Is It Too Late To Consider Marriott International (MAR) After A 44% One Year Run?

Marriott International, Inc. Class A MAR | 0.00 |

- Wondering whether Marriott International at around US$375.60 is still reasonable value after a strong run, or if you might be paying too much for the stock.

- The share price sits at US$375.60 after returns of 1.7% over the past week, 6.1% over the past month, 19.8% year to date and 43.6% over the last year. These moves naturally raise questions about growth potential and changing risk perceptions.

- Recent news coverage has focused on Marriott International's position as a large global hotel operator and ongoing interest in travel and accommodation stocks. This attention has helped keep the company in focus. The broader interest provides a backdrop for the recent share price moves and sets up an important question about whether the current price lines up with underlying value.

- Right now, the company scores 0 out of 6 on our valuation checks, as shown in our valuation summary. The next sections will compare different ways to think about Marriott International's value and finish with an approach that can give you a fuller picture of what the stock might be worth over time.

Marriott International scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

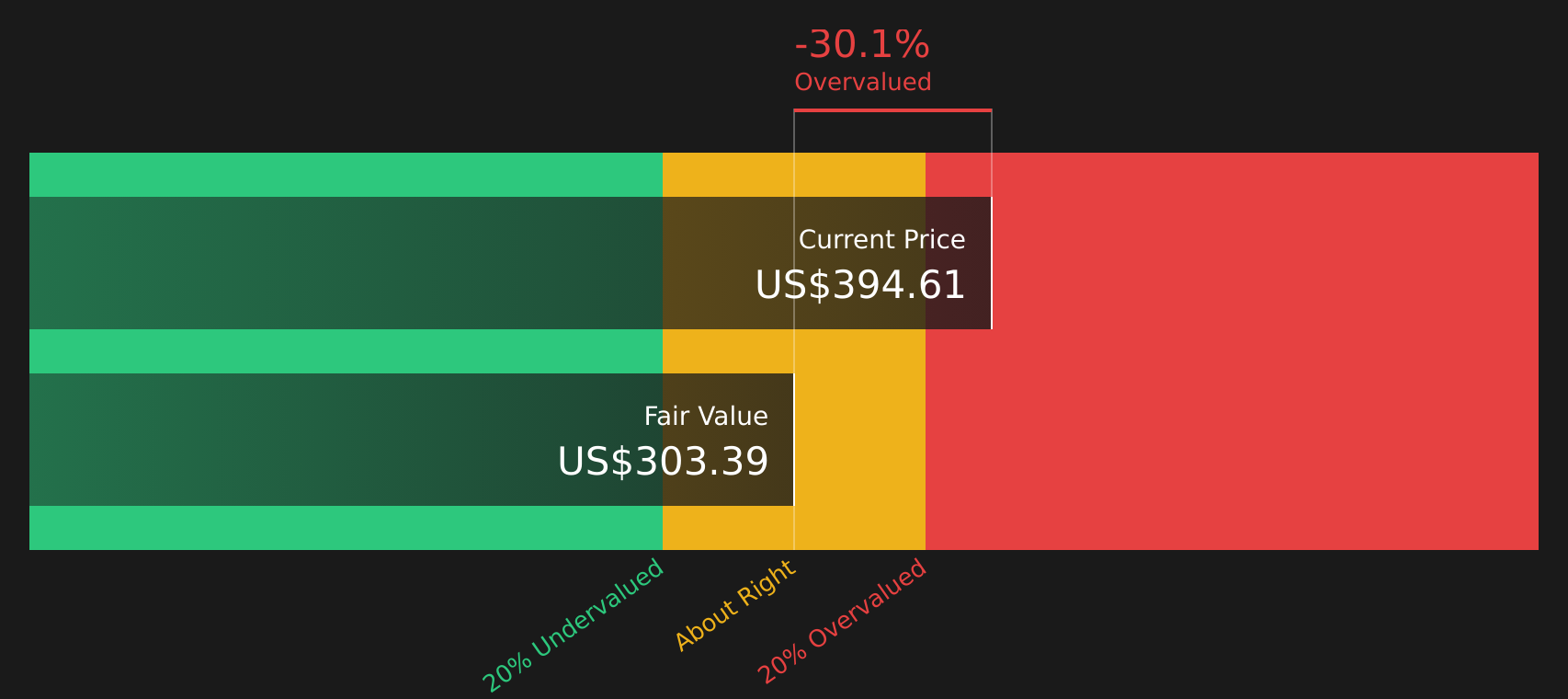

Approach 1: Marriott International Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock might be worth by projecting the company’s future cash flows and discounting them back to today’s value using a required return.

For Marriott International, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections in US$. The latest twelve month free cash flow is around $2.6b. Analyst estimates and subsequent extrapolations point to projected free cash flow of $3.1b in 2026 and $4.8b by 2030, with later years based on Simply Wall St’s own assumptions beyond the explicit analyst horizon.

Aggregating and discounting these projected cash flows results in an estimated intrinsic value of about $310.18 per share. Compared with the current share price of $375.60, the DCF output suggests the stock is around 21.1% above this modelled value. On this measure alone, the shares appear expensive relative to this DCF estimate.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Marriott International may be overvalued by 21.1%. Discover 46 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Marriott International Price vs Earnings

For profitable companies, the P/E ratio is a useful way to think about value because it links what you pay for the stock to the earnings the business is currently generating. Higher growth expectations or lower perceived risk often support a higher P/E, while slower growth or higher risk can justify a lower multiple.

Marriott International currently trades on a P/E of 38.33x. That sits above both the Hospitality industry average P/E of 20.31x and a peer group average of 29.48x, so the stock is priced more expensively than these broad benchmarks. To refine that comparison, Simply Wall St uses a proprietary “Fair Ratio” of 32.23x, which reflects factors such as the company’s earnings growth profile, profit margins, industry, market cap and specific risks.

This Fair Ratio is more tailored than a simple peer or sector comparison because it adjusts for company specific characteristics instead of assuming all Hospitality stocks deserve the same multiple. Comparing the current P/E of 38.33x with the Fair Ratio of 32.23x suggests Marriott International is trading above what this framework would consider a fair level.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Marriott International Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are a simple way for you to attach a story to the numbers by setting your own fair value and assumptions for Marriott International’s future revenue, earnings and margins, then linking that story to a financial forecast and a fair value estimate.

On Simply Wall St’s Community page, Narratives are an accessible tool used by millions of investors that let you compare that fair value with the current price to help you decide whether the stock looks cheap or expensive based on your own view. They update automatically when fresh information like news, earnings or guidance is added to the platform.

For Marriott International, one investor might focus on an asset light model, high margins and loyalty economics and arrive at a higher fair value such as US$569.07. Another might place more weight on cyclicality, risk factors or different assumptions and come to a lower figure such as US$313.53. Narratives simply make those different viewpoints visible, comparable and easier for you to use in your own decision making.

For Marriott International however, here are previews of two leading Marriott International Narratives:

Fair value: US$569.07 per share

Implied discount to this fair value: around 34.0% compared with the last close of US$375.60

Revenue growth assumption: 19.23%

- Highlights the asset light model, with management and franchise contracts supporting fee based revenue and margins across a global hotel portfolio.

- Emphasizes the breadth of brands and the Marriott Bonvoy loyalty program as drivers of repeat stays and pricing power for a wide range of travelers.

- Frames Marriott as a long term beneficiary of global mobility and experience led travel, with scale and brand trust as key differentiators.

Fair value: US$313.94 per share

Implied premium to this fair value: around 19.6% compared with the last close of US$375.60

Revenue growth assumption: 2.36%

- Focuses on Marriott as a high margin, fee based platform that relies heavily on franchise and management contracts rather than owning hotel real estate.

- Points to risks such as economic slowdowns, potential brand dilution from under invested properties, competitive pressure from online travel platforms and loyalty program devaluation concerns.

- Uses forward revenue and P/E assumptions to suggest a fair value range that sits below the current share price, which may limit upside based on this framework.

These two Narratives sit alongside others on Simply Wall St. They provide a way to compare different fair values, growth assumptions and risk views before deciding how Marriott International fits into an individual portfolio and return expectations.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Marriott International on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Marriott International? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.