Is Oceaneering International (OII) Fairly Valued Or Looking Stretched?

Oceaneering International, Inc. OII | 0.00 |

Oceaneering International stock has delivered a strong 214.1% return over the past five years, yet current valuation checks suggest the shares are trading at a premium, with both market multiples and an intrinsic value estimate pointing in the same direction.

- Over the last 5 years, Oceaneering International has returned 214.1%, which puts extra focus on whether today’s price already reflects much of that improvement.

- Winning a role in the U.S. Defense Innovation Unit’s undersea vehicle program can support longer term contract visibility. The expanded revolving credit facility means higher financial flexibility, but it also brings attention to how efficiently new capital is deployed.

- With a value score of 2 out of 6, Oceaneering International currently screens as leaning expensive rather than a clear bargain on the broader valuation checks.

The issue now is whether Oceaneering International’s recent gains justify paying what looks like an overvaluation premium, or if the current price leaves limited room for disappointment.

Has Oceaneering International Run Too Far on Cash Flow?

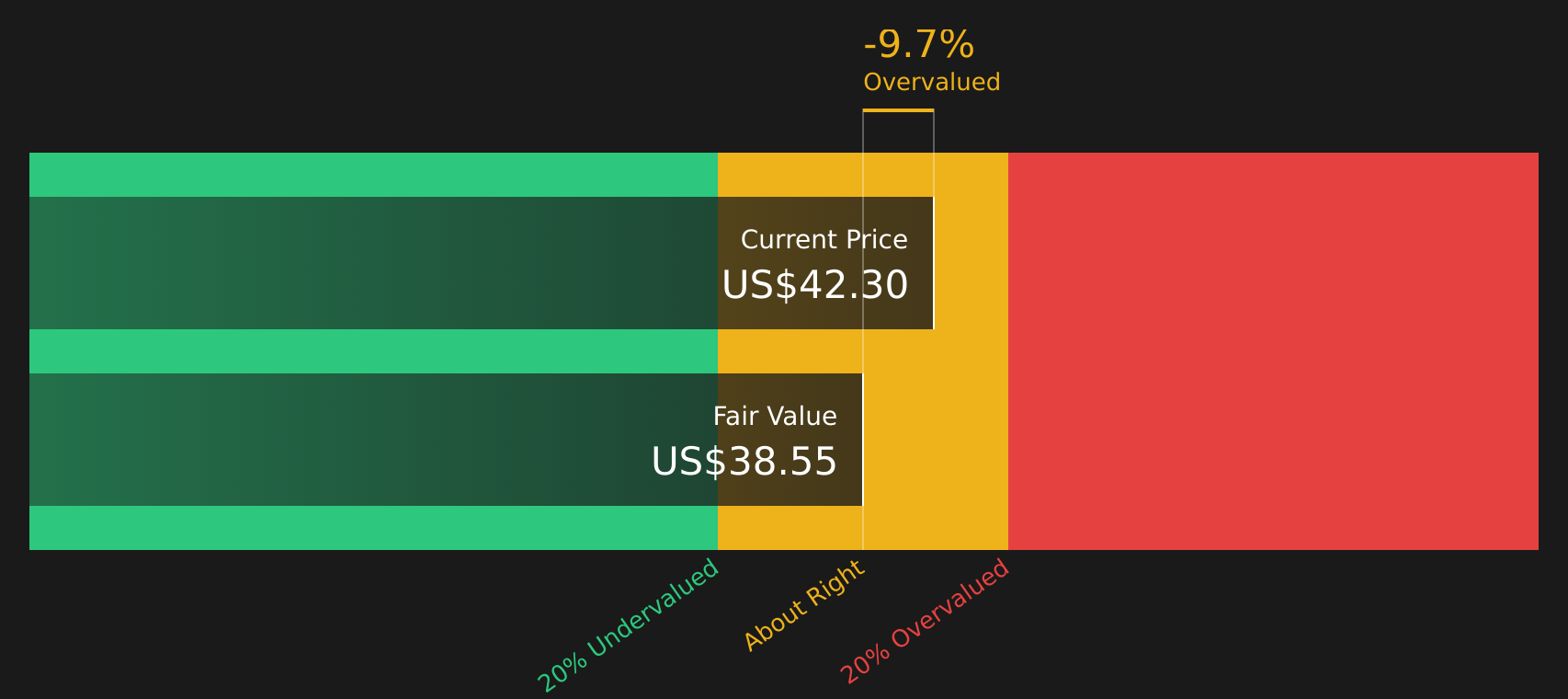

The Discounted Cash Flow (DCF) model used here looks at Oceaneering International’s projected free cash flows and discounts them back to today. Based on the latest twelve-month figures, the company is generating about $229.4 million of free cash flow, with the model assuming these cash flows broadly level off rather than compounding aggressively over the next decade.

Using those inputs, the DCF arrives at an estimated intrinsic value of about $38.55 per share, which is roughly 10.7% below the current share price. On this basis, the stock screens as overvalued using this method. The recent expansion of Oceaneering International’s revolving credit facility helps explain why the market might be willing to pay a premium, because greater liquidity can support ongoing projects and bidding for work such as the Defense Innovation Unit undersea vehicle program.

On balance, the DCF workup suggests Oceaneering International stock currently appears overvalued relative to its projected cash flows.

Our Discounted Cash Flow (DCF) analysis suggests Oceaneering International may be overvalued by 10.7%. Discover 47 high quality undervalued stocks or create your own screener to find better value opportunities.

Does Oceaneering International Look Pricey on Earnings?

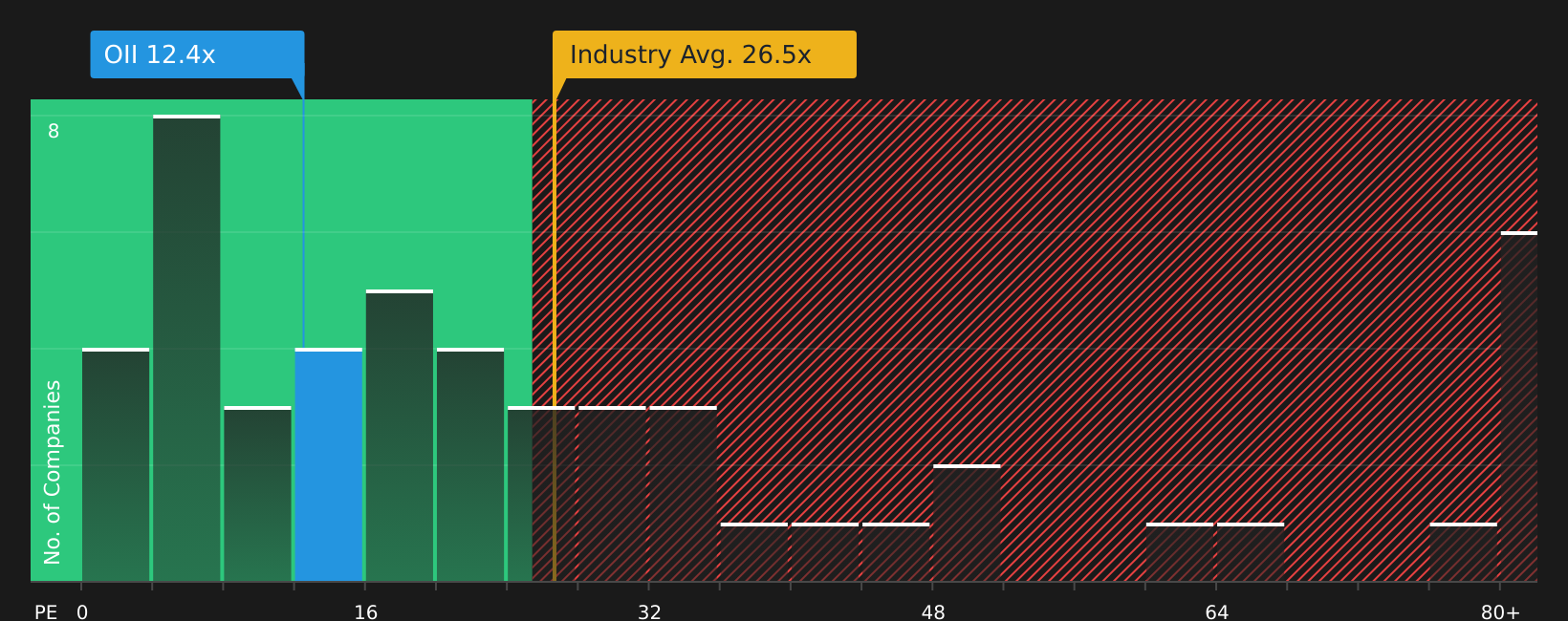

The P/E ratio is a useful cross check for Oceaneering International because earnings remain a key reference point for many investors in the Energy Services sector. Right now, the stock trades on a P/E of about 12.5x, which is well below the sector average of roughly 27.3x and also below the peer group average of around 30.2x.

However, a more tailored fair P/E for Oceaneering International, which considers its business profile and risk factors, is closer to 5.7x. Against that benchmark, the current 12.5x multiple is more than double what this framework would suggest. This indicates that the market is pricing in a premium relative to what these fundamentals might support.

Overall, based on this comparison with the fair P/E ratio benchmark, Oceaneering International stock currently trades at a higher multiple than that framework would imply.

The Oceaneering International Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Oceaneering International pick up where this valuation puzzle leaves off by spelling out what kind of future for growth, margins and earnings would need to play out for the stock to be worth materially more or less than today’s price. These Narratives are available on the company’s Community page. Each Narrative treats its implied fair value as a thesis about Oceaneering International’s business that you can watch over time, rather than a one off snapshot.

One of the top community narratives on Oceaneering International: 7% overvalued

"The company's sustained investment in next-generation robotics and digital automation unlocks high-growth opportunities in adjacent markets, such as offshore wind, carbon capture, and deep-sea mining..."

Do you think there's more to the story for Oceaneering International? Head over to our Community to see what others are saying!

The Bottom Line

For Oceaneering International, both the Discounted Cash Flow (DCF) estimate and the earnings multiple workup currently lean toward the stock being overvalued, rather than a clear opportunity on price alone. The broader valuation checks are also on the weak side, so the debate from here is less about hidden upside and more about how much optimism is already reflected in the shares.

The key question for you is whether Oceaneering International can deliver enough cash flow and earnings resilience to justify staying at or above this richer valuation, or whether the market eventually reins in that optimism.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.