Is It Too Late To Consider Maase (MAAS) After A 64% Monthly Surge?

Maase Inc MAAS | 0.00 |

- Wondering whether Maase at US$9.30 is priced for opportunity or already reflecting expectations? This article walks through what the current valuation suggests about the stock.

- Over the last month, the share price return of 64.0% and a year-to-date return of 59.7%, despite a 4.1% decline over the past week, indicate that the market's view on the stock has been shifting quickly.

- Recent coverage around Maase has focused on its positioning within the insurance sector and how investors are reacting to changing expectations about the business. This context helps explain why the share price has moved sharply in a short period and why some investors are now questioning whether the stock still appears attractively valued.

- Despite these moves, Maase currently has a valuation score of 0 out of 6. The rest of this article will unpack what traditional approaches like DCFs and multiples suggest about the current price, and then finish with a more complete way to think about valuation that ties all of these signals together.

Maase scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

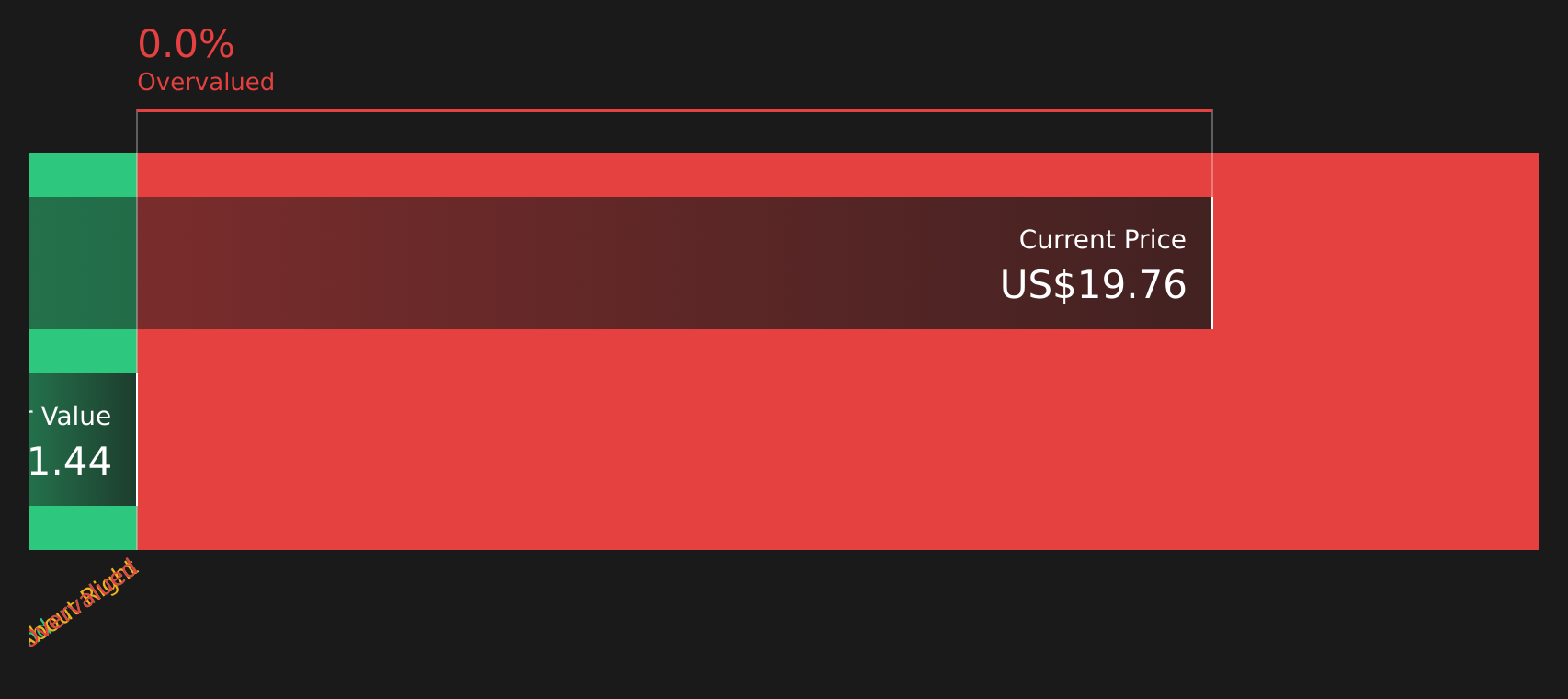

Approach 1: Maase Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes estimates of a company’s future cash flows and discounts them back to today using a required rate of return, to arrive at an implied intrinsic value per share.

For Maase, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections in CN¥. The latest twelve month free cash flow is CN¥10.20 million, and the model projects increasing free cash flows over time, reaching an estimated CN¥296.98 million in 2035, with intermediate annual projections between these points. Estimates beyond the first few years are extrapolated from the available data rather than based on explicit analyst forecasts.

The output of this DCF suggests an intrinsic value of about US$1.51 per share, compared with the current share price of US$9.30. On this basis, the model indicates that Maase is trading at a very large premium to its DCF estimate, with the stock described as more than 5x above the implied value.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Maase may be overvalued by 515.2%. Discover 51 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Maase Price vs Book

For profitable financial and insurance companies, price to book, or P/B, is a useful yardstick because it compares what you are paying in the market to the accounting value of the company’s net assets. Investors generally accept a higher P/B when they expect stronger growth or lower risk, and a lower P/B when growth prospects or risk look less favorable.

Maase is currently trading on a P/B of 14.42x, which is well above both the Insurance industry average of about 1.50x and the peer group average of about 4.41x. This indicates that the market is placing a much higher value on each dollar of Maase’s book value than it does for typical insurers and peers.

Simply Wall St’s Fair Ratio is a proprietary estimate of what Maase’s P/B could be, given factors such as its earnings profile, industry, profit margins, market value and risk characteristics. This tends to be more tailored than a simple comparison to peers or industry averages because it considers company specific growth and risk inputs rather than broad groupings. In Maase’s case, the Fair Ratio is not available, so it is not possible to say whether the current 14.42x looks overvalued, undervalued or about right based on that framework.

Result: ABOUT RIGHT

P/B ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Maase Narrative

Earlier the article mentioned that there is an even better way to understand valuation. Narratives bring this to life by letting you attach a clear story, your view on Maase’s fair value and your assumptions for future revenue, earnings and margins to the numbers.

A Narrative links what you believe about the business, such as how it might grow or how profitable it could be, to a financial forecast and then to an estimated fair value that you can compare with today’s US$9.30 share price.

On Simply Wall St’s Community page, Narratives are available as an easy tool used by millions of investors. They help you see at a glance whether your fair value suggests Maase looks expensive or attractive compared with the current price, and whether that might indicate a time to buy, hold or sell.

Narratives also update automatically when new information such as news, filings or earnings is added to the platform, so your Maase view can stay aligned with the latest data. Different investors can express very different fair values for the stock based on their own assumptions, even when they are looking at the same underlying figures.

Do you think there's more to the story for Maase? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.