Is It Too Late To Consider Philip Morris International (PM) After Its Recent Share Price Rebound?

Philip Morris International Inc. PM | 0.00 |

- Wondering if Philip Morris International at around US$180.77 a share offers good value, or if the recent price action has already done the heavy lifting for you?

- The stock is up 3.3% over the past week, while it is down 3.3% over the past month, with returns of 12.8% year to date and 1.7% over the last year, giving mixed signals about momentum and risk sentiment.

- Recent coverage of Philip Morris International has focused on how investors view its long term positioning and the role of the stock in income focused portfolios. This context helps explain why shorter term price moves can attract attention even when the longer term return profile looks different.

- Right now the company has a valuation score of 0 out of 6, so the rest of this article looks at what different valuation approaches say about the stock and concludes with a way to think about value that goes beyond any single model.

Philip Morris International scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

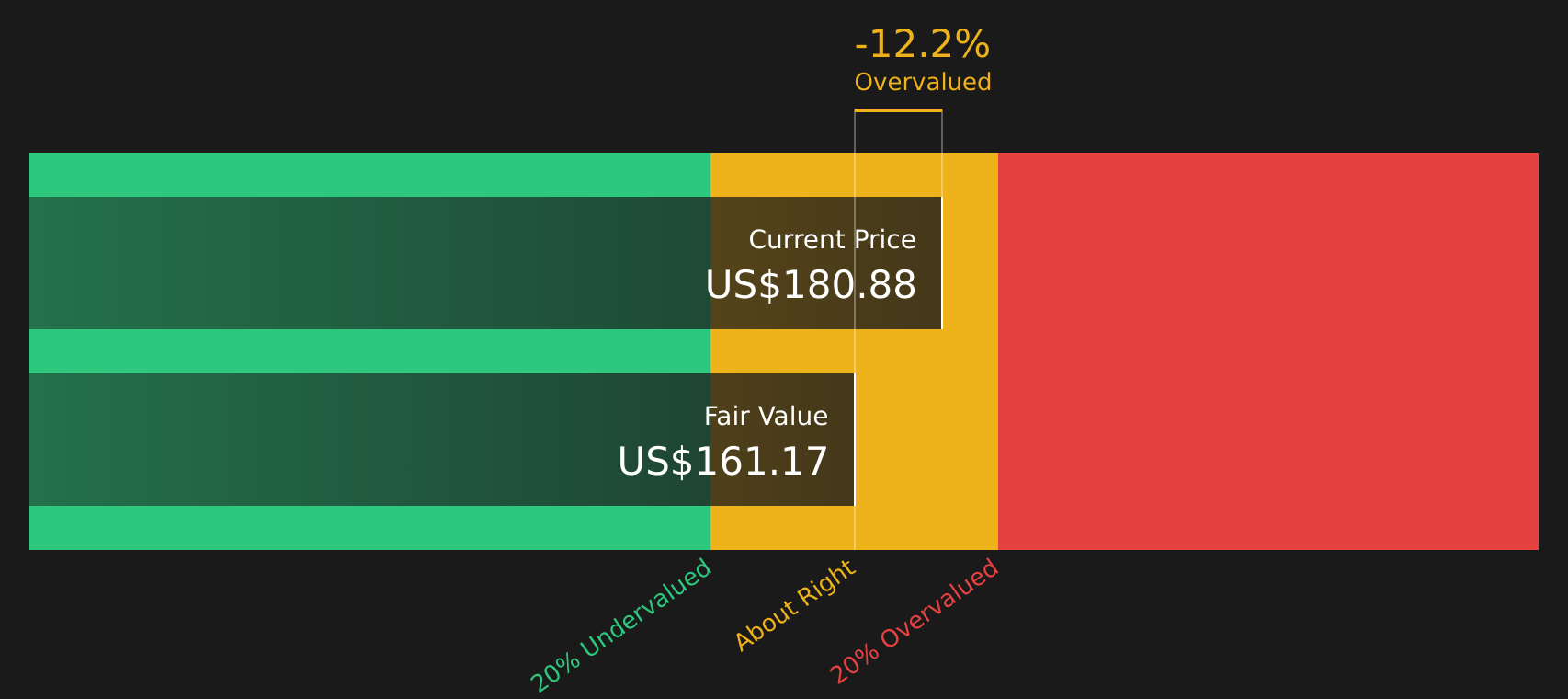

Approach 1: Philip Morris International Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting the company’s future cash flows and discounting them back to today using a required rate of return. It is essentially asking what today’s fair price might be for those future dollars of cash.

For Philip Morris International, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is about $10.60b. Simply Wall St then uses analyst estimates to 2025 and extrapolates further, with projected free cash flow for 2035 of about $15.14b. Each of these future cash flows is discounted back to today in dollar terms to reflect time and risk.

Putting those projections together gives an estimated intrinsic value of $162.75 per share, compared with the recent share price of about $180.77. On this view, the stock screens as around 11.1% overvalued, so the DCF suggests the recent price already builds in a fair amount of optimism.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Philip Morris International may be overvalued by 11.1%. Discover 47 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Philip Morris International Price vs Earnings

For a profitable company, the P/E ratio is a handy shorthand for how much you are paying for each dollar of earnings. It links directly to what the business is currently generating, which many investors find easier to relate to than long dated cash flow forecasts.

What counts as a “normal” or “fair” P/E depends on what the market expects for growth and how much risk investors see in those earnings. Higher expected growth or lower perceived risk can justify a higher P/E, while slower growth or higher risk usually points to a lower multiple.

Philip Morris International currently trades on a P/E of 25.46x. That sits well above the Tobacco industry average of 12.07x and also above the peer group average of 22.88x, so on simple comparisons the stock looks expensive. Simply Wall St’s Fair Ratio for Philip Morris International is 25.24x, which is an estimate of the P/E that might fit the company based on factors like its earnings growth profile, profit margins, industry, market cap and risk characteristics.

Because the Fair Ratio is tailored to the company, it can give a more nuanced view than broad peer or industry averages alone.

With the current P/E at 25.46x versus a Fair Ratio of 25.24x, the stock screens as about in line with this metric.

Result: ABOUT RIGHT

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Upgrade Your Decision Making: Choose your Philip Morris International Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Meet Narratives, a simple way for you to connect your view of Philip Morris International’s future to hard numbers by telling a short story about its revenue, earnings, margins and fair value, then comparing that fair value to today’s price to decide whether the stock looks attractive or not.

On Simply Wall St’s Community page, Narratives are available as an easy tool used by millions of investors. Each Narrative links a company story to a forecast and a fair value that automatically updates when new information such as news, regulatory developments or earnings is added.

For Philip Morris International, one investor might align with the bullish Narrative that assumes a fair value of US$210.00 per share based on higher expected revenue growth, margins and a P/E of 26.1x. Another might prefer the more cautious Narrative that assumes a fair value of US$153.00 per share with different revenue and margin expectations, and seeing these side by side helps you decide which story, and which fair value, fits your own view best.

For Philip Morris International, we will make it really easy for you with previews of two leading Philip Morris International Narratives:

Each one connects a different story about regulation, earnings and smoke free products to a specific fair value, so you can quickly see which version of the future lines up more closely with your own expectations for the stock.

Fair value in this bullish Narrative: US$193.14 per share.

On this view, the stock looks about 6.4% below that fair value based on the recent price of US$180.77.

Revenue growth assumption: 6.12% a year.

- Assumes smoke free products such as IQOS, ZYN and VEEV keep gaining traction globally, supporting higher net revenue and margin outcomes over time.

- Builds in benefits from geographic diversification, digital and direct to consumer channels and higher long term profit margins.

- Takes analyst forecasts and discounts projected earnings and a future P/E of 24.8x back to today to reach a consensus fair value close to US$193 per share.

Fair value in this cautious Narrative: US$170.00 per share.

On this view, the stock screens about 6.3% above that fair value based on the recent price of US$180.77.

Revenue growth assumption: 5.72% a year.

- Emphasises public health pressures, tax and regulatory hurdles and ESG driven capital constraints that could limit how much value investors are willing to place on future earnings.

- Assumes ongoing cigarette volume declines and execution risk in next generation products, even with growth from areas like ZYN nicotine pouches.

- Uses a lower future P/E multiple of 23.85x and a slightly higher discount rate to bring projected revenues and earnings back to a fair value around US$170 per share.

If you want to go deeper than these two previews and see the full range of Narratives that other investors are using to think about Philip Morris International, including how they weigh risks against potential rewards, you can review the wider set of community views via See what the community is saying about Philip Morris International.

Do you think there's more to the story for Philip Morris International? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.