Is Lockheed Martin (LMT) Stock Still Reasonable After New Contract Wins?

Lockheed Martin Corporation LMT | 0.00 |

Lockheed Martin stock has delivered a 55.1% total return over the past 5 years, yet current checks suggest the shares may still trade below an intrinsic value estimate, with both the Discounted Cash Flow (DCF) work and earnings multiples pointing to upside compared with the recent price near US$514.99. At the same time, the share price has eased in the short term, which raises the question of whether the pullback is creating a valuation opportunity or simply reflecting execution and contract risk already visible in the news flow.

- Over 5 years, Lockheed Martin has returned 55.1%, which indicates investors have already seen meaningful gains while still debating how much value remains on the table.

- Large recent contract wins, such as new missile and radar work in the US and Europe, can support expectations for future cash flows. However, factors like program charges, integration of the Ultra Maritime acquisition, and defense budget decisions may pressure how much of that flows through to long term value.

- On Simply Wall St’s broader valuation checks, Lockheed Martin screens as undervalued in 5 out of 6 tests, which leans toward the stock looking cheap rather than fully priced on these measures.

The issue now is whether the current discount to the intrinsic value estimate is enough to compensate you for the contract, execution, and budget risks that come with owning Lockheed Martin at today’s price.

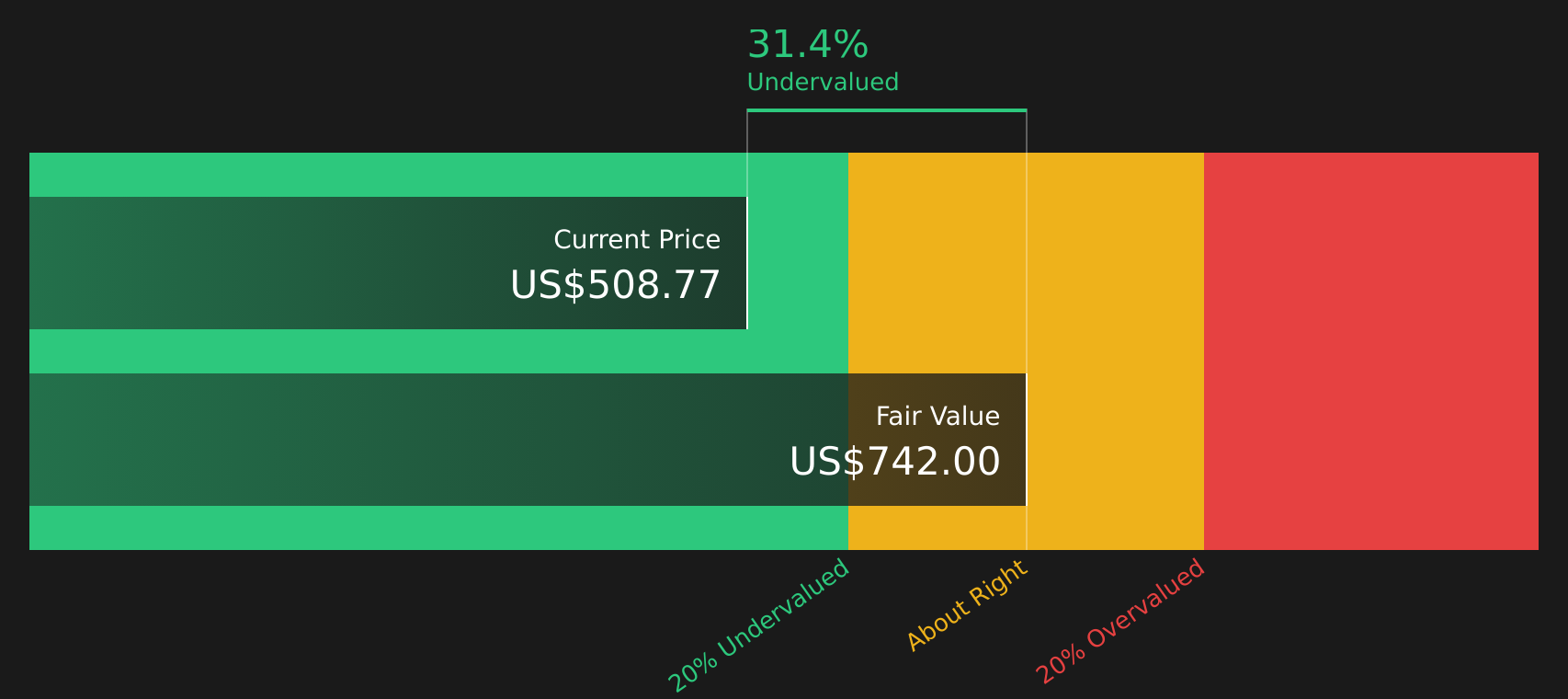

Is Lockheed Martin Still Cheap on Cash Flow?

The Discounted Cash Flow (DCF) model values Lockheed Martin by projecting future free cash flows and discounting them back to today. On this approach, the latest twelve month free cash flow is about US$5.6b, with the model assuming these cash flows continue growing rather than shrinking over time.

Those projections translate into an estimated intrinsic value of about $742 per share, compared with the recent share price around $515, implying the stock screens roughly 30.5% undervalued on this method. The recent stream of contract wins, including large missile and radar awards, is one factor that helps explain why the cash flow outlook in the DCF remains solid even as headline earnings have occasionally been mixed.

Overall, the DCF work suggests Lockheed Martin stock currently appears undervalued relative to the cash flows implied by its contract pipeline.

Our Discounted Cash Flow (DCF) analysis suggests Lockheed Martin is undervalued by 30.5%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Is Lockheed Martin Still Cheap on Earnings?

P/E is usually a clear snapshot for a mature, profitable contractor like Lockheed Martin because earnings are closely tied to long term programs and services. Lockheed Martin currently trades around 24.8x earnings, which is below the Aerospace & Defense industry average of about 40.5x and the peer group average near 48.0x.

A fair P/E multiple for Lockheed Martin, based on its scale, margins and risk profile, is estimated at 36.3x. That is a sizable gap to the current 24.8x, indicating that the market is applying a discount even though recent contract wins and a large backlog provide visibility on ongoing work. If earnings were valued in line with that fair multiple, the implied valuation would be higher than where the stock trades today.

On the P/E yardstick, Lockheed Martin stock appears undervalued compared with both its tailored fair multiple and sector pricing.

The Lockheed Martin Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where the Lockheed Martin valuation puzzle leaves off by spelling out which assumptions about future growth, margins and earnings would need to hold for the stock to be worth materially more or less than it is today. Each narrative ties a fair value estimate to a particular story about Lockheed Martin's potential catalysts and risks, so you can watch over time which version of events appears closer to reality on the Community page.

The community is split on Lockheed Martin, with one camp seeing meaningful upside still on the table while the other argues the stock already prices in most of what can go right.

Bull case: 18% undervalued

"Demand for advanced platforms such as the F-35, PAC-3, THAAD, and hypersonic weapons is being reinforced by actual combat use and rising geopolitical tensions..."

Bear case: roughly fairly valued

"The company's continued high reliance on a small set of large programs, including the F-35 and classified Aeronautics projects, creates significant vulnerability to evolving defense priorities or budget cuts..."

Do you think there's more to the story for Lockheed Martin? Head over to our Community to see what others are saying!

The Bottom Line

For investors weighing Lockheed Martin today, the key point is that both the Discounted Cash Flow (DCF) work and the earnings multiple view line up, with each suggesting the stock screens undervalued on current assumptions. The broader valuation checks also lean in the same direction. As a result, the debate is less about whether there is a discount and more about why it exists.

The crux from here is whether Lockheed Martin can execute on its large contract pipeline and manage budget and program risks well enough for that discount to close, or whether those risks prove persistent and the current pricing simply reflects them accurately.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.