Is It Too Late To Consider First Solar (FSLR) After Its Strong Multi Year Run

First Solar, Inc. FSLR | 0.00 |

- If you are wondering whether First Solar at around US$214.57 is still good value after its strong run, this article walks through what the current price actually reflects.

- The stock has moved 6.3% over the last 7 days, 11.6% over 30 days, 60.4% over 1 year and 208.4% over 5 years. Year to date, the return stands at a 21.8% decline, which can change how you think about both upside and risk.

- Recent coverage has focused on First Solar as part of ongoing interest in US-listed solar and semiconductor related companies. Investors are paying closer attention to how policy support and capital spending trends may influence the sector. This backdrop helps explain why the stock has seen periods of strong gains as well as pullbacks within the broader trend.

- Simply Wall St currently gives First Solar a valuation score of 4 out of 6, reflecting where it screens as undervalued on several checks. Next you will see how different valuation methods line up, followed by a closing section on an even clearer way to think about what fair value might mean for you.

Approach 1: First Solar Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes the cash flows a company is expected to generate in the future and discounts them back to what they might be worth today, using a required rate of return. It is essentially asking what those future dollars are worth in today’s terms.

For First Solar, the latest twelve month Free Cash Flow is about $1.01b. Using a 2 Stage Free Cash Flow to Equity model, analysts provide explicit cash flow estimates through 2030, and Simply Wall St extrapolates further projections beyond that. Within these projections, annual Free Cash Flow figures run in the low to mid single digit billions of dollars, with discounted values that reflect the time value of money.

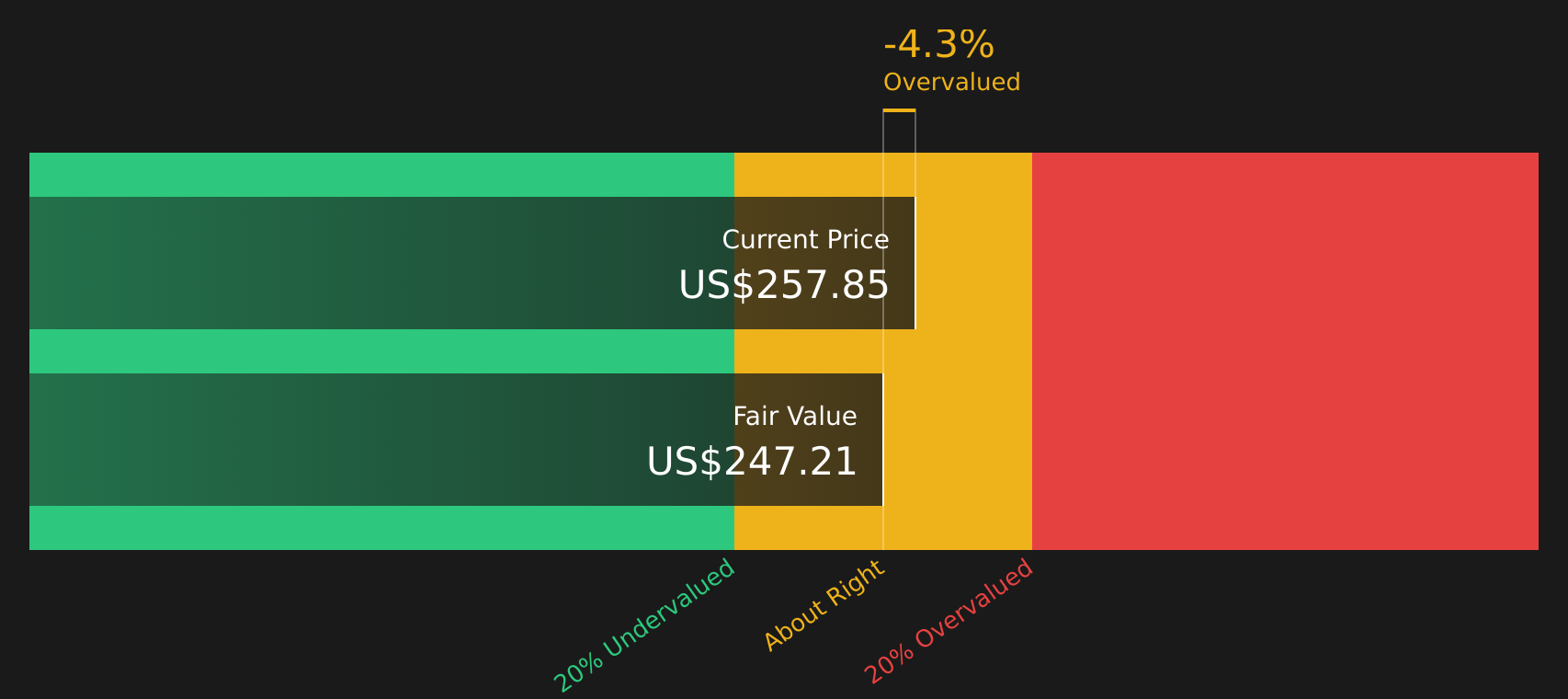

Putting all of these discounted cash flows together gives an estimated intrinsic value of $246.85 per share. Compared with the recent share price of about $214.57, the DCF suggests the stock trades at roughly a 13.1% discount, which indicates it may be undervalued on this measure.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests First Solar is undervalued by 13.1%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: First Solar Price vs Earnings

For profitable companies, the P/E ratio is a useful way to think about what you are paying for each dollar of current earnings. It ties the share price directly to the business’ ability to generate profit, which is often a core driver of long term returns.

What counts as a “normal” P/E depends on how the market views a company’s growth outlook and risk profile. Higher expected growth or lower perceived risk can support a higher multiple, while slower expected growth or higher risk usually leads to a lower one.

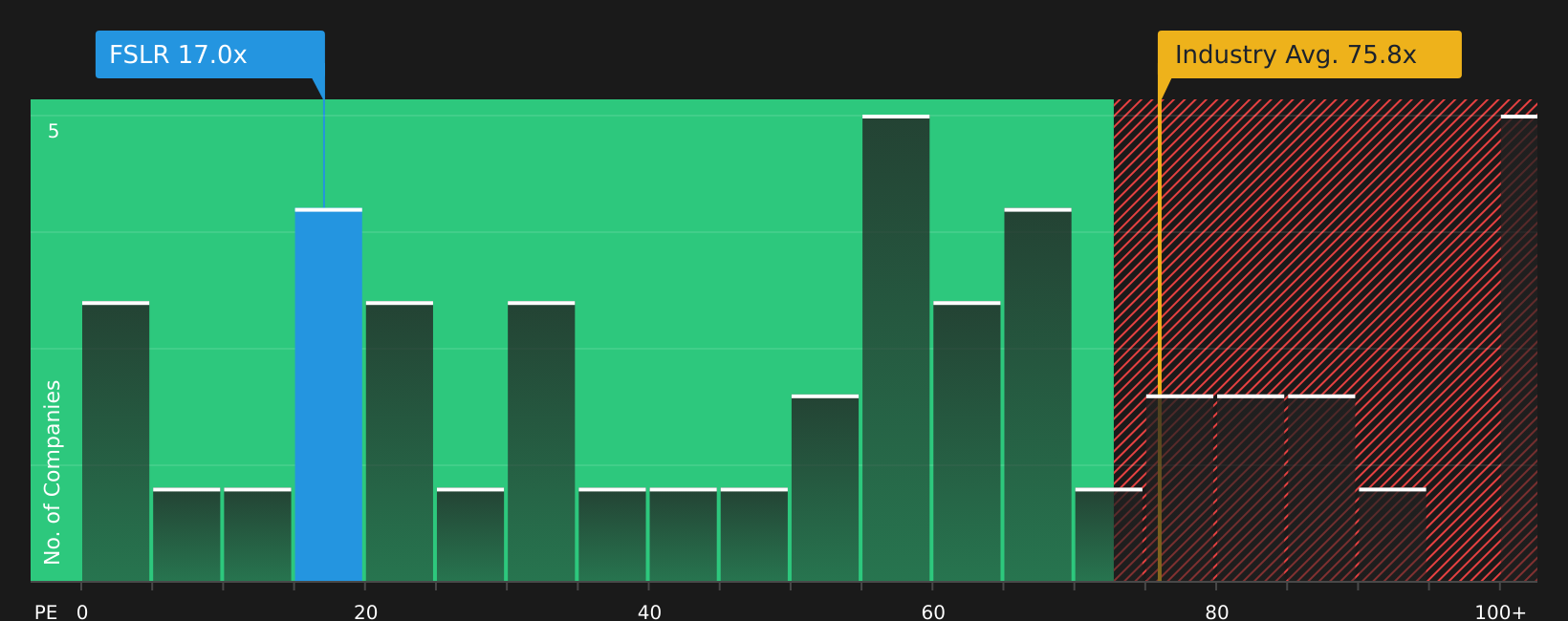

First Solar currently trades on a P/E of 13.85x. That sits well below the Semiconductor industry average of 53.66x and the peer average of 90.77x. Simply Wall St’s Fair Ratio for First Solar is 41.30x, which is a proprietary estimate of the P/E that could be reasonable given factors such as earnings growth, profit margins, industry, market cap and company specific risks.

The Fair Ratio is more tailored than a simple comparison with peers or the broad industry because it attempts to line up the multiple with company specific fundamentals rather than broad group averages. Since 13.85x is below the 41.30x Fair Ratio, this method points to the stock screening as undervalued on earnings.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your First Solar Narrative

Earlier it was mentioned that there is an even better way to think about valuation. This is where Narratives come in, letting you attach a clear story about First Solar to the numbers by linking your view on its future revenue, earnings and margins to a financial forecast and then to a Fair Value that you can compare with the current price.

On Simply Wall St’s Community page, Narratives are an accessible tool used by millions of investors. Each investor can set assumptions and see a live Fair Value that updates automatically when new information such as earnings or policy news is added, so your view on First Solar does not stay static.

The range of Narratives already visible for First Solar shows how perspectives can differ. One investor sets Fair Value near US$155.98 and another closer to US$313.00. This gives you a concrete sense of how different stories and assumptions about growth, margins, risk and required return translate into very different Fair Values and potential investment decisions.

For First Solar however, we will make it really easy for you with previews of two leading First Solar narratives:

On one side, you have a bullish view that leans heavily on policy support, domestic buildout and contracted cash flows. On the other, a more cautious take that highlights execution risks, supply constraints and policy dependence. Looking at both can help you decide which story feels closer to your own expectations.

Fair value: US$281.65 per share

Implied discount to this fair value: 23.8% versus the recent price of about US$214.57

Revenue growth used in this narrative: 12.54%

- Emphasis on U.S. policy support, Section 232 trade actions and domestic manufacturing capacity as key supports for pricing, margins and contracted volumes.

- Large contracted backlog and thin film technology focus are used to support long term revenue visibility, profitability and an updated fair value of about US$281.65.

- Analyst research referenced in this narrative weighs policy tailwinds against trade and execution risks, yet still arrives at a higher internal fair value than the current share price.

Fair value: US$180.44 per share

Implied premium to this fair value: 18.9% versus the recent price of about US$214.57

Revenue growth used in this narrative: 13%

- Highlights that a large part of the investment case relies on strong policy support, high tariffs and tax credits, which leaves the business exposed if incentives change.

- Points to material cost and supply risks around tellurium, as well as operational issues like plant underutilisation and CuRe ramp up challenges that can pressure margins.

- Flags that competition, potential price pressure and policy or trade shifts could limit how much value current projects and capacity expansions ultimately deliver for shareholders.

Putting these side by side gives you a practical range. If your own assumptions sit closer to the bullish story, the higher fair value may feel more reasonable, while if you lean toward the cautious view, the lower fair value may feel more appropriate. Either way, using clear narratives like these can help you stay consistent when new data, guidance or policy news arrives and forces you to revisit your thesis.

Do you think there's more to the story for First Solar? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.