Is Paysign’s (PAYS) Affordability Shift Redefining Its Core Profit Engine?

Paysign, Inc. PAYS | 0.00 |

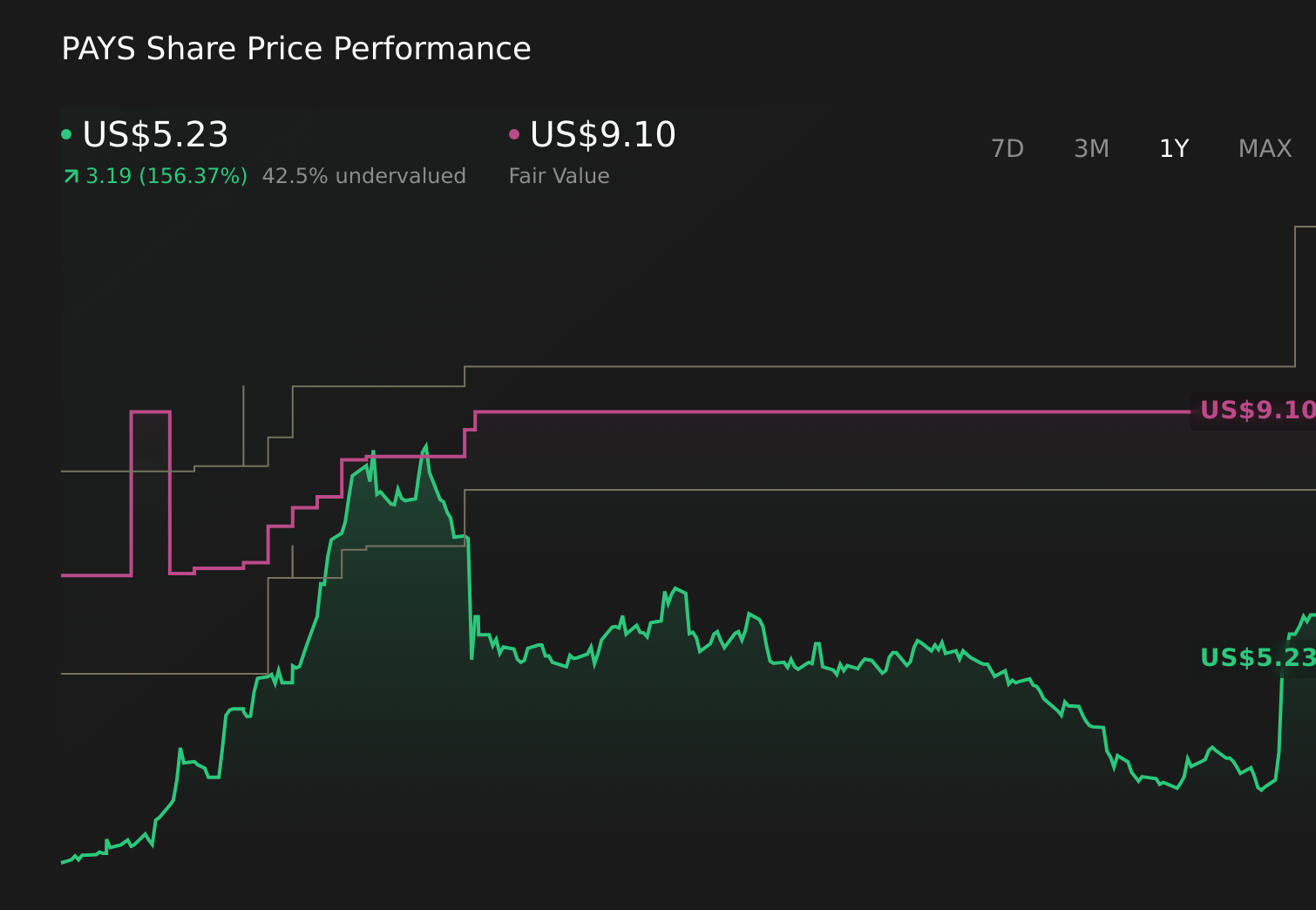

- Paysign, Inc. reported past first-quarter 2026 results on May 12, posting revenue of US$28.04 million and net income of US$5.44 million, with diluted EPS of US$0.09 from continuing operations.

- The quarter marked a shift as patient affordability programs became Paysign’s largest revenue contributor, reflecting a mix change toward higher-margin pharma offerings.

- We’ll now examine how this record first quarter and the rise of patient affordability as Paysign’s largest revenue stream affect its investment narrative.

Invest in the nuclear renaissance through our list of 87 elite nuclear energy infrastructure plays powering the global AI revolution.

Paysign Investment Narrative Recap

To stay invested in Paysign, you need to believe that its shift from plasma cards toward higher margin patient affordability programs can support profitable growth while managing concentration in just a few healthcare niches. The record Q1 2026 results, with patient affordability now the largest revenue stream, directly reinforce this thesis. In the near term, the biggest catalyst is continued program growth in pharma, while the key risk is that plasma headwinds or rising costs erode the benefit of this mix shift.

The most relevant recent announcement here is Paysign’s 2026 guidance, which points to full year revenue of US$106.5 million to US$110.5 million and net income of US$13.0 million to US$16.0 million. This frames Q1’s performance as part of a broader plan, but it also highlights execution risk: sustaining margins as the company invests in new capabilities, like its contact center and platform enhancements, is critical if the patient affordability catalyst is to remain the main driver.

Yet despite the strong quarter, investors should be aware that concentration in a few healthcare segments could still...

Paysign's narrative projects $124.4 million revenue and $15.5 million earnings by 2028. This requires 22.0% yearly revenue growth and a $8.7 million earnings increase from $6.8 million today.

Uncover how Paysign's forecasts yield a $9.10 fair value, a 57% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, penciling in about US$123.5 million of revenue and US$14.4 million of earnings by 2028, and worried that overdependence on plasma and pharma reimbursement could cap progress, which shows how differently you and other shareholders might interpret this new quarter and whether it softens or reinforces that more pessimistic view.

Explore 7 other fair value estimates on Paysign - why the stock might be worth 49% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Paysign research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Paysign research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Paysign's overall financial health at a glance.

Interested In Other Possibilities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 39 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.