Is Permian Resources’ (PR) Earnings Beat Streak Hiding a Deeper Operational Edge?

Permian Resources PR | 0.00 |

- Permian Resources has recently drawn attention after analysts highlighted its strong record of beating earnings expectations and flagged a positive setup for another potential earnings surprise ahead of its early May 2026 quarterly report.

- This ongoing pattern of outperformance against forecasts is sharpening focus on how effectively the company converts operational execution into consistent earnings resilience.

- We’ll now examine how this renewed optimism around another possible earnings beat influences Permian Resources’ investment narrative built on operational efficiency and growth.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 17 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Permian Resources Investment Narrative Recap

To own Permian Resources, you need to believe its operational efficiency in the Permian Basin can support resilient earnings and disciplined capital returns despite commodity and regulatory uncertainty. The fresh optimism around another earnings beat ahead of the May 2026 report reinforces that near term earnings momentum is a key catalyst, while commodity price volatility and the capital intensity of continuous drilling remain the most important risks. This latest news sharpens, but does not materially change, that near term setup.

The most relevant recent announcement here is the Q4 2025 and full year 2025 results, which showed net income of US$339.5 million for the quarter and US$935.2 million for the year, alongside production of about 401,475 Boe/d in Q4. Coupled with 2026 production guidance of 400,000 to 430,000 Boe/d, these figures provide the backdrop against which any new earnings surprise will be judged, and frame how investors assess the durability of the current earnings narrative.

Yet beneath the optimism around earnings beats, investors should be aware of how ongoing cost inflation and potential well productivity pressures could eventually...

Permian Resources' narrative projects $6.4 billion revenue and $1.3 billion earnings by 2029.

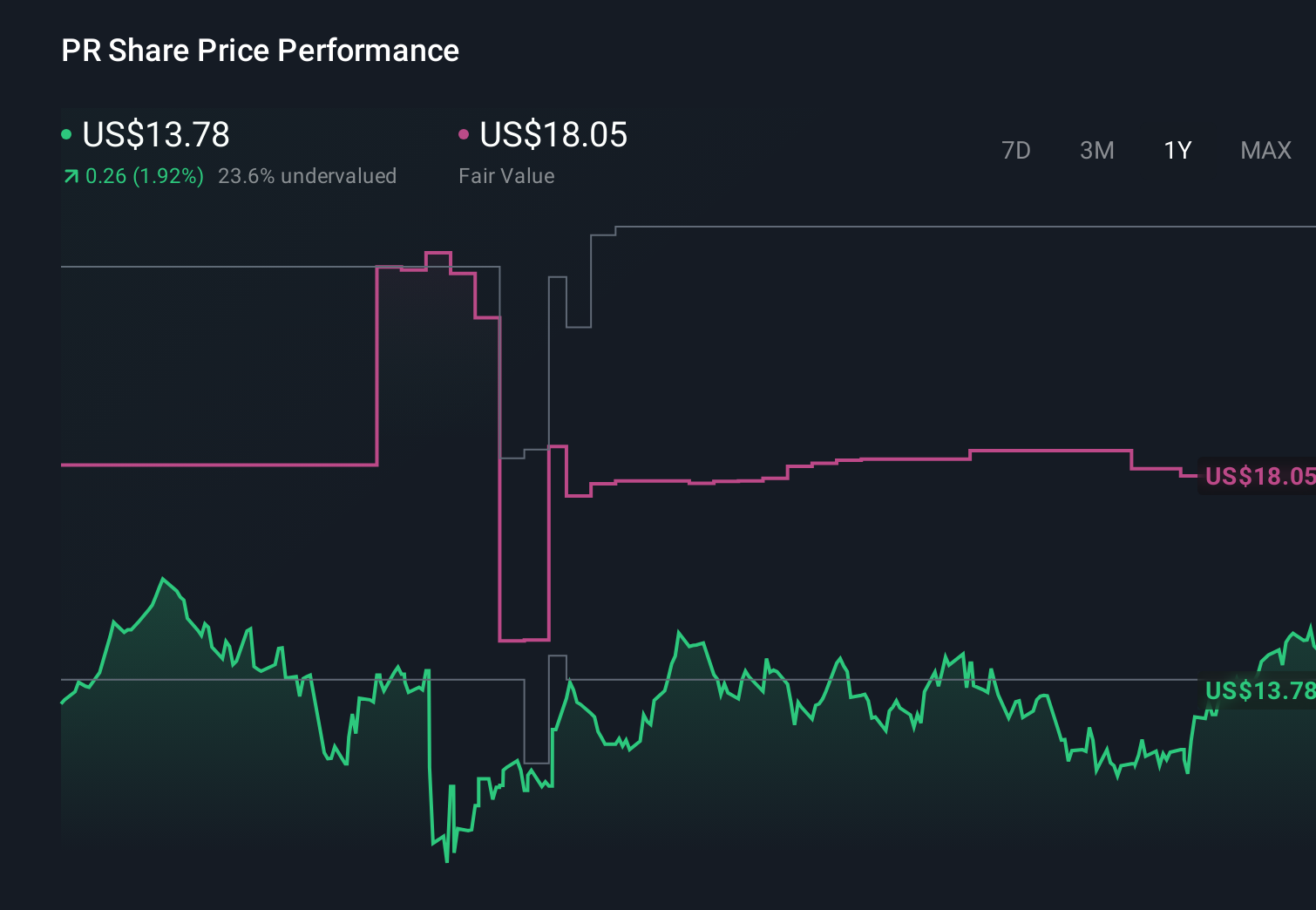

Uncover how Permian Resources' forecasts yield a $23.90 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already assuming only about 4.8 percent annual revenue growth to roughly US$5.8 billion and margin pressure, so this upbeat earnings setup could either challenge or reinforce their more cautious view depending on how the next few reports unfold.

Explore 6 other fair value estimates on Permian Resources - why the stock might be worth 14% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Permian Resources research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Permian Resources research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Permian Resources' overall financial health at a glance.

Interested In Other Possibilities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.