Is It Too Late To Consider RenaissanceRe Holdings (RNR) After Strong Multi‑Year Share Price Gains?

RenaissanceRe Holdings Ltd. RNR | 305.85 | +0.93% |

- If you are wondering whether RenaissanceRe Holdings at around US$307 per share still offers value, or if most of the upside is already reflected in the price, this article breaks that question down for you.

- The stock has recent returns of 3.9% over 7 days, 3.5% over 30 days, 12.8% year to date, 29.3% over 1 year, 51.3% over 3 years and 86.3% over 5 years. These figures naturally raise questions about what is already priced in.

- Recent news coverage has focused on RenaissanceRe Holdings as a major player in reinsurance and insurance linked risk, with attention on how it manages exposure to large loss events and capital allocation decisions. These themes help frame how investors are currently thinking about both risk and potential reward around the stock.

- On Simply Wall St's valuation checks, RenaissanceRe Holdings records a valuation score of 5 out of 6. The sections that follow will compare several valuation approaches before finishing with a more holistic way to think about what that score really means for you.

Approach 1: RenaissanceRe Holdings Excess Returns Analysis

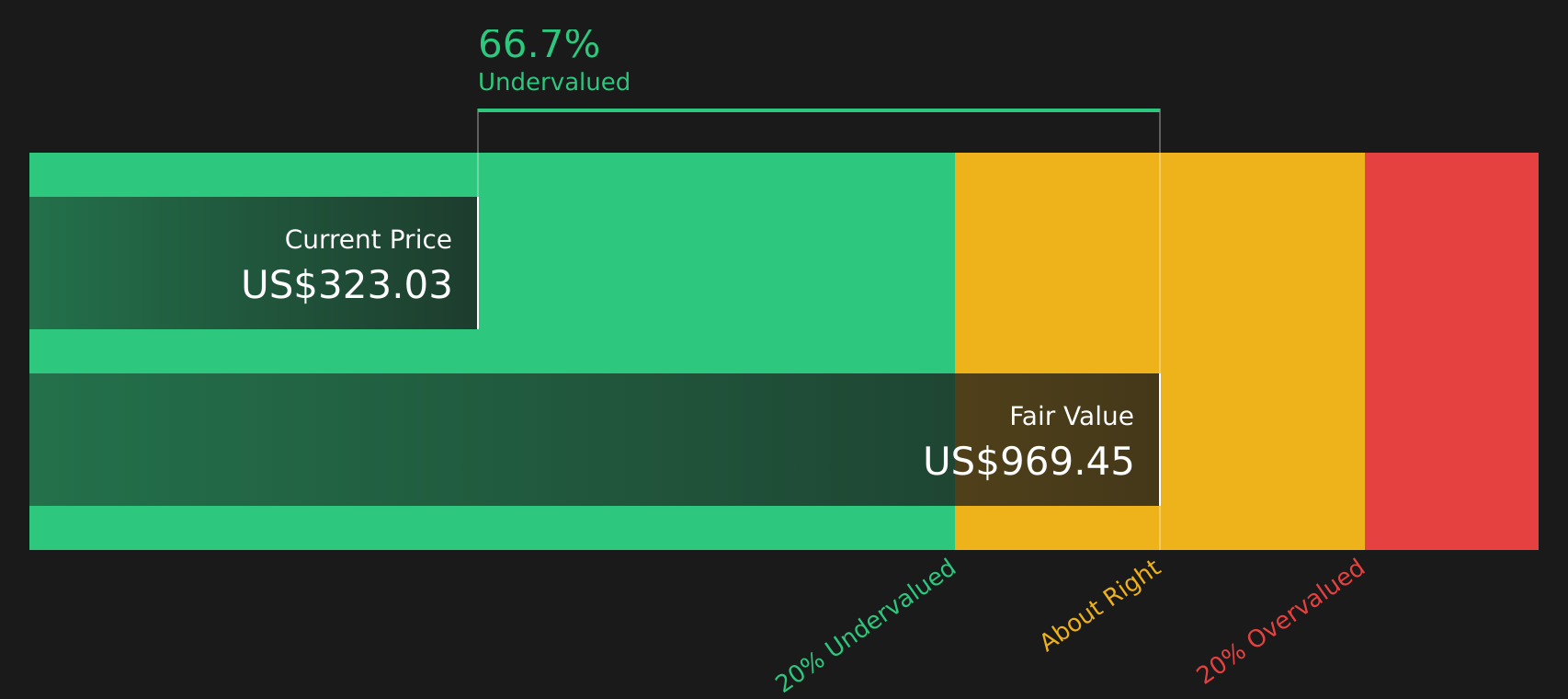

The Excess Returns model looks at how much value a company may create over and above the return that shareholders typically require on their equity. Instead of focusing on cash flows, it compares the earnings power of the business with the cost of that equity capital.

For RenaissanceRe Holdings, the model starts with a Book Value of $247.00 per share and a Stable EPS estimate of $44.89 per share, based on weighted future Return on Equity estimates from 9 analysts. The Average Return on Equity used is 14.74%, while the Cost of Equity is $21.26 per share. That produces an Excess Return of $23.64 per share. This is then capitalized over time on a Stable Book Value base of $304.60 per share, sourced from weighted future Book Value estimates from 8 analysts.

Putting this together, the Excess Returns model arrives at an intrinsic value of about $967.11 per share. Compared with the recent share price of roughly $307, this implies RenaissanceRe Holdings is 68.2% undervalued according to this method.

Result: UNDERVALUED

Our Excess Returns analysis suggests RenaissanceRe Holdings is undervalued by 68.2%. Track this in your watchlist or portfolio, or discover 64 more high quality undervalued stocks.

Approach 2: RenaissanceRe Holdings Price vs Earnings

For a profitable business like RenaissanceRe Holdings, the P/E ratio is a useful quick check on how much you are paying for each dollar of earnings. It helps you see how the market is weighing current performance against expectations and perceived risk.

In simple terms, higher growth expectations and lower perceived risk usually support a higher "normal" P/E, while lower growth expectations or higher risk tend to justify a lower multiple. RenaissanceRe Holdings currently trades on a P/E of 5.09x. This sits below the Insurance industry average P/E of 11.47x and below the peer group average of 8.69x.

Simply Wall St's Fair Ratio for RenaissanceRe Holdings is 8.49x. This Fair Ratio is a proprietary estimate of what the P/E might be given the company’s earnings profile, industry, profit margins, market value and risk factors. It is more tailored than a simple comparison with peers or the broad industry, because it adjusts for company specific characteristics rather than assuming all insurers deserve the same multiple.

Comparing the Fair Ratio of 8.49x with the current P/E of 5.09x indicates that the shares are trading below that tailored benchmark on this measure.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your RenaissanceRe Holdings Narrative

Earlier the article mentioned that there is an even better way to understand valuation, and that is where Narratives come in, giving you a clear story behind your numbers by linking your view on RenaissanceRe Holdings to a simple financial forecast and a Fair Value estimate that can then be compared with the current share price.

A Narrative on Simply Wall St is your own explanation of what you think will happen to a company’s revenue, earnings and margins, and it connects that story directly to a Fair Value so you can quickly see whether your view suggests the stock is cheap or expensive at today’s price.

Narratives live inside Simply Wall St’s Community page, are designed to be easy to use, and are used by millions of investors to turn their opinions into structured forecasts that update automatically when new information such as earnings, news or guidance is incorporated into the platform’s data.

With RenaissanceRe Holdings, one investor might align with a more cautious Narrative that anchors on a Fair Value around US$282 per share. Another might prefer a more optimistic Narrative closer to US$407. By comparing each Fair Value to the current market price, each investor can decide whether that story supports buying, holding or waiting based on their own assumptions rather than a single consensus view.

For RenaissanceRe Holdings however we will make it really easy for you with previews of two leading RenaissanceRe Holdings Narratives:

Fair Value: US$406.84 per share

Implied discount to this Fair Value based on the last close of US$307.08: 24.5%

Revenue growth assumption: 9.73% annual decline

- Emphasises underwriting discipline supported by proprietary modeling and advanced analytics that aim to secure terms and margins above market levels.

- Highlights capital management and share buybacks as important to earnings per share, especially if the share price trades below the analyst view of intrinsic value.

- Sees fee based insurance linked securities activity and a scalable underwriting platform as building blocks for resilient earnings, while still flagging climate, competition and regulatory risks.

Fair Value: US$282.00 per share

Implied premium to this Fair Value based on the last close of US$307.08: 8.9%

Revenue growth assumption: 10.67% annual decline

- Focuses on heavier exposure to natural catastrophe and property risks, which could pressure capital and earnings if large loss events become more frequent or costly.

- Points to competition from alternative capital, integration costs and possible changes in regulation and technology as headwinds for pricing power, margins and revenue.

- Still recognises diversified underwriting, fee income and capital management as supports for profitability, but concludes that these are already close to reflected in the Fair Value.

Do you think there's more to the story for RenaissanceRe Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.