Is It Too Late To Consider Howmet Aerospace (HWM) After A 74% One Year Surge?

Howmet Aerospace Inc. HWM | 232.68 | -2.66% |

- If you are wondering whether Howmet Aerospace's share price still reflects its underlying value after a strong run, you are not alone. This article is designed to walk you through that question step by step.

- The stock last closed at US$224.47, with returns of 5.1% over 7 days, 2.8% over 30 days, 6.0% year to date and 74.0% over 1 year, while the 3 year return is very large and the 5 year return is around 7x.

- These share price moves sit against a backdrop of ongoing investor attention on aerospace and defense suppliers, with Howmet often cited in market commentary around demand for aircraft components and related equipment. Broader sector headlines about supply chains, defense spending and airline fleet upgrades have all helped frame how investors think about companies in this space.

- Despite that backdrop, Howmet currently has a valuation score of 0 out of 6, which means none of our six valuation checks flag it as undervalued. Next we will walk through the usual tools like P/E, cash flows and asset-based measures, then finish with a more holistic way to think about what the market is really pricing in.

Howmet Aerospace scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

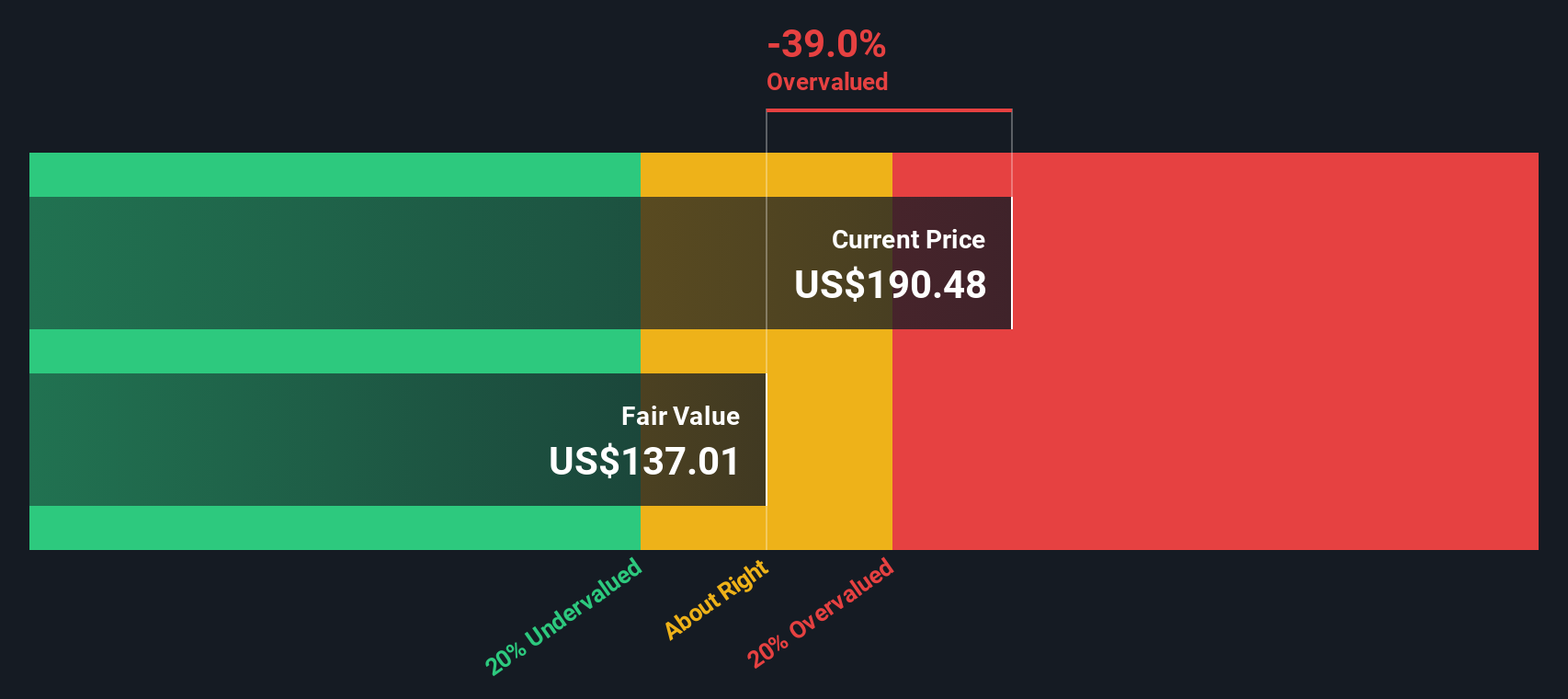

Approach 1: Howmet Aerospace Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes projected future cash flows and discounts them back to today to estimate what the company might be worth at present.

For Howmet Aerospace, the latest twelve month Free Cash Flow (FCF) is about $1.37b. Using a 2 Stage Free Cash Flow to Equity model, analysts provide explicit FCF estimates for the next few years, and Simply Wall St then extrapolates those numbers further out. Under this framework, projected FCF in 2029 is $2.70b, with additional projections extending out to 2035.

When all those future cash flows are discounted back and added up, the model arrives at an estimated intrinsic value of US$171.39 per share. Compared to the recent share price of US$224.47, the DCF output indicates that the stock trades at roughly a 31.0% premium to this intrinsic value, which suggests that Howmet may be overvalued on this specific cash flow model.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Howmet Aerospace may be overvalued by 31.0%. Discover 51 high quality undervalued stocks or create your own screener to find better value opportunities.

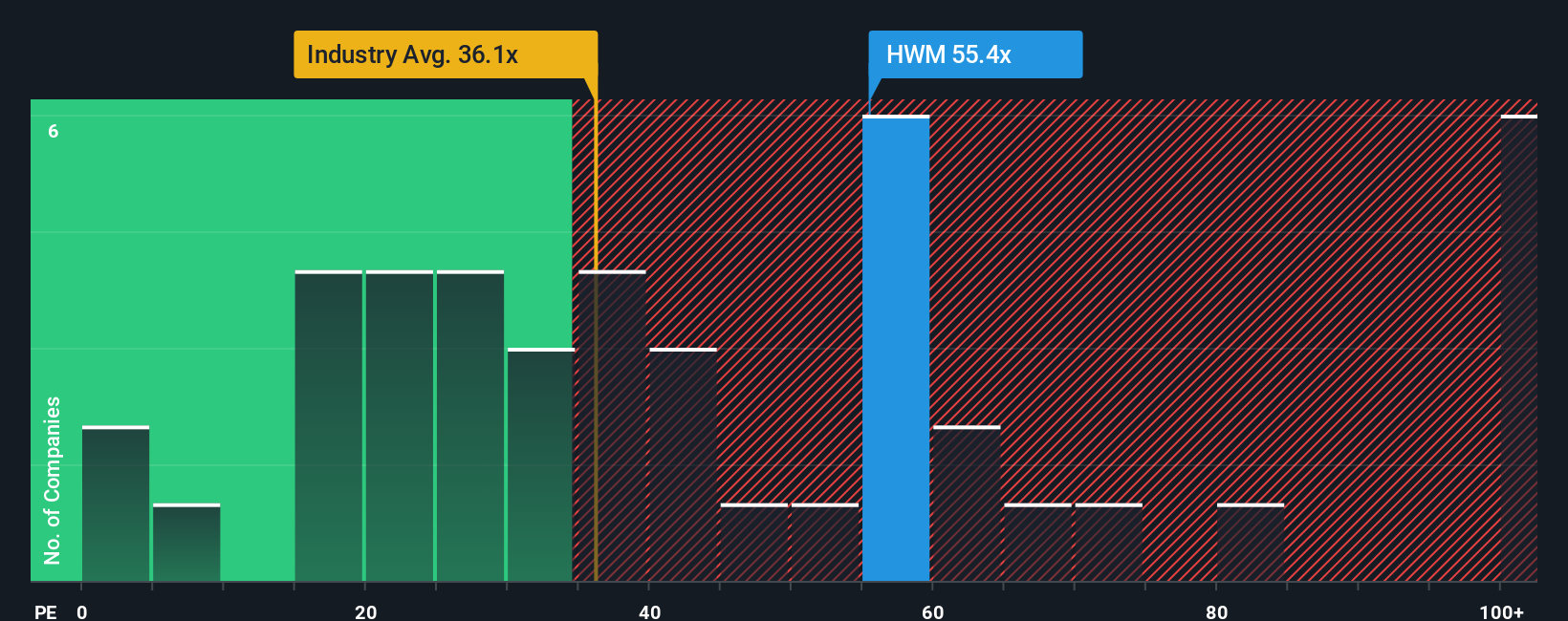

Approach 2: Howmet Aerospace Price vs Earnings

For profitable companies, the P/E ratio is a useful shortcut because it links what you pay for each share directly to the earnings that company is currently generating. It gives you a quick way to see how much investors are willing to pay for every dollar of profit.

What counts as a "normal" or "fair" P/E depends on what the market expects for growth and how risky those earnings appear. Higher expected growth or lower perceived risk can justify a higher P/E, while lower growth or higher risk usually calls for a lower one.

Howmet Aerospace currently trades on a P/E of 62.33x. That sits above both the Aerospace & Defense industry average P/E of 41.86x and the peer average of 31.86x. Simply Wall St also calculates a proprietary “Fair Ratio” of 39.21x, which aims to capture what a suitable P/E might look like once you factor in earnings growth, profit margins, industry, market cap and risk profile. This Fair Ratio can be more tailored than a simple comparison to peers or the broad industry because it accounts for company specific characteristics. With the current P/E of 62.33x versus the Fair Ratio of 39.21x, the shares appear expensive on this measure.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your Howmet Aerospace Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, which are simple stories you and other investors build around Howmet Aerospace that link assumptions about future revenue, earnings, margins and a fair value to a clear view of whether the current price looks high or low.

On Simply Wall St’s Community page, Narratives give you an easy way to spell out your view of the company, connect it to a financial forecast, and see the implied fair value. You can then compare this with the live share price to help decide whether you are more comfortable buying, holding or selling at today’s level.

Because Narratives on the platform update when fresh information such as news or earnings is added, you can see how different investors respond. For example, one Howmet Aerospace narrative currently implies a fair value of about US$285.78, while another is closer to US$121.54, and a third sits around US$233.70. This shows how the same company can look very different depending on the story and numbers you think are most realistic.

For Howmet Aerospace however we will make it really easy for you with previews of two leading Howmet Aerospace Narratives:

First up is a bullish take that leans on margin expansion and higher value end markets.

Fair value: US$233.70 per share

Implied discount to fair value: about 3.9% premium to this narrative fair value at the recent price of US$224.47

Assumed revenue growth: 10.38% per year

- Analysts in this camp expect strong demand from commercial and defense aerospace, newer fuel efficient aircraft and engine spares to support higher revenue and net margins.

- They point to capacity expansions, automation and productivity gains as reasons earnings and margins could be resilient over time.

- Key watchpoints include high capital spending, reliance on major aerospace customers and the risk that spares and industrial gas turbine demand tied to data centers does not meet expectations.

On the other side you have a more cautious view that puts more weight on execution risks and capital intensity.

Fair value: US$121.54 per share

Implied premium to fair value: about 84.6% over this narrative fair value at the recent price of US$224.47

Assumed revenue growth: 7.27% per year

- This narrative assumes more conservative narrow body aircraft demand and potential production challenges, which could affect revenue and operating margins.

- Higher capital expenditure and headcount growth are seen as possible drags on cash flow and margins, especially with ongoing buybacks and dividends.

- Supportive factors include solid financial health and investments in key segments, but the overall view is that the share price leaves less room for disappointment if growth or profitability are weaker than hoped.

Taken together, these Narratives give you a structured way to decide which story feels closer to your own expectations, then judge whether the current price of US$224.47 lines up with that view or not.

Do you think there's more to the story for Howmet Aerospace? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.