Is It Too Late To Consider Norfolk Southern (NSC) After Strong Multi Year Share Gains?

Norfolk Southern Corporation NSC | 0.00 |

- For investors considering whether Norfolk Southern at around US$309.93 is still offering value or if the easy money has already been made, this article walks through what the price may be reflecting.

- The stock has returned 1.6% over the past week and 7.7% year to date, with a 26.0% return over the last year and 53.2% across three years, giving plenty for current and prospective shareholders to think about.

- Recent attention has centered on Norfolk Southern's role within the broader US transportation sector and how rail operators fit into long term infrastructure and freight trends. At the same time, investors have been weighing sector sentiment and company specific headlines against the stock's 30 day return, which is down 0.7%.

- Norfolk Southern currently scores a 2 out of 6 on our valuation checks. The next sections will break down what traditional methods like P/E, P/B and cash flow based models suggest about the current price, and then conclude with a deeper way to think about what valuation may mean for long term holders.

Norfolk Southern scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Norfolk Southern Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model projects the cash Norfolk Southern could generate in the future and then discounts those projections back to today to estimate what the stock might be worth now.

Norfolk Southern’s latest twelve month free cash flow is about $893.3 million. Analysts and internal estimates project free cash flow rising to $2.96 billion by 2030, using a 2 Stage Free Cash Flow to Equity model that blends analyst forecasts for the nearer years with extrapolated figures for the later period.

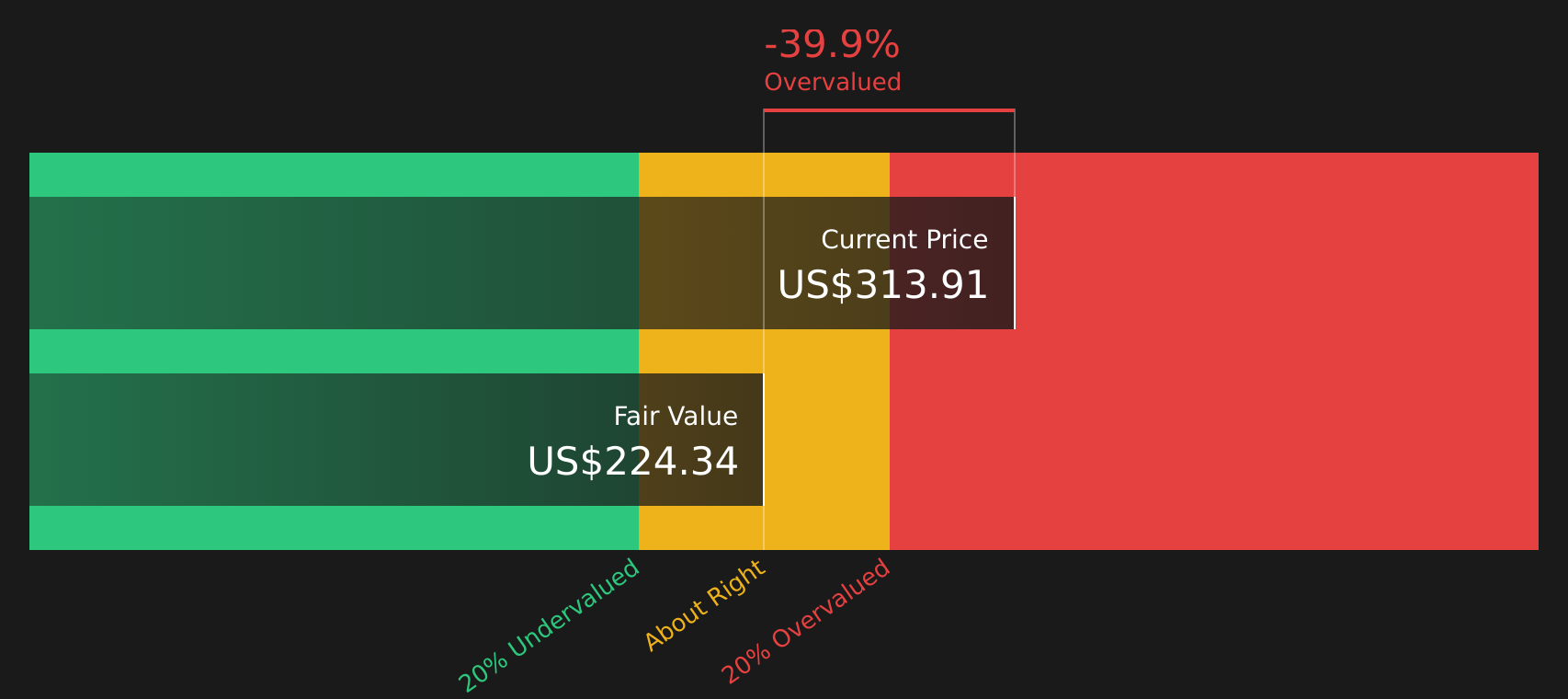

When all projected cash flows from 2026 through 2035 are discounted back to today, the DCF model indicates an intrinsic value of about $224.60 per share. Compared with the recent share price of about $309.93, this model suggests the stock is around 38.0% above that estimate of fair value. In other words, the DCF view points to Norfolk Southern trading at a premium.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Norfolk Southern may be overvalued by 38.0%. Discover 47 high quality undervalued stocks or create your own screener to find better value opportunities.

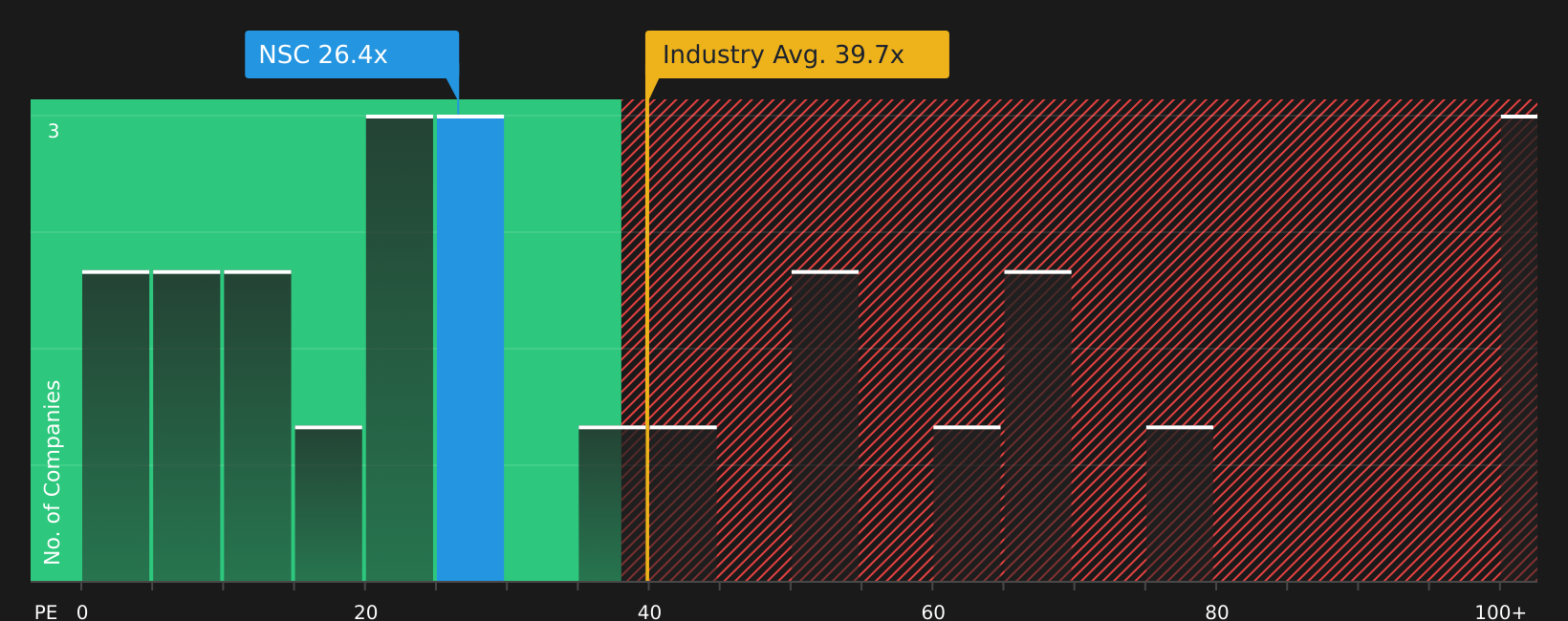

Approach 2: Norfolk Southern Price vs Earnings

For a profitable company like Norfolk Southern, the P/E ratio is a straightforward way to check what you are paying for each dollar of earnings. Investors generally accept that stronger growth potential or lower perceived risk can support a higher P/E, while slower growth or higher risk usually call for a lower, more conservative multiple.

Norfolk Southern currently trades on a P/E of about 26.10x. That sits below the broader Transportation industry average of about 39.57x and also below the peer group average of around 29.85x. To go a step further, Simply Wall St estimates a proprietary “Fair Ratio” of 24.87x for Norfolk Southern, which reflects factors such as its earnings growth profile, industry, profit margin, market capitalization and company specific risks.

This Fair Ratio is more tailored than a simple comparison with peers or the overall industry because it attempts to align the multiple with Norfolk Southern’s own fundamentals rather than broad group averages. Set against the current P/E of 26.10x, the Fair Ratio of 24.87x suggests the stock is priced somewhat above that customized benchmark.

Result: OVERVALUED

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Upgrade Your Decision Making: Choose your Norfolk Southern Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Think of a Narrative as your own clear story for Norfolk Southern that links what you believe about its business, its future revenue, earnings and margins to a fair value estimate on Simply Wall St's Community page. It then compares that fair value with the current price to help you decide if the stock looks attractive or stretched, keeps that view automatically refreshed when news or earnings land, and lets you see how different investors frame the same company. For example, one Narrative might lean toward the higher US$378.00 analyst target because it expects PSR 2.0 efficiencies and industrial development to support long term earnings, while another might anchor closer to the lower US$297.00 target because it focuses more on risks like storm restoration costs, coal pricing, trade policy and pricing pressure in intermodal.

Do you think there's more to the story for Norfolk Southern? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.