Is It Too Late To Reassess Coterra Energy (CTRA) After Its 31% One-Year Rally?

Coterra Energy CTRA | 0.00 |

- If you are wondering whether Coterra Energy at around US$31.85 still offers value or is starting to look fully priced, the recent share performance gives you a useful starting point.

- The stock is up 0.6% over the last week, has a 6.2% decline over 30 days, yet sits on gains of 19.7% year to date and 31.3% over the past year. This can change how the market is currently assessing both its potential and its risks.

- These moves sit against a backdrop of ongoing interest in US oil and gas producers, as investors weigh how established energy names might fit into portfolios focused on cash generation and capital returns. Sector headlines around commodity prices, supply expectations, and capital allocation policies continue to influence how investors think about companies like Coterra Energy.

- Coterra Energy currently holds a valuation score of 4 out of 6. The next sections will break down what that means across different valuation methods, before finishing with a broader way to think about what the current price really implies for the business.

Approach 1: Coterra Energy Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business could be worth by projecting its future cash flows and then discounting those back to today using a required rate of return.

For Coterra Energy, the model used is a 2 Stage Free Cash Flow to Equity approach, based on current last twelve months free cash flow of about $1.58b. Analyst and extrapolated estimates point to free cash flow of $3.03b by 2030, with annual projections between 2026 and 2035 ranging roughly from $2.60b to $3.39b before discounting. Simply Wall St only uses direct analyst inputs for up to five years, then extends the series using its own growth assumptions.

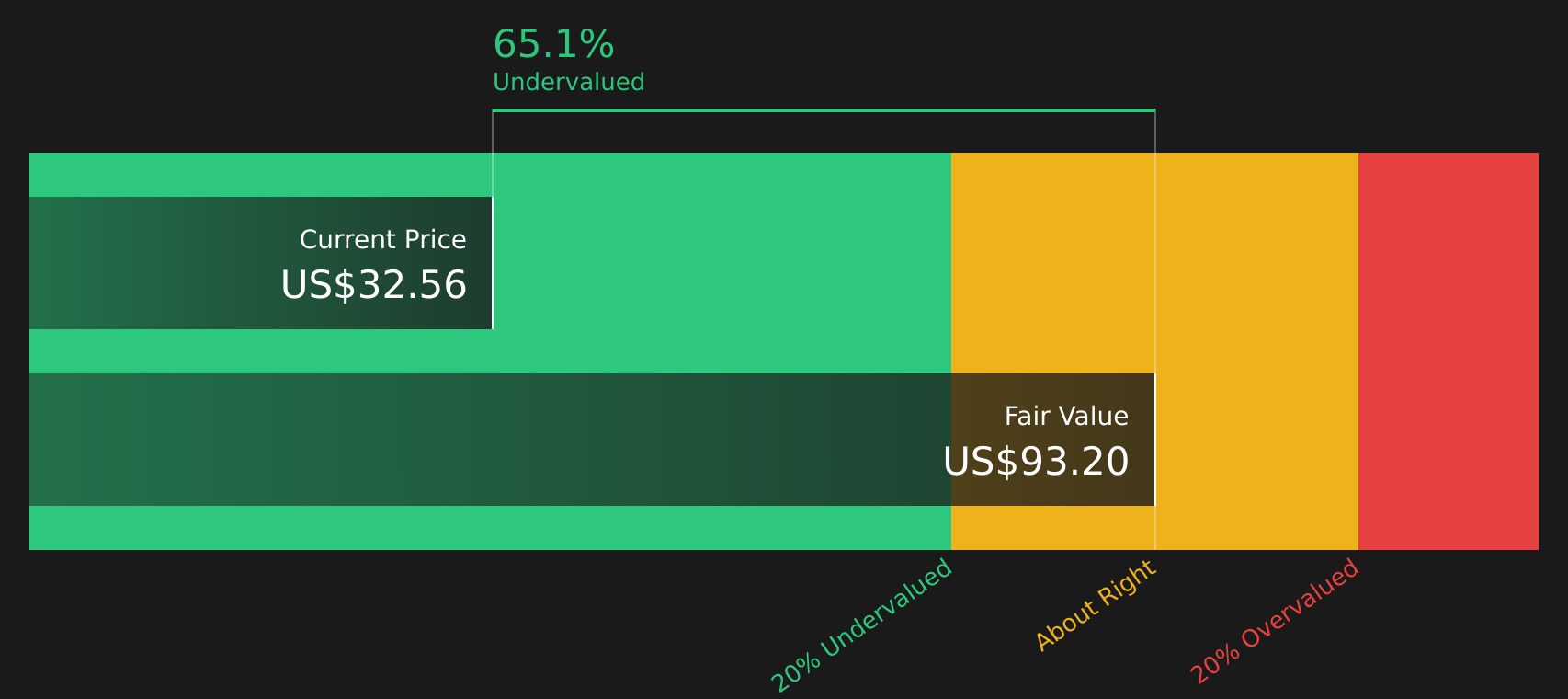

When all those projected cash flows are discounted back to today, the model arrives at an estimated intrinsic value of about $93.85 per share. Compared with a current share price around $31.85, this output suggests the stock is 66.1% undervalued according to this DCF framework.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Coterra Energy is undervalued by 66.1%. Track this in your watchlist or portfolio, or discover 58 more high quality undervalued stocks.

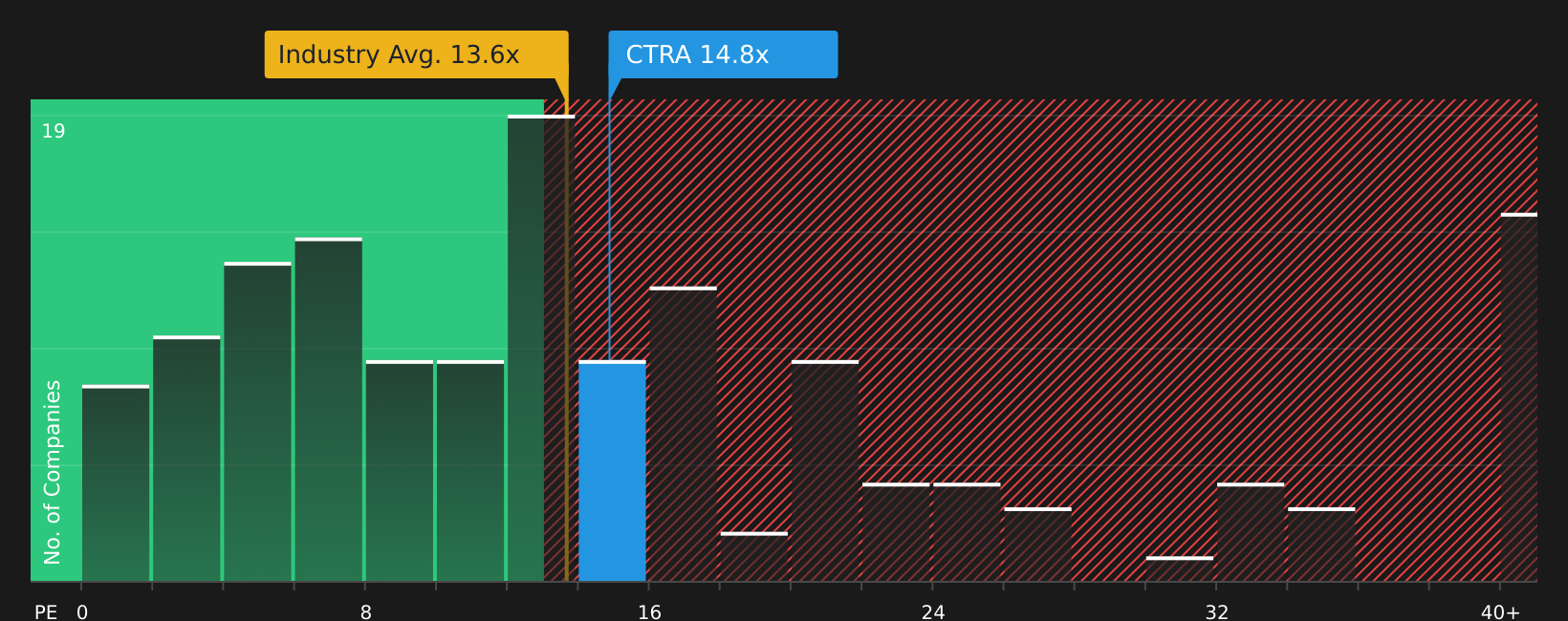

Approach 2: Coterra Energy Price vs Earnings

For profitable companies, the P/E ratio is a useful quick check because it links what you pay directly to the earnings the business is already generating. A higher P/E typically reflects stronger growth expectations or lower perceived risk, while a lower P/E can point to more modest growth expectations or higher risk.

Coterra Energy currently trades on a P/E of 14.09x. That sits close to both the Oil and Gas industry average P/E of 15.06x and the peer group average of 13.29x, so on simple comparisons the stock is in the same general range as its sector and similar companies.

Simply Wall St also estimates a proprietary “Fair Ratio” for Coterra Energy of 22.07x. This Fair Ratio is designed to be more tailored than a basic peer or industry comparison because it factors in elements such as the company’s earnings growth profile, profit margins, market capitalization, industry, and risk characteristics. By bringing those pieces together, it aims to show what a more company specific P/E could reasonably look like.

Comparing the Fair Ratio of 22.07x with the current P/E of 14.09x, the shares appear undervalued on this preferred multiple framework.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Coterra Energy Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Meet Narratives, a simple tool on Simply Wall St’s Community page where you connect your view of Coterra Energy’s story to a set of revenue, earnings and margin assumptions. These then roll into a Fair Value you can compare with the current price to decide whether the stock looks attractive, stretched or somewhere in between. The Narratives automatically refresh as fresh news or earnings arrive. For Coterra today, you might see one Narrative arguing for a higher Fair Value around US$42.56 based on stronger LNG contracts, cost savings and higher profit margins, alongside another more cautious Narrative closer to US$28.00 that leans on tougher gas pricing and margin pressure. This gives you a live range of informed views you can benchmark your own thinking against.

For Coterra Energy, however, we will make it really easy for you with previews of two leading Coterra Energy Narratives:

Fair value: US$37.36 per share

Implied gap to fair value: 14.7% below this narrative fair value at the recent price of about US$31.85

Revenue growth assumption: 7.76% a year

- Analysts backing this view see Coterra using its mix of oil and gas assets, along with drilling and completion efficiencies, to support steady cash flow and maintain relatively high profit margins.

- They are building in revenue growth, modest margin compression, and a small reduction in share count, which together support earnings of about US$2.0b by 2029 and a P/E of 17.4x, above the current US Oil and Gas industry P/E of 15.7x.

- Risks in this narrative include weaker for longer gas prices, operational issues in certain fields, higher regulatory and acreage costs, and the possibility that Tier 1 inventory becomes harder and more expensive to replace over time.

Fair value: US$25.55 per share

Implied gap to fair value: 24.6% above this narrative fair value at the recent price of about US$31.85

Revenue growth assumption: 12.0% a year

- This more cautious view still factors in LNG agreements, high return oil projects and capital efficiency, but argues that execution, pricing and regulatory risks justify a lower fair value than today’s share price.

- It highlights that while LNG exports, power demand and international pricing could lift revenue and margins, low regional gas prices, production curtailments and policy changes in areas such as New Mexico may offset some of that upside.

- The narrative also points to uncertainty around how global LNG markets, domestic energy policies and competing producers could influence Coterra’s ability to sustain premium valuation multiples over time.

Putting both together, you can see how different assumptions on gas pricing, LNG growth, operating reliability and capital discipline lead to a fairly tight bullish fair value above the current price, and a more conservative fair value below it. If you want to see how other investors are connecting their assumptions to specific fair values, and where your own view on Coterra fits along that spectrum, See what the community is saying about Coterra Energy

Do you think there's more to the story for Coterra Energy? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.