Is It Too Late To Consider Ultra Clean Holdings (UCTT) After 182% Year To Date Surge?

Ultra Clean Holdings, Inc. UCTT | 0.00 |

- If you are wondering whether Ultra Clean Holdings at US$76.98 still offers value or is starting to look stretched, the stock’s recent performance makes that question especially timely.

- The share price has delivered a 181.8% return year to date and 258.0% over the last year, even though it has fallen 7.2% over the past week and 3.2% over the past month.

- Recent coverage has focused on Ultra Clean Holdings as a semiconductor equipment supplier exposed to ongoing demand for chip manufacturing capacity, which helps explain why the stock has been on many investors’ radar. At the same time, headlines have highlighted sector wide volatility, which provides some context for the shorter term pullback in the share price.

- Ultra Clean Holdings currently holds a valuation score of 4/6. The rest of this article will walk through how different valuation methods line up on the stock, and will conclude with a way to think about its value in more depth.

Approach 1: Ultra Clean Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes estimates of a company’s future cash flows and discounts them back to what they could be worth today. It is a way of asking what you might be paying now for the cash the business could generate in the future.

For Ultra Clean Holdings, the model used is a 2 Stage Free Cash Flow to Equity approach, based on projected free cash flows in $. The latest twelve months free cash flow is a loss of $55.42 million. Analysts provide free cash flow estimates out to 2030, with projected free cash flow of $306.70 million in that year. Beyond the explicit analyst window, Simply Wall St extrapolates additional cash flow projections through 2035 using its own growth assumptions.

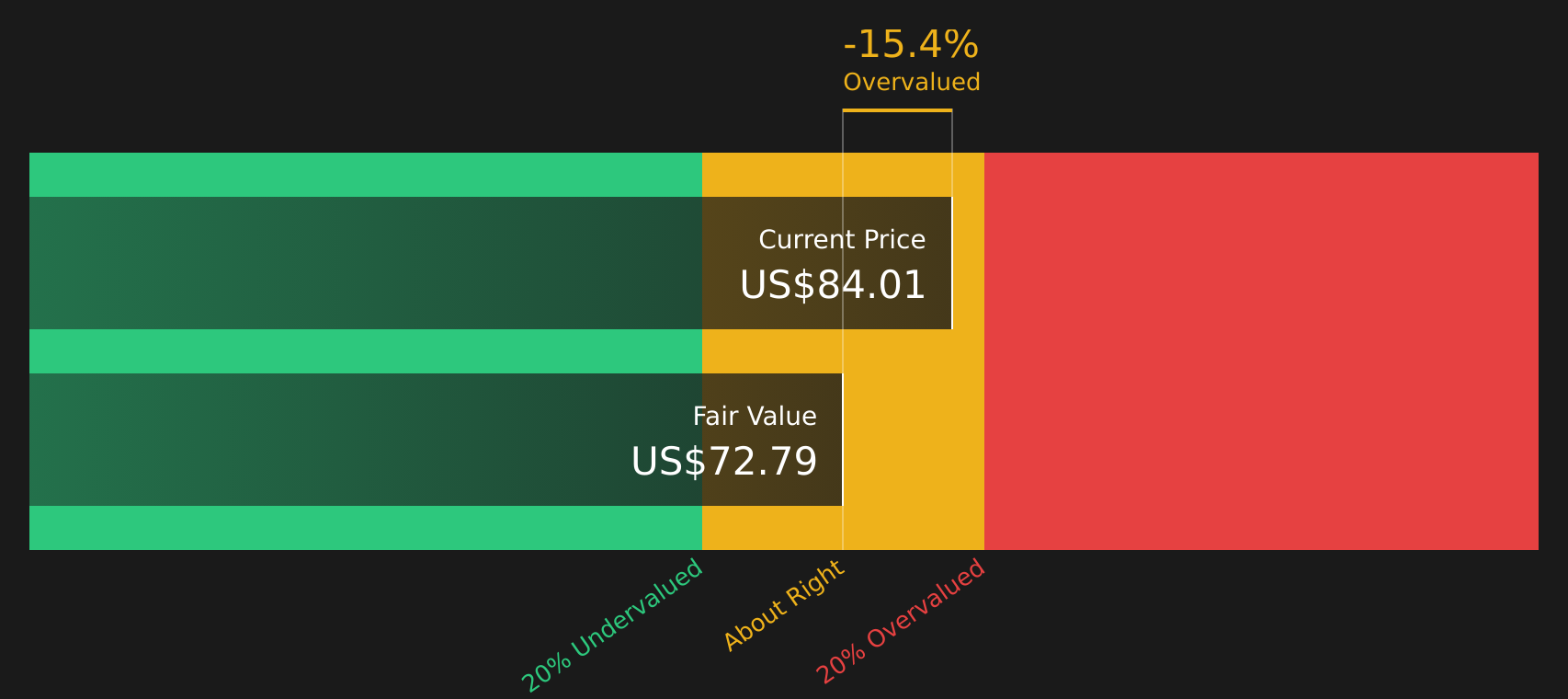

When these projected cash flows are discounted back and summed, the DCF model indicates an estimated fair value of $72.88 per share. At a market price of $76.98, this implies Ultra Clean Holdings is trading at about a 5.6% premium to the model’s estimate, which is a relatively small gap.

Result: ABOUT RIGHT

Ultra Clean Holdings is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Ultra Clean Holdings Price vs Sales

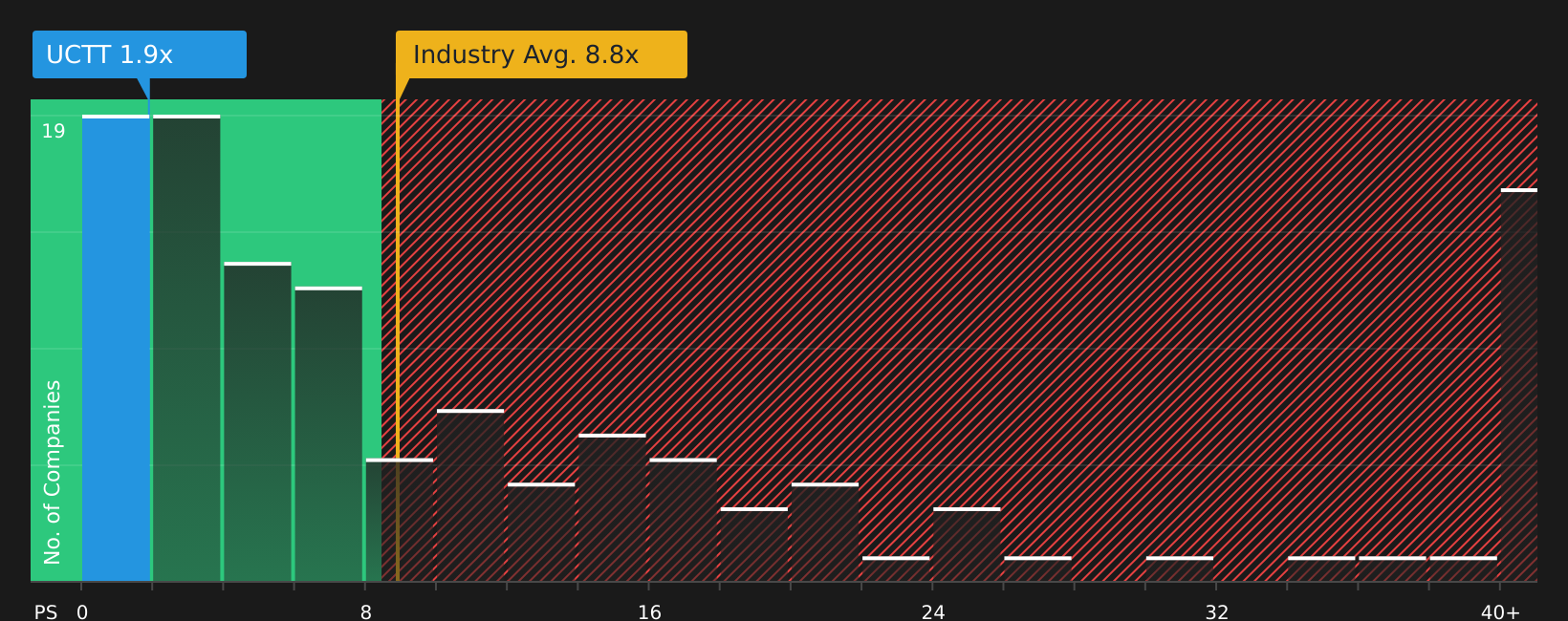

For companies where earnings can be uneven, the P/S ratio is often a useful cross check because it compares the stock price with the revenue the business generates, rather than profits that can be affected by one off items.

In general, higher expected growth and lower perceived risk can justify a higher P/S multiple, while slower growth or higher risk usually points to a lower “normal” range. That is why simply lining up one company’s P/S ratio against another’s only tells part of the story.

Ultra Clean Holdings currently trades on a P/S ratio of 1.67x. This sits below the Semiconductor industry average P/S of 8.30x and below the peer group average of 3.94x. Simply Wall St’s Fair Ratio for Ultra Clean Holdings is 2.79x, which is its proprietary view of what a sensible P/S might be given factors such as earnings growth, industry, profit margin, market cap and risk profile.

Because the Fair Ratio adjusts for those fundamentals, it can be more informative than a simple industry or peer comparison. With the Fair Ratio of 2.79x above the current 1.67x, Ultra Clean Holdings screens as undervalued on this metric.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Ultra Clean Holdings Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives bring this to life by letting you set a clear story for Ultra Clean Holdings, link that story to your own forecasts for revenue, earnings and margins, translate those into a Fair Value, then continually compare that Fair Value with the live share price as new data like earnings or news arrives. This helps you see, for example, how one investor on the Simply Wall St Community page might build an optimistic Ultra Clean Holdings Narrative around a Fair Value near US$100.00, while another anchors a more cautious Narrative closer to US$70.00. This gives you an accessible tool to decide which story fits your view.

For Ultra Clean Holdings, we will make it really easy for you with previews of two leading Ultra Clean Holdings narratives:

First is a more optimistic take that sees the current price as broadly lining up with long term analyst expectations, with some room for upside if things go right.

Fair value anchor: US$81.25

Gap vs current price: about 5.2% below this fair value estimate

Analyst revenue growth assumption: 12.54% a year

- Focuses on AI related memory and advanced fab investment feeding into higher revenue over time, supported by Ultra Clean Holdings' exposure to complex chip manufacturing equipment.

- Highlights cost reduction, vertical integration and the UCT 3.0 plan as levers that could lift margins if execution stays on track.

- Flags customer concentration, tariff related friction and past goodwill impairment as real risks that could limit how much of the upside story actually shows up in earnings.

The other side is a more cautious view that treats the current share price as rich compared with a lower fair value anchor from the bearish end of analyst expectations.

Fair value anchor: US$35.00

Gap vs current price: about 120% above this fair value estimate

Bear case revenue growth assumption: 11.50% a year

- Points to long qualification cycles, inventory overhang and complex factory changes as factors that could keep margins and revenue from matching higher industry spending.

- Notes that deeper integration with a concentrated set of large customers and a cluster manufacturing model could backfire if key programs are delayed or regional demand is misaligned.

- Accepts that AI, automation and vertical integration could help profitability, but treats these as offsets that may not fully balance the risks of higher costs and execution challenges.

Taken together, these two narratives outline a clear range for what different analysts think Ultra Clean Holdings could be worth. It is then up to you to decide which story feels closer to your own view of the company, its risks and its long term earnings power.

To see how these narratives connect with detailed fair values, risks and forecasts, and to track Ultra Clean Holdings over time in a way that matches your own assumptions, To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Ultra Clean Holdings on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Ultra Clean Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.