Is KKR (KKR) Now A Long Term Opportunity After Recent Share Price Weakness

KKR & Co KKR | 0.00 |

- If you are wondering whether KKR at around US$90.53 is priced for opportunity or risk, the starting point is to understand what the current share price implies about its underlying value.

- The stock has had a mixed run, with the share price down about 4.7% over the past week, down 12.4% over the past month, down 29.8% year to date and down 24.4% over the last year, while still showing a 69.0% gain over three years and 70.8% over five years.

- Recent coverage has focused on KKR's role as a large capital markets player and how broader sentiment toward alternative asset managers and financial stocks has been reflected in pricing. This context around the sector and investor risk appetite helps explain why shorter term moves look very different to the longer term returns.

- On Simply Wall St's valuation framework, KKR scores 3 out of 6. The rest of this article will walk through what different valuation approaches say about the stock and point to one more comprehensive way to think about value at the end.

Approach 1: KKR Excess Returns Analysis

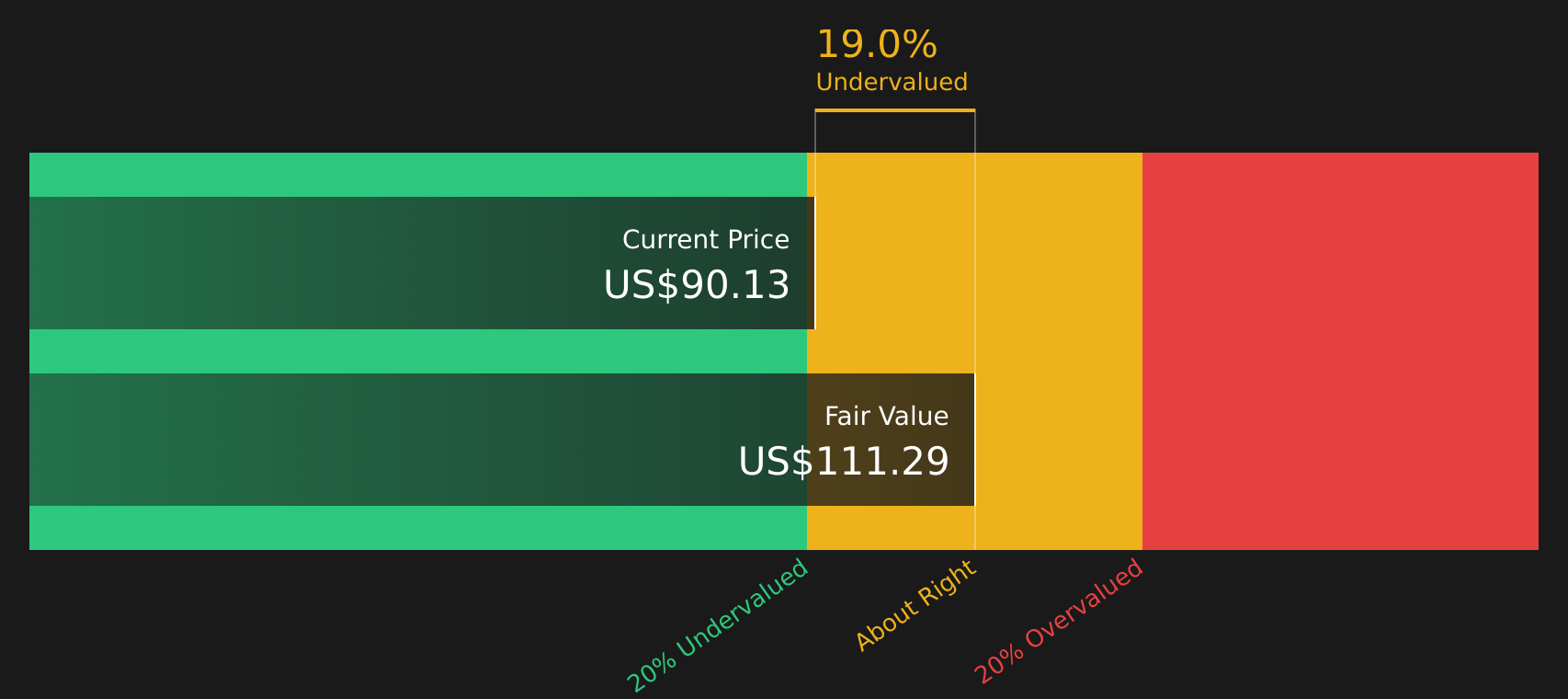

The Excess Returns model looks at how much profit KKR is expected to earn on its equity base after covering the cost of that equity, then capitalizes those “excess” profits into an intrinsic value per share.

For KKR, the model uses a Book Value of US$31.43 per share and a Stable EPS of US$8.71 per share, based on weighted future Return on Equity estimates from 5 analysts. The implied Cost of Equity is US$6.41 per share, so the Excess Return is US$2.30 per share. That excess is linked to an Average Return on Equity of 12.46% and a Stable Book Value of US$69.92 per share, sourced from weighted future Book Value estimates from 4 analysts.

On this basis, the Excess Returns framework arrives at an intrinsic value of about US$110.80 per share. Compared with the current share price of around US$90.53, this indicates the stock is trading at roughly an 18.3% discount, which suggests it screens as undervalued on this metric.

Result: UNDERVALUED

Our Excess Returns analysis suggests KKR is undervalued by 18.3%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Approach 2: KKR Price vs Earnings

For a profitable company, the P/E ratio is a useful way to think about what you are paying for each dollar of earnings, because it links the share price directly to current profitability.

What counts as a “fair” P/E depends on how the market views a company’s growth prospects and risk. Higher growth and lower perceived risk often support a higher P/E, while slower growth or higher risk tend to justify a lower multiple.

KKR currently trades on a P/E of 29.0x. That sits below the Capital Markets industry average of 39.3x, but above the peer group average of 22.0x. To go a step further, Simply Wall St’s Fair Ratio for KKR is 23.9x, which is an estimate of what its P/E might be based on factors like earnings growth, industry, profit margins, market cap and risk profile.

This Fair Ratio is more tailored than a simple comparison with peers or the industry, because it adjusts for KKR’s specific characteristics rather than assuming all companies should trade on the same multiple. On this basis, KKR’s current P/E of 29.0x sits above the Fair Ratio of 23.9x, which indicates that the stock screens as overvalued on this metric.

Result: OVERVALUED

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Upgrade Your Decision Making: Choose your KKR Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so this is where Narratives come in. They give you a simple way to attach your own story about KKR to hard numbers like fair value, future revenue, earnings and margins. You can then link that story to a financial forecast on Simply Wall St’s Community page so you can compare your Fair Value with the current price, see how it lines up with other investors’ views, watch it update automatically when new results or news arrive, and decide whether the stock looks more like an opportunity at the bullish end of the range with a Fair Value around US$150.18 or closer to the cautious view with Fair Value near US$84.45 or US$106.00.

For KKR however we will make it really easy for you with previews of two leading KKR Narratives:

Fair value in this bullish narrative: US$140.24 per share

Implied discount to that fair value at US$90.53: about 35% below the narrative fair value

Revenue growth assumption used in this narrative: a decline of about 17.85% a year

- Analysts in this narrative see KKR as a fee focused alternative asset manager, with fundraising, credit and asset based finance, and private markets exposure feeding into higher long run fee and performance revenue.

- The view leans on a large pool of unrealized carried interest, technology and origination investments, and ongoing data center and IPO pipeline activity to support future monetizations and earnings.

- Key risks flagged include credit quality, competition and fee pressure, reliance on performance income, and exposure to regulation and geopolitical events across global and emerging markets.

Fair value in this cautious narrative: US$84.45 per share

Implied premium to that fair value at US$90.53: about 7% above the narrative fair value

Revenue growth assumption used in this narrative: about 7% a year

- This narrative focuses on KKR as a long run capital compounder but stresses that a large share of its earnings is still tied to credit markets, insurance and complex balance sheet exposures.

- It uses a conservative Buffett style owner earnings framework, haircutting reported earnings, running credit stress tests on KKR’s US$329b credit platform and then comparing the outcome with peers like Blackstone and Apollo.

- The conclusion is that KKR’s business looks resilient under severe credit shocks, yet the stock can look more fully priced if investors assume benign credit conditions, so the margin of safety depends heavily on an investor’s view of private credit risk.

Do you think there's more to the story for KKR? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.