Is Pool (POOL) A Bargain After Russell Index Removals And Before Earnings?

Pool Corporation POOL | 0.00 |

Pool stock reacts to Russell index removals and upcoming earnings date

Pool (POOL) has been removed from several Russell growth benchmarks, including the Russell 1000 Growth and Russell Midcap Growth indexes, shortly before its scheduled second quarter 2026 earnings release on July 23.

Pool’s share price has been volatile around the index removals and upcoming earnings, with a 1 day share price return of 1.85% but a year to date share price return down 9.46%, alongside a 1 year total shareholder return down 31.70%. This points to fading longer term momentum despite some recent short term strength.

If you are reassessing Pool after this index change and earnings date, it can help to broaden your watchlist with 18 top founder-led companies

Bulls may highlight Pool’s revenue and net income growth alongside a lower share price, while bears focus on index exits and several years of underperformance as a warning. Which side does the current valuation appear to support?

Most Popular Narrative: 18.7% Undervalued

Pool’s most followed narrative points to a fair value of about $255.91 per share, compared with the recent $207.97 close. This sets up a valuation story built around modest growth assumptions and a specific required return of 7.2%.

The analysts have a consensus price target of $255.91 for Pool based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $300.0, and the most bearish reporting a price target of just $210.0.

Curious what sits behind that fair value gap for Pool? The narrative leans on measured revenue and earnings growth, firmer profit margins, and a richer future earnings multiple. The interplay between those three levers is what really moves the valuation.

Result: Fair Value of $255.91 (UNDERVALUED)

However, Pool’s reliance on mature North American housing, along with its sensitivity to inflation in labor and materials, could still undermine those margin and growth assumptions if conditions stay tough.

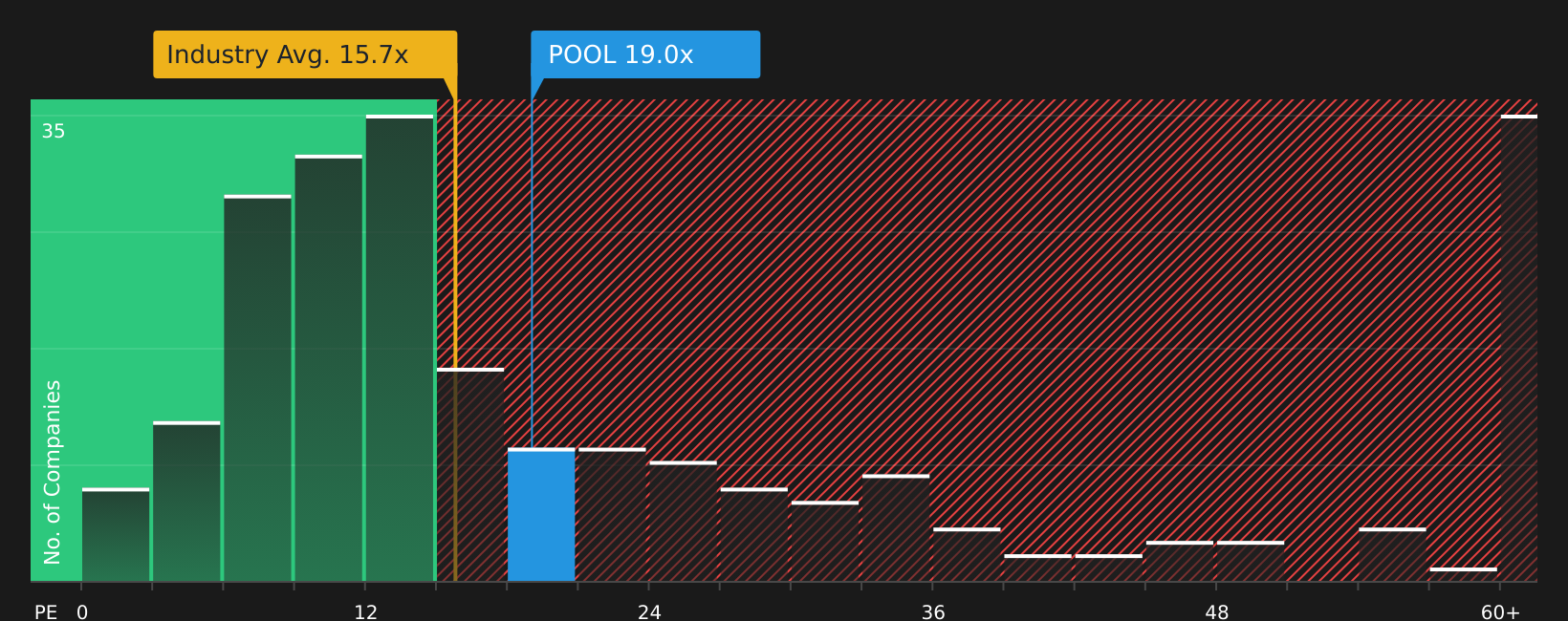

Another View: Pool through the earnings multiple lens

The earlier fair value narrative paints Pool as undervalued, but the current P/E of 18.8x tells a tougher story. It stands above the estimated fair ratio of 13.7x, the peer average of 12.8x, and the global Retail Distributors average of 15.6x. This suggests less room for error if growth or margins fall short. Which version of Pool’s valuation do you think better reflects the risks you care about?

To see how this pricing gap could close over time, and what it might mean for upside or downside, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With Pool caught between index exits, earnings expectations and mixed sentiment, it is worth reviewing the data yourself and acting promptly to decide where you stand with 4 key rewards and 1 important warning sign

Looking for more investment ideas beyond Pool?

If Pool’s story has you thinking harder about your portfolio, now is a good time to line up a few fresh ideas before the next move.

- Spot potential mispricings early by scanning 44 high quality undervalued stocks that combine solid fundamentals with more attractive valuations.

- Strengthen your portfolio’s foundations by checking out the solid balance sheet and fundamentals stocks screener (47 results) that can better handle tougher conditions.

- Get ahead of the crowd by reviewing a screener containing 19 high quality undiscovered gems before they hit everyone else's radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.