Is nLIGHT (LASR) Quietly Recasting Its Defense Profile With European Directed Energy Expansion?

NLIGHT, INC. LASR | 0.00 |

- In recent days, nLIGHT announced an expansion of its Torino, Italy operations to support growing European demand for locally assembled directed energy and high‑power laser subsystems, tailored to regional security and supply‑chain requirements.

- At the same time, the company’s strong first‑quarter aerospace and defense performance and new directed energy products have drawn increased attention to its defense‑oriented growth profile, even as executive share sales largely reflected tax‑related “sell to cover” transactions.

- We’ll now look at how the European directed energy expansion and defense momentum reshape nLIGHT’s existing investment narrative and risk balance.

The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

nLIGHT Investment Narrative Recap

To own nLIGHT today you need to believe its pivot toward aerospace and defense lasers can support a more durable, higher quality business, even as commercial demand and profitability remain uneven. The European directed energy expansion and strong first quarter A&D results appear to reinforce the near term defense growth catalyst, while the biggest current risk still looks tied to heavy reliance on a handful of large defense programs and how consistently nLIGHT can execute as amplifier and HEL volumes scale.

The Torino, Italy expansion stands out here, because it directly addresses one of nLIGHT’s main catalysts: broadening international directed energy revenue beyond U.S. programs. By enabling local assembly and lifecycle support for European and allied customers, this move connects recent defense momentum and the new HADES high energy laser line to a deeper, more regionally anchored pipeline, which could matter if U.S. funding patterns or specific contracts such as HELSI 2 eventually slow or shift.

Yet beneath the current optimism, investors should also be aware of how much depends on a concentrated set of defense contracts, amplifier ramp up, and...

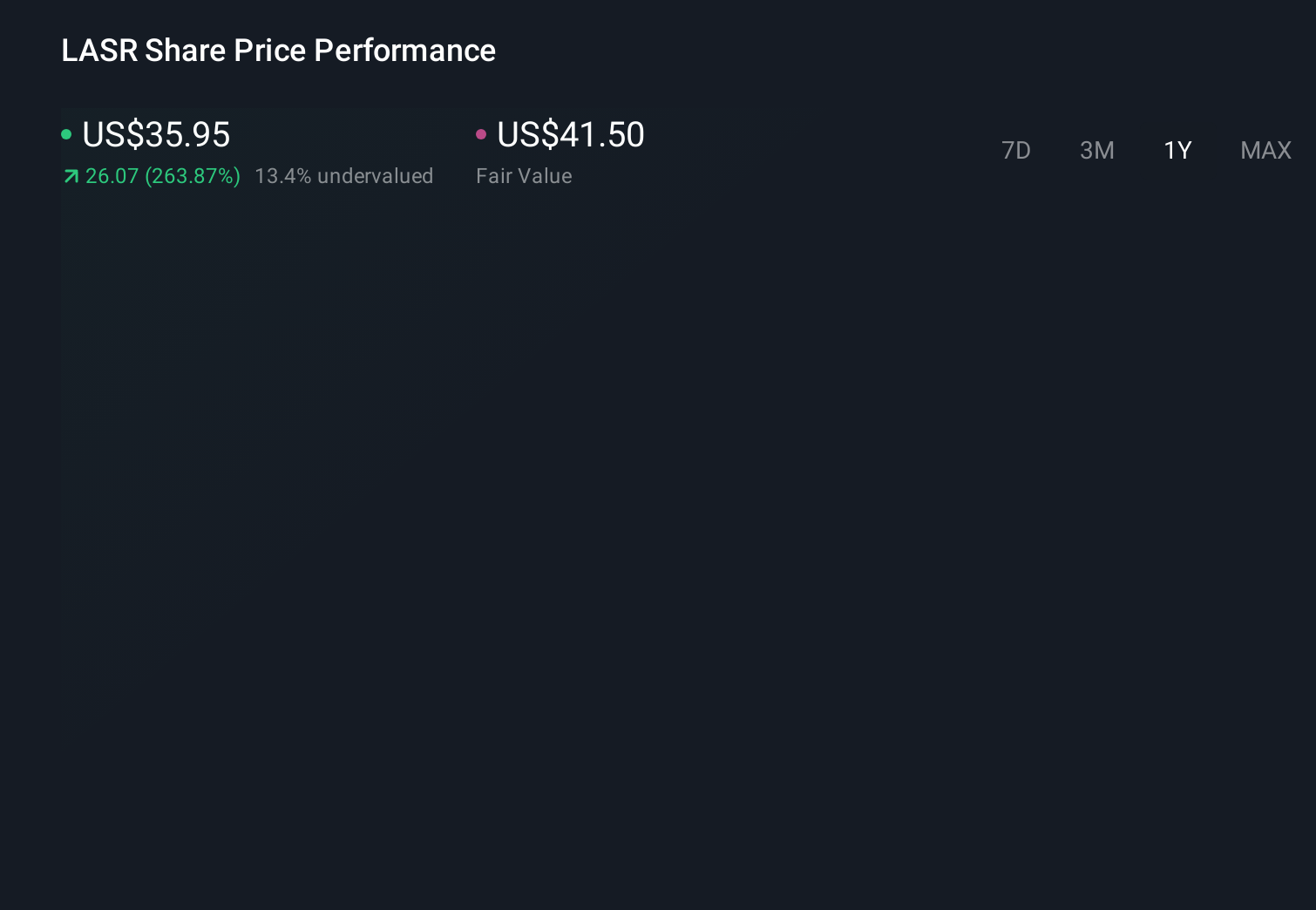

nLIGHT's narrative projects $454.9 million revenue and $8.2 million earnings by 2029.

Uncover how nLIGHT's forecasts yield a $85.00 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already assuming about 15.7 percent annual revenue growth and no profits by 2029, so their more cautious view on concentrated defense programs and amplifier manufacturing bottlenecks contrasts sharply with the current enthusiasm around Europe and HADES and suggests these bearish forecasts might shift meaningfully as the impact of the latest expansion becomes clearer.

Explore 6 other fair value estimates on nLIGHT - why the stock might be worth as much as 18% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your nLIGHT research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free nLIGHT research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate nLIGHT's overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Rare earth metals are the new gold rush. Find out which 27 stocks are leading the charge.

- Capitalize on the AI infrastructure supercycle with our selection of the 46 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.