Is Popular (BPOP) Undervalued After The Analyst Upgrade On Earnings Optimism?

Popular, Inc. BPOP | 0.00 |

Popular (BPOP) is back in focus after an analyst upgrade linked to optimism around its earnings prospects and business fundamentals, a shift that often draws fresh attention from investors assessing bank stocks.

Against that backdrop, Popular’s momentum has been firm, with a 30-day share price return of 10.07% and a year-to-date share price return of 31.51%. The 1-year total shareholder return of 56.94% and 3-year total shareholder return near 3x suggest optimism around both earnings potential and risk profile.

If you are assessing how this kind of momentum compares with opportunities elsewhere in the market, it can be useful to widen the lens and review other financials and regional banks through a broader discovery tool such as the 20 top founder-led companies

With Popular’s share price already reflecting solid recent returns and analysts pointing to stronger earnings prospects, the key question now is simple: is the stock still undervalued, or is the market already pricing in future growth?

Preferred P/E of 11.9x: Is it justified?

Popular is currently trading on a P/E of 11.9x, which sits slightly below both its US Banks industry average and the peer group averages that have been provided.

The P/E multiple compares the share price to earnings per share and is a common way investors look at bank stocks because earnings tend to be a key driver of long term value. For Popular, the focus is on whether current and forecast earnings support this 11.9x level or point to something different over time.

On one side, Popular is flagged as trading at good value versus both peers and the broader US Banks industry, and its current P/E of 11.9x is below the industry average of 12.2x and peer average of 12.1x. In addition, the SWS fair value framework suggests the stock is good value relative to an estimated fair P/E of 12.4x, which is a level the market could potentially move toward if earnings and profitability trends stay aligned with current expectations.

Result: Price-to-earnings of 11.9x (UNDERVALUED)

However, Popular’s strong recent returns could be vulnerable if earnings or revenue growth of 7% to 8% slows, or if conditions in key Puerto Rico markets weaken.

Another view on Popular’s valuation

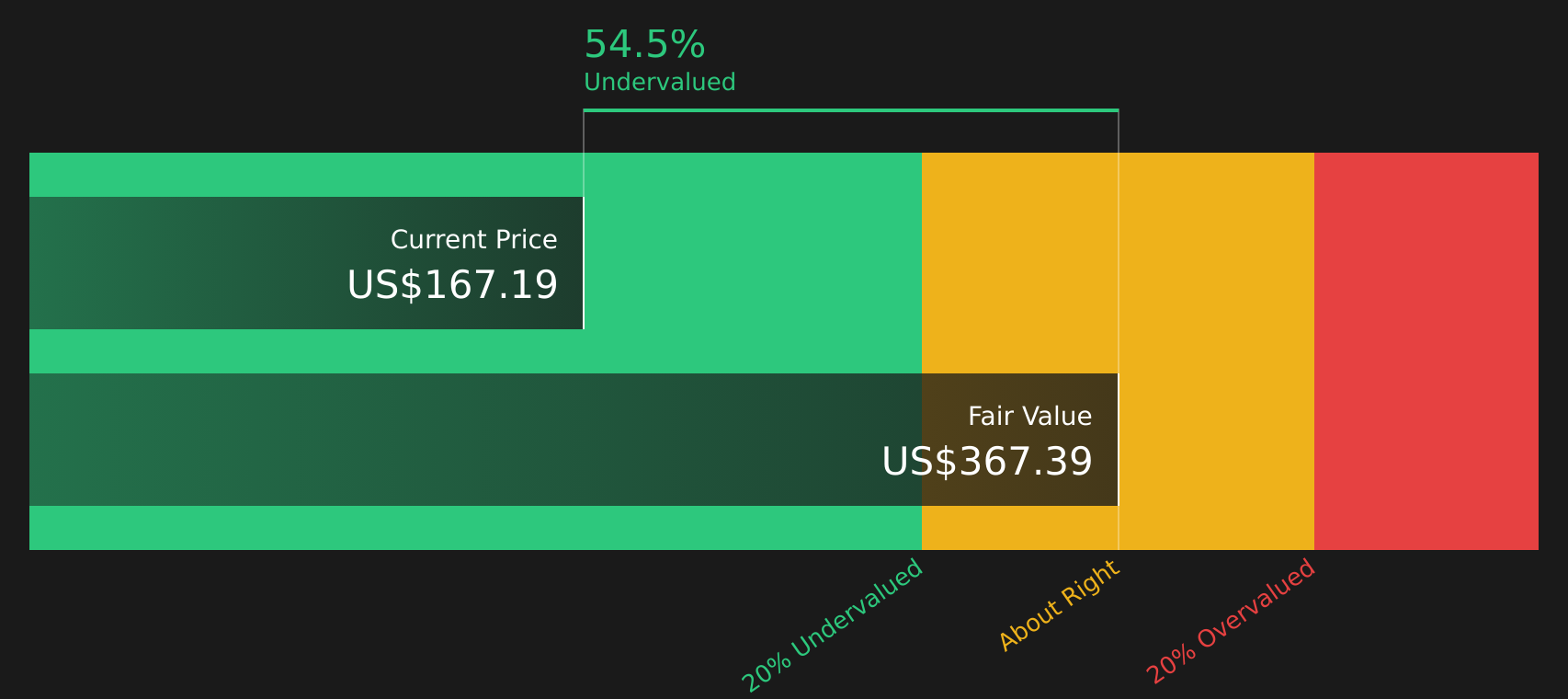

While Popular looks modestly cheap on its 11.9x P/E compared with peers and the US Banks industry, the SWS DCF model points to a very different picture. On this measure, the stock at $165.65 screens as heavily undervalued versus an estimated future cash flow value of $366.52.

That kind of gap can suggest either a meaningful opportunity or that the DCF assumptions are more generous than the earnings multiple implies. Which lens do you trust more for Popular at this stage?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Popular for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of optimism and caution around Popular leaves you undecided, it is worth reviewing the full picture yourself and weighing both sides quickly. To see how those risks and rewards balance out, take a closer look at the 5 key rewards and 1 important warning sign

Looking for more investment ideas beyond Popular?

If Popular has your attention, do not stop there. Use a few targeted stock lists to quickly surface other opportunities that match the kind of profile you care about most.

- Target potential mispricings by reviewing companies that screen as attractively valued using the 44 high quality undervalued stocks.

- Strengthen your income focus by checking out companies in the 7 dividend fortresses that pair higher yields with disciplined payout profiles.

- Prioritize resilience by scanning companies highlighted in the 69 resilient stocks with low risk scores, so you are not relying on Popular alone for stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.