Is nLIGHT (LASR) Justifying Its Rich Valuation Amid Cash Burn and Muted Growth?

NLIGHT, INC. LASR | 71.58 | -5.55% |

- Recently, commentary on nLIGHT highlighted that the laser manufacturer is experiencing muted revenue growth, ongoing cash burn, and weakening returns on capital, raising questions about the effectiveness of its current growth initiatives.

- The interesting twist for investors is that these operational challenges are arising while nLIGHT still trades on a relatively high forward earnings multiple, sharpening focus on whether its business model can support such a valuation.

- With these concerns around cash burn and returns on capital in mind, we’ll now examine how this latest development reshapes nLIGHT’s investment narrative.

Uncover the next big thing with 26 elite penny stocks that balance risk and reward.

nLIGHT Investment Narrative Recap

To own nLIGHT today, you need to believe its high energy laser technology and growing aerospace and defense exposure can eventually convert contract momentum into durable profits, even as the business currently burns cash. The latest concerns about muted revenue growth, weakening returns on capital, and cash usage sharpen the near term focus on whether existing defense programs and the industrial recovery can offset balance sheet strain. If these pressures persist, the key risk is that the high valuation multiple becomes harder to justify.

The recent US$175.0 million follow on equity offering is particularly relevant here, because it directly intersects with worries about ongoing cash burn and capital efficiency. While the raise bolsters nLIGHT’s financial flexibility to fund capacity expansion, R&D, and defense production, it also increases the share count at a time when the company remains loss making. For investors, this mix of fresh capital and continued losses brings the cash burn and dilution risk firmly into the spotlight.

Yet beneath the optimism around directed energy growth, you should be aware of how rising costs and persistent cash burn could eventually...

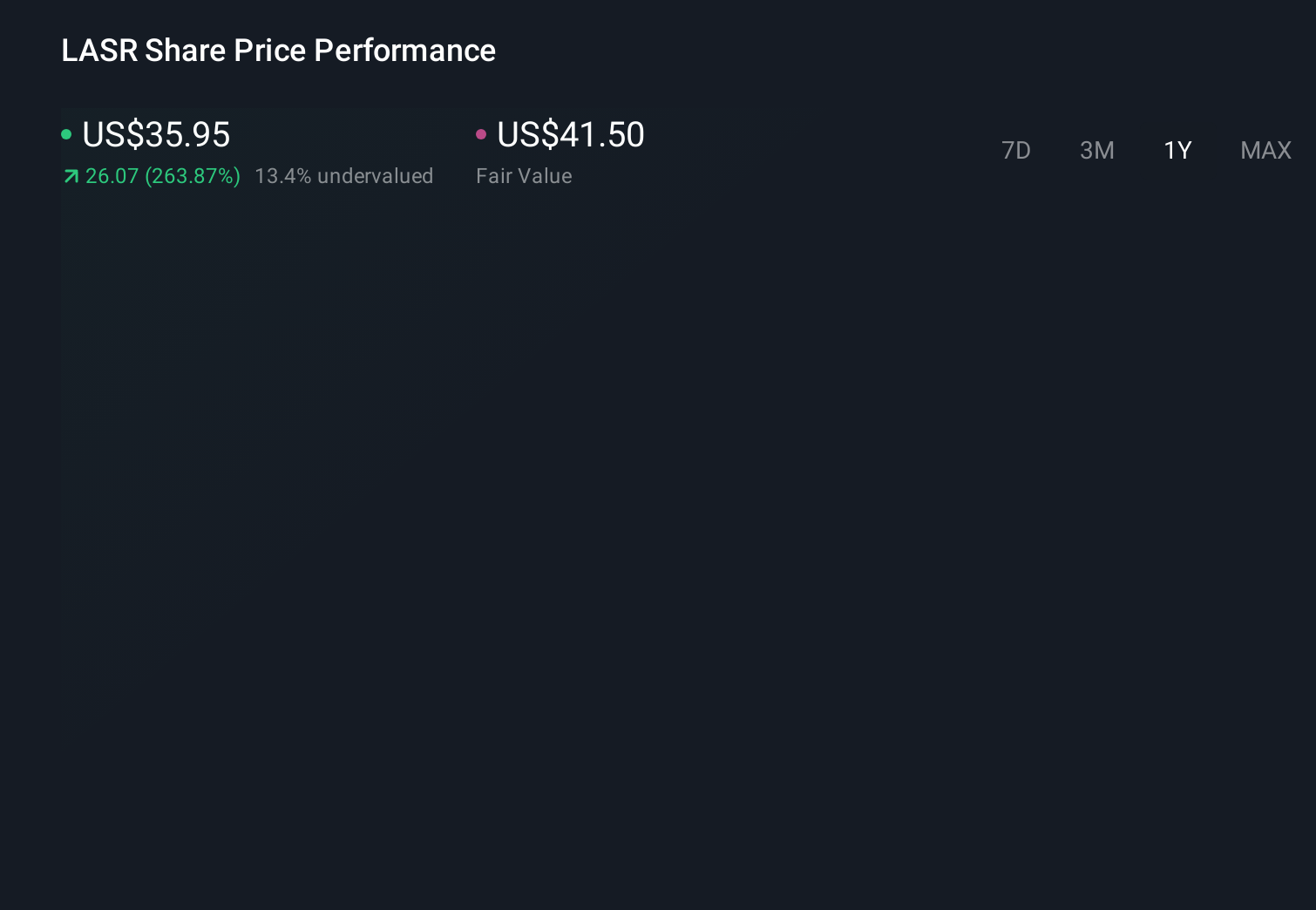

nLIGHT's narrative projects $415.9 million revenue and $23.2 million earnings by 2029.

Uncover how nLIGHT's forecasts yield a $73.50 fair value, in line with its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were modeling revenue of about US$432.2 million and earnings of roughly US$25.3 million by 2029, but with today’s questions around cash burn and heavy defense reliance, you can see how that much rosier scenario might need revisiting as different views on nLIGHT’s future emerge.

Explore 6 other fair value estimates on nLIGHT - why the stock might be worth as much as 29% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your nLIGHT research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free nLIGHT research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate nLIGHT's overall financial health at a glance.

Want Some Alternatives?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Find 61 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.