Is It Too Late To Consider Marriott International (MAR) After Its Strong Multi Year Rally

Marriott International, Inc. Class A MAR | 0.00 |

- Wondering whether Marriott International's share price still offers value after such a strong run, or if you might be arriving late? This article walks through what the current price could mean for you.

- Marriott International last closed at US$377.93, with returns of 6.7% over 7 days, 17.2% over 30 days, 20.6% year to date, 73.1% over 1 year, 123.2% over 3 years and 164.7% over 5 years.

- Recent coverage around Marriott International has focused on its position within global travel and hospitality, as well as ongoing interest in large hotel operators as the sector continues to attract attention. This backdrop helps explain why investors are closely watching the stock after such strong multi year returns.

- Despite this performance, Marriott International currently scores 0 out of 6 on Simply Wall St's valuation checks. The sections that follow will walk you through what standard valuation methods suggest about the stock, then finish with a broader way to think about valuation that can put those numbers into context.

Marriott International scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

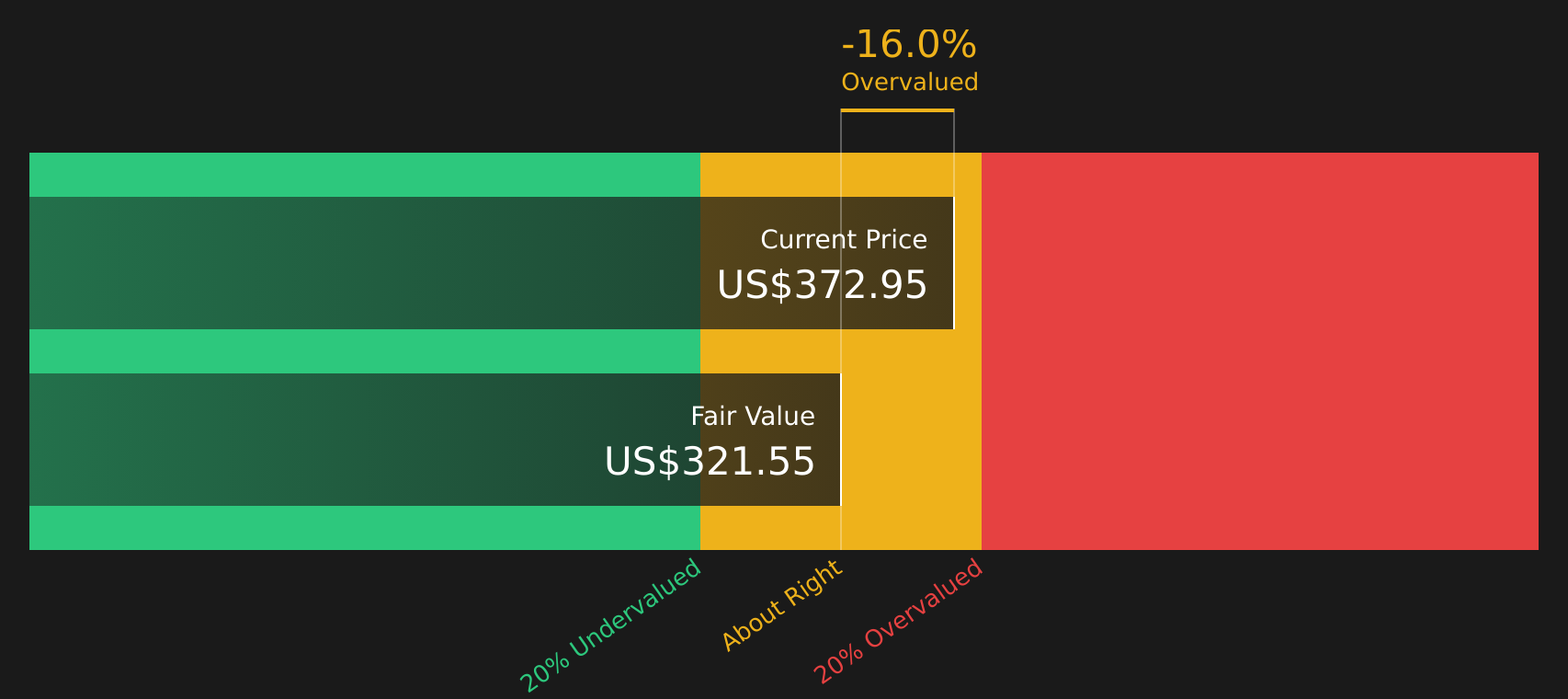

Approach 1: Marriott International Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business could be worth by projecting its future cash flows and then discounting those back to today using a required return. It is essentially asking what all those future dollars are worth in present terms.

For Marriott International, the model uses a 2 Stage Free Cash Flow to Equity approach built on cash flow projections. The latest twelve month free cash flow is about US$2.41b. Analysts supply forecasts for the coming years, and Simply Wall St then extends those projections, with free cash flow estimates reaching about US$6.33b in 2035 based on the provided path.

When these projected cash flows are discounted back, the DCF model arrives at an estimated intrinsic value of US$305.84 per share. Against the recent share price of US$377.93, this implies the stock is about 23.6% above the DCF estimate, which points to a rich valuation on this model alone.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Marriott International may be overvalued by 23.6%. Discover 59 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Marriott International Price vs Earnings

For profitable companies, the P/E ratio is a useful yardstick because it links what you pay per share to the earnings that support that share price. In general, higher growth expectations or lower perceived risk can justify a higher P/E, while slower growth or higher risk often point to a lower, more conservative P/E being reasonable.

Marriott International currently trades on a P/E of 38.50x. This sits above both the Hospitality industry average P/E of 22.02x and the peer group average of 33.39x, so the stock is priced at a premium compared with many similar businesses. Simply Wall St also provides a proprietary “Fair Ratio” of 29.97x, which reflects the P/E level suggested by factors such as the company’s earnings growth profile, industry, profit margin, market cap and identified risks.

The Fair Ratio can be more informative than a simple comparison with peers or the broad industry because it adjusts for Marriott International’s specific characteristics, rather than assuming all companies in the sector deserve the same multiple. Comparing the Fair Ratio of 29.97x with the actual P/E of 38.50x suggests the shares are trading above this modelled range.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Marriott International Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives step in as your way of turning a view about Marriott International into a clear story that connects assumptions about future revenue, earnings and margins with a fair value that you can compare to the current share price.

On Simply Wall St, Narratives sit inside the Community page and let you anchor that story to hard numbers. For example, one investor might build a more cautious Marriott view around a fair value close to the DCF estimate of about US$305.84 per share. Another might align with a higher fair value closer to the more optimistic Community and analyst work that clusters around the US$356.92 to US$370.00 range.

Each Narrative links those assumptions to a fair value so you can quickly see whether your story says Marriott looks expensive or inexpensive versus today’s US$377.93 price. Because Narratives are updated as new earnings, news or forecasts are added, your framework stays current without you needing to rebuild it from scratch.

For Marriott International however, we will make it really easy for you with previews of two leading Marriott International Narratives:

These sit on opposite sides of the debate, which is exactly what you want when you are weighing up a stretched P/E and an above market share price against the quality of the underlying business model.

Fair value in this narrative: US$569.07 per share

Implied discount to this fair value: about 33.6% relative to the recent US$377.93 price

Revenue growth assumption used: 19.23%

- Sees Marriott as a resilient global travel platform built around an asset light management and franchise model with fee based revenue.

- Highlights the breadth of brands and the Marriott Bonvoy ecosystem as key supports for customer loyalty and pricing power across regions.

- Frames expansion in emerging markets and continued focus on experiences, extended stays and partnerships as important drivers alongside disciplined capital allocation.

Fair value in this narrative: US$313.94 per share

Implied premium to this fair value: about 20.3% relative to the recent US$377.93 price

Revenue growth assumption used: 2.36%

- Focuses on Marriott as a high margin, fee driven, asset light platform that keeps real estate risk with hotel owners while benefiting from franchise and management contracts and loyalty point sales.

- Points to strong returns on invested capital and high EBITDA margins, supported by scale, direct booking strength and the Bonvoy program, but with meaningful exposure to the hotel cycle.

- Flags risks around macro slowdowns, potential brand dilution, technology competition and loyalty point devaluation, and applies more conservative growth and P/E assumptions to arrive at lower fair values than the current share price.

Do you think there's more to the story for Marriott International? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.