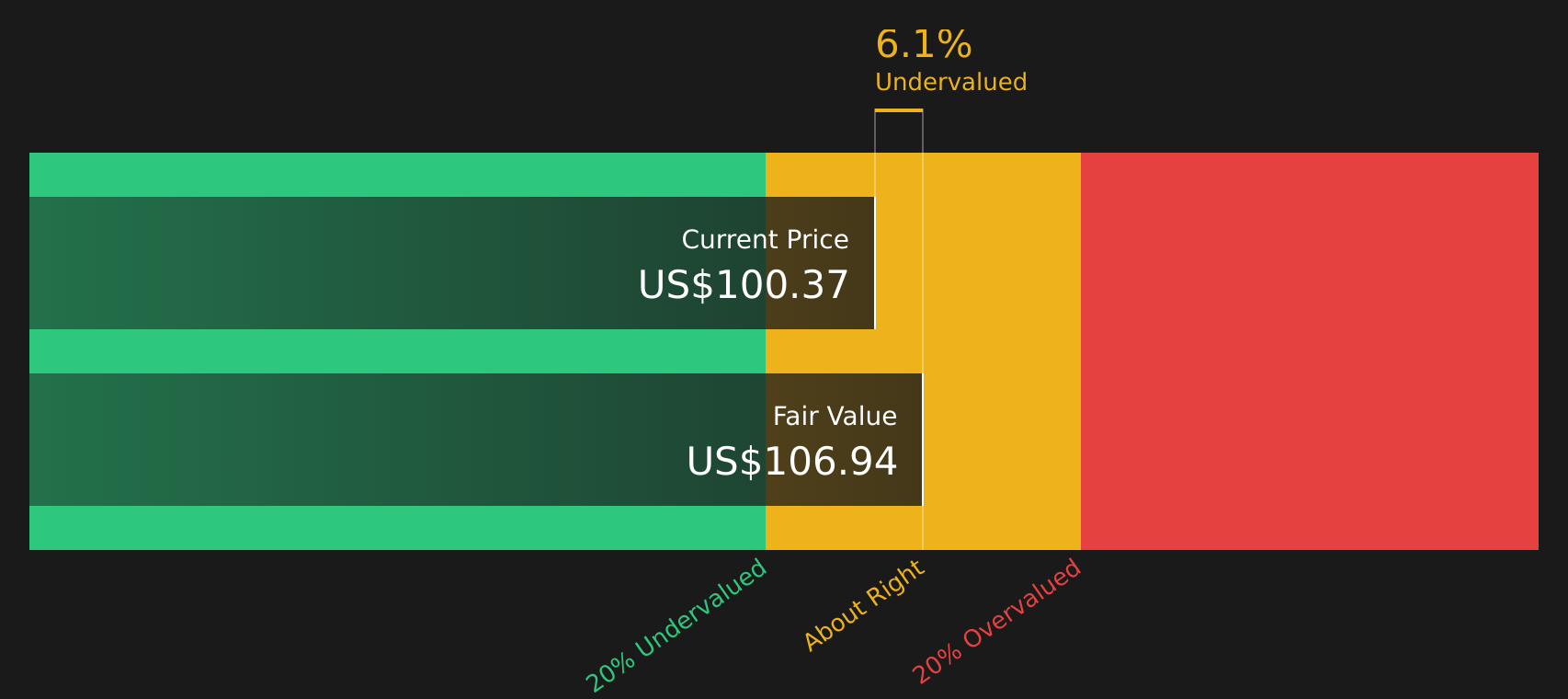

A Discounted Cash Flow, or DCF, model takes estimates of the cash CRH could generate in the future and discounts those amounts back to a single value in today’s dollars. It is a way of asking what those future cash flows might be worth right now.

For CRH, the latest twelve month Free Cash Flow is about $3.09b. Using a 2 Stage Free Cash Flow to Equity model that projects cash flows out over the coming years, analysts see Free Cash Flow of $4.78b by 2030. Estimates up to 2030 blend analyst forecasts through 2029 and then extrapolated figures after that point, with all numbers kept in dollar terms.

When those projected cash flows are discounted back, the model points to an intrinsic value of about $106.42 per share. Compared with a share price around $115, the DCF output suggests CRH trades at roughly an 8.5% premium, which is a relatively small gap that puts it close to the model’s estimate of fair value.

Result: ABOUT RIGHT

CRH is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

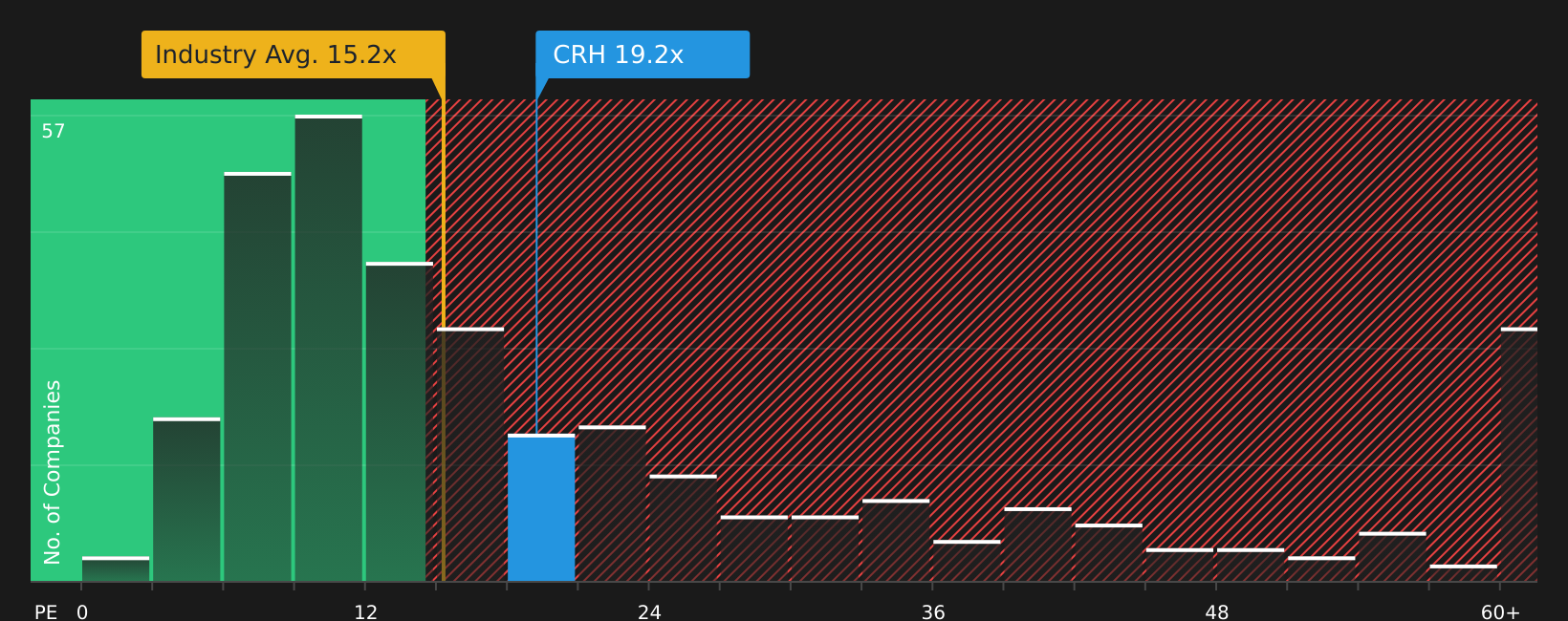

Approach 2: CRH Price vs Earnings

P/E is a common way to value profitable companies because it connects what you pay for each share with the earnings that support that price. A higher P/E often reflects higher expected growth or lower perceived risk, while a lower P/E can point to lower growth expectations or higher risk.

CRH currently trades on a P/E of 21.15x. That sits above the Basic Materials industry average of 15.65x, but below the peer group average of 30.44x. On the surface, this positions CRH between the broader sector and more highly rated peers.

Simply Wall St’s Fair Ratio for CRH is 25.72x. This is a proprietary estimate of what the P/E might look like after considering factors such as earnings growth, profit margins, industry, market cap and company specific risks. Because it blends these elements into a single benchmark, it can be more tailored than a simple comparison against industry or peer averages.

Comparing CRH’s actual P/E of 21.15x with the Fair Ratio of 25.72x suggests the shares trade below that customised benchmark.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your CRH Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St’s Community page let you turn your view of CRH into a clear story that links what the business is doing to a forecast and a fair value. They update that story automatically when fresh news or earnings arrive and help you compare that fair value with the current price. For example, one investor might build a bullish CRH Narrative that lines up with the US$163 analyst target using higher revenue, margin and P/E assumptions. Another might lean toward the US$105 view with more cautious assumptions. Both can see in one place how their story, numbers and implied fair value fit together.

Do you think there's more to the story for CRH? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.