Is Ongoing Sales Weakness and Softer Returns Reshaping the Investment Case For Pediatrix (MD)?

Pediatrix Medical Group, Inc. MD | 0.00 |

- Pediatrix Medical Group recently reported that sales have fallen each year for the past two years, with the latest outlook pointing to flat revenue and weakening returns on capital from its recent investments.

- This combination of declining top-line momentum and eroding capital efficiency has raised fresh questions about how effectively the company is allocating resources in its specialized pediatric and neonatal care portfolio.

- We’ll now examine how the ongoing sales decline and deteriorating returns on capital may influence Pediatrix Medical Group’s broader investment narrative.

Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

Pediatrix Medical Group Investment Narrative Recap

To own Pediatrix Medical Group today, you likely need to believe that its focused neonatal and pediatric franchise can offset recent sales pressure and weaker returns on capital through stable demand and disciplined cost control. The latest guidance for flat revenue and declining capital efficiency may weigh on sentiment around the near term earnings trajectory, while the biggest current risk is that portfolio changes and softer demand could turn recent revenue slippage into a more persistent downtrend.

The most relevant recent announcement here is the full year 2025 result, which showed sales of US$1,913.85 million compared with US$2,012.92 million the year before, confirming a second consecutive annual revenue decline. That print aligns with the new outlook calling for flattish sales and puts added focus on whether management can protect margins and cash generation without relying on further portfolio disposals or heavy cost cuts.

But beneath those headline numbers, there is an emerging risk around how much further Pediatrix can push hospital admin fees before partners and payers start to push back that investors should be aware of...

Pediatrix Medical Group's narrative projects $2.1 billion revenue and $171.4 million earnings by 2029. This requires 2.6% yearly revenue growth and about a $6 million earnings increase from $165.4 million today.

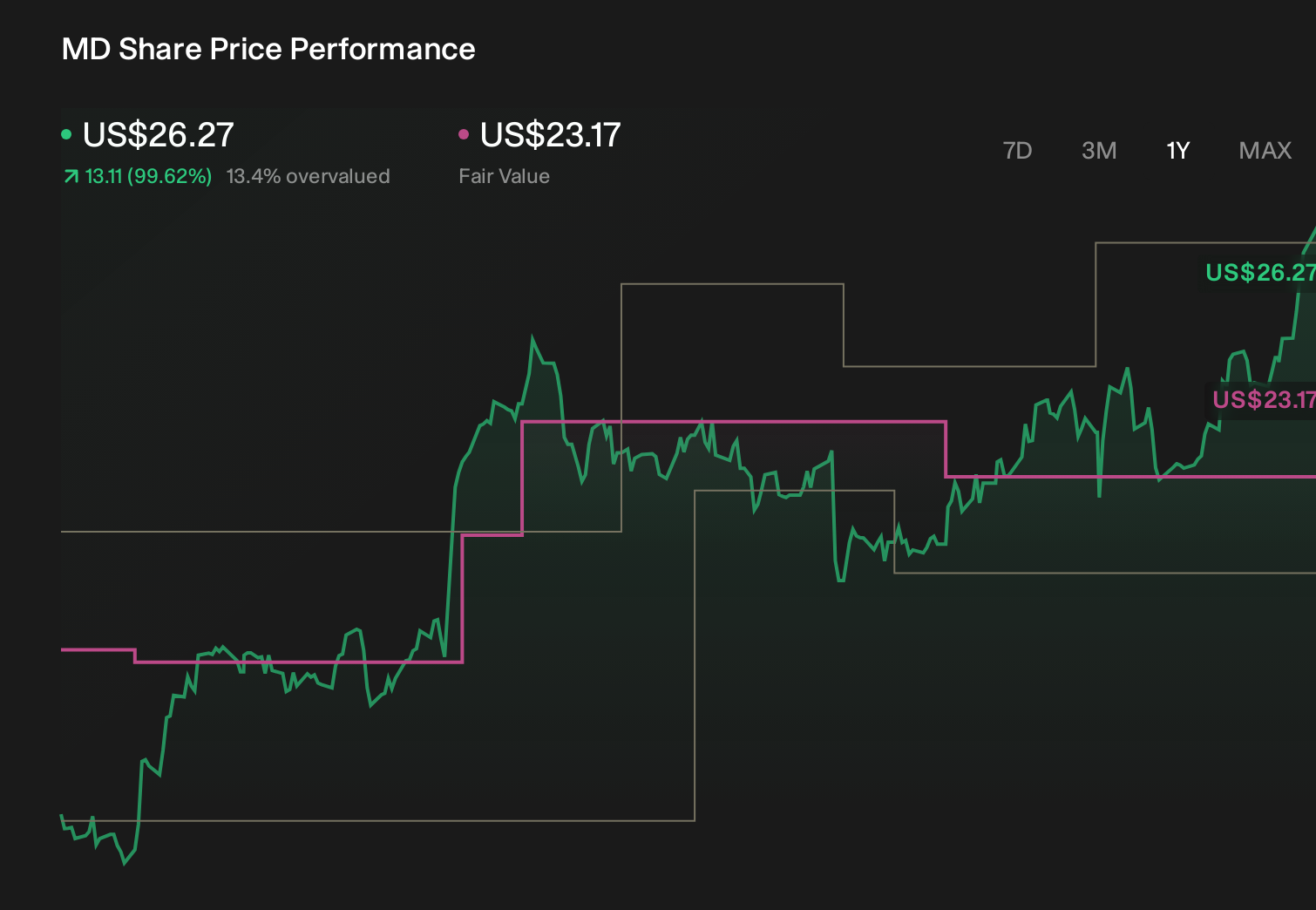

Uncover how Pediatrix Medical Group's forecasts yield a $21.33 fair value, a 11% downside to its current price.

Exploring Other Perspectives

Before this update, the most optimistic analysts were assuming Pediatrix could lift revenue to about US$2.1 billion and earnings to roughly US$184 million, which is far more upbeat than the baseline view and sits uncomfortably against fresh signs of flat sales and rising labor and hospital contracting risks that you now need to weigh for yourself.

Explore 6 other fair value estimates on Pediatrix Medical Group - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Pediatrix Medical Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Pediatrix Medical Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Pediatrix Medical Group's overall financial health at a glance.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.