Is It Too Late To Consider Entegris (ENTG) After Its Recent Share Price Surge?

Entegris, Inc. ENTG | 0.00 |

- If you are wondering whether Entegris is priced for opportunity or already reflecting high expectations, it helps to start by looking at how the market has been treating the stock recently and how that lines up with its fundamentals.

- Entegris shares last closed at US$130.90, with returns of 18.6% over 7 days, 28.2% over 30 days, 46.2% year to date, 20.8% over 1 year, 52.2% over 3 years and 30.6% over 5 years.

- Recent price moves sit against a backdrop of ongoing interest in semiconductor related names, including companies involved in materials and equipment for chip production. For Entegris, this context helps explain why investors are paying close attention to its role in the broader supply chain and how that might relate to the price they are willing to pay.

- Simply Wall St currently gives Entegris a valuation score of 0/6. Next, we will look at how different valuation approaches view the stock and then finish with a way of assessing value that goes beyond any single model.

Entegris scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Entegris Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes estimates of a company’s future cash flows and discounts them back to today using a required rate of return, to arrive at an estimate of what the business might be worth per share right now.

For Entegris, Simply Wall St uses a 2 Stage Free Cash Flow to Equity model, starting from last twelve months free cash flow of about $351.5 million. Analyst projections and subsequent estimates extend that to a forecast free cash flow of $850.3 million in 2030, with further years extrapolated rather than based on direct analyst coverage.

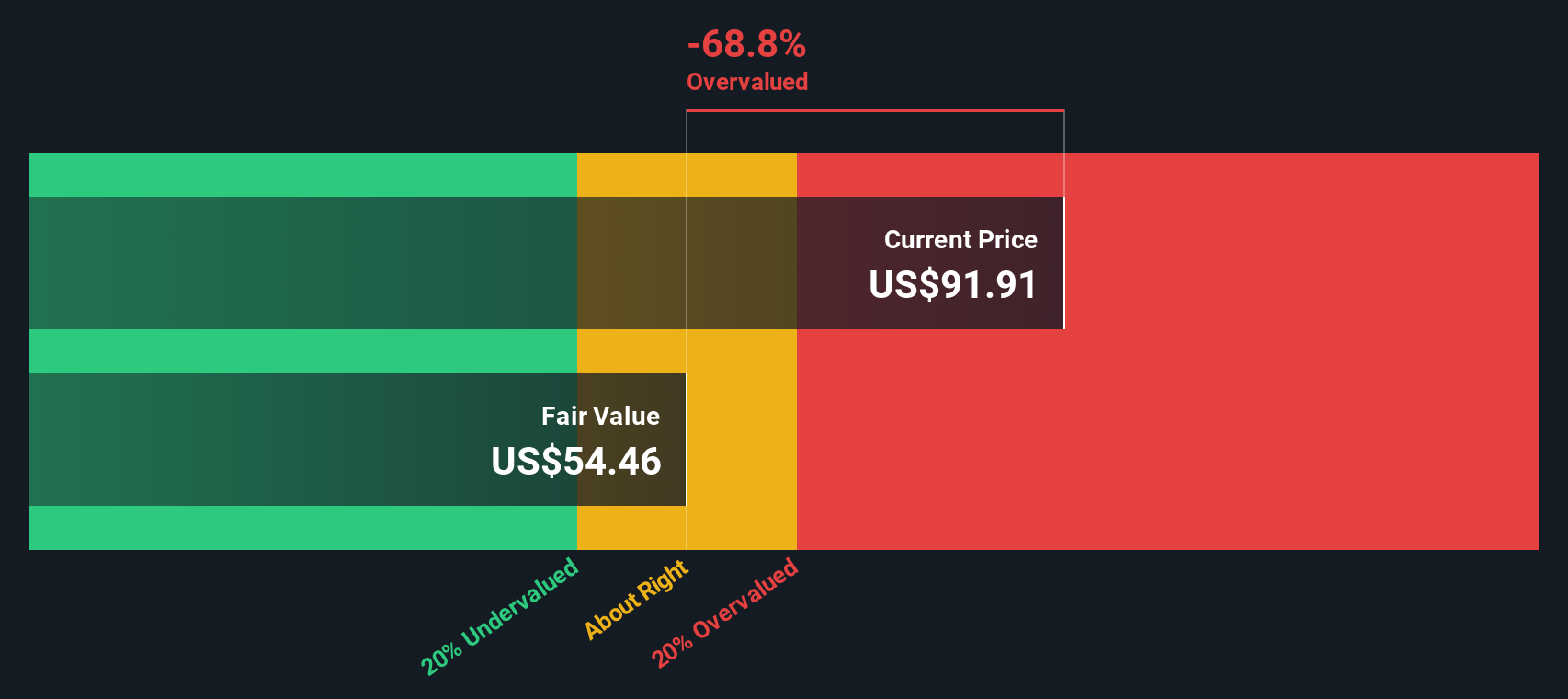

When all those projected cash flows in dollars are discounted back and summed, the model produces an estimated intrinsic value of about $68.22 per share. Compared with the recent share price of US$130.90, the model suggests the stock is about 91.9% overvalued on this DCF view. In other words, the current market price sits well above what this particular cash flow based approach implies.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Entegris may be overvalued by 91.9%. Discover 55 high quality undervalued stocks or create your own screener to find better value opportunities.

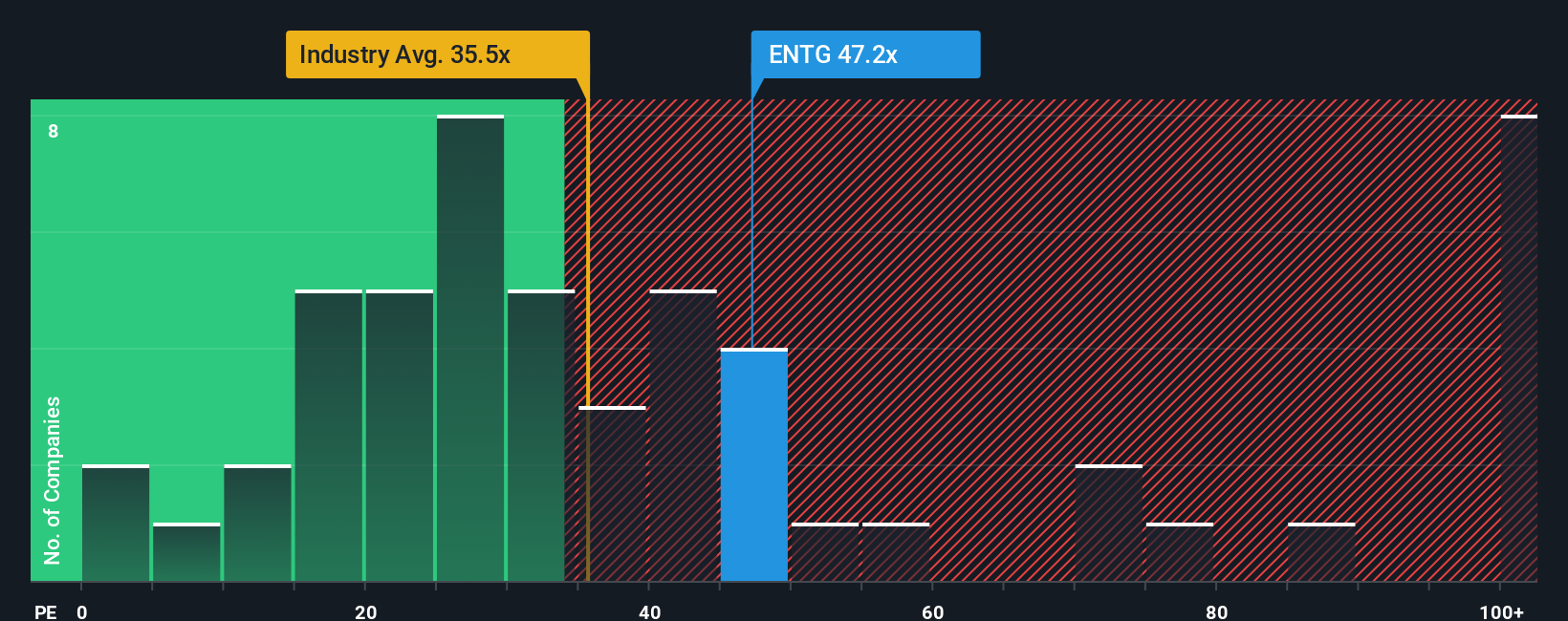

Approach 2: Entegris Price vs Earnings

For profitable companies, the P/E ratio is a useful yardstick because it links what you pay for each share to the earnings that business is currently generating. The higher the growth expectations and the lower the perceived risk, the more investors are usually willing to pay in terms of a higher P/E, and the reverse also holds.

Entegris is currently trading on a P/E of 84.40x. That sits above the Semiconductor industry average of about 43.24x and the peer average of 45.83x, so on simple comparisons the shares are priced at a richer multiple than many sector peers.

Simply Wall St’s Fair Ratio for Entegris is 41.42x. This is a proprietary estimate of what a reasonable P/E might be, given factors such as the company’s earnings growth profile, profit margins, industry, market cap and specific risks. Because it adjusts for these company level characteristics instead of just lining Entegris up against broad peer or industry averages, the Fair Ratio aims to give a more tailored view of what investors might expect to pay.

Comparing the current P/E of 84.40x to the Fair Ratio of 41.42x suggests the shares are trading well above that tailored benchmark.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your Entegris Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce Narratives. With Narratives, you set a story for Entegris, link that story to simple forecasts for revenue, earnings and margins, and then see what fair value drops out and how it compares to today’s price.

On Simply Wall St’s Community page, Narratives are an easy tool used by millions of investors. They let you plug in your own assumptions, see a fair value estimate, and quickly compare that to the current share price to help you evaluate whether the stock looks expensive or cheap on your numbers.

Narratives also stay fresh, because when new information such as earnings, guidance or news is added, the underlying data and fair value are refreshed so your story does not get stuck on old numbers.

For Entegris, one investor might build a Narrative that lines up with the higher fair value of about US$150.00, while another might lean toward the lower fair value of about US$75.00. Seeing both side by side can make it easier for you to decide which story, and which implied fair value, feels closer to your own view.

For Entegris however we will make it really easy for you with previews of two leading Entegris Narratives:

Fair value in this bullish narrative: US$150.00 per share

Current price vs this fair value: about 12.8% below the narrative fair value

Revenue growth used in this narrative: 7.22% a year

- The bullish author focuses on Entegris’ role in advanced semiconductor materials, with AI, 5G, automotive and broader digital demand supporting a larger content opportunity per wafer over time.

- They highlight a wide, global manufacturing footprint and product development in areas such as molybdenum deposition and advanced wet chemistries as key to supporting margins and customer reliance.

- On the risk side they flag tariffs, cyclicality, debt of about US$4b and customer purchasing behavior as factors that could still pressure profitability and cash flow if conditions become less favorable.

Fair value in this bearish narrative: US$75.00 per share

Current price vs this fair value: about 74.5% above the narrative fair value

Revenue growth used in this narrative: 6.13% a year

- The bearish author focuses on geopolitics, tariffs and regulatory shifts that could limit access to key markets such as China and lead to lasting revenue and margin pressure.

- They point to rising competition, potential commoditization in some product lines and higher compliance and supply chain costs as headwinds for sustained margin expansion.

- In their view, semiconductor cyclicality, slower fab build outs and the risk of product obsolescence mean Entegris may not justify a premium P/E without stronger evidence that earnings volatility and execution risks are contained.

Seeing these two Entegris Narratives side by side gives you clear guardrails so you can decide which assumptions feel closer to your own view on the company’s risks, growth profile and the price you are comfortable paying for the stock.

Do you think there's more to the story for Entegris? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.