Is Raised 2026 Guidance Altering The Investment Case For CACI International (CACI)?

CACI International Inc Class A CACI | 0.00 |

- CACI International Inc. recently reported third-quarter fiscal 2026 results, with sales of US$2,351 million and net income of US$130.39 million, and updated full-year guidance to revenue of US$9,500 million–US$9,600 million and net income of US$481 million–US$496 million.

- The company’s higher year-on-year sales and earnings, alongside raised full-year guidance, underline management’s confidence in its operating performance and earnings profile.

- We’ll now examine how CACI’s raised full-year revenue and earnings guidance may influence the existing investment narrative and outlook.

We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

CACI International Investment Narrative Recap

To own CACI, you need to believe that long term demand for secure, mission-focused technology and services to U.S. federal customers will remain resilient, and that CACI can keep winning and executing complex contracts. The Q3 FY2026 beat, higher year-on-year earnings, and raised full year guidance support this view in the near term. However, with over 90% of revenue tied to federal budgets, the biggest risk remains potential funding delays or cuts. This latest guidance update does not materially change that core risk.

One recent announcement that ties closely to this quarter’s results is CACI’s revised FY2026 guidance to revenues of US$9,500 million to US$9,600 million and net income of US$481 million to US$496 million. This update, coming alongside solid Q3 numbers, feeds directly into the main catalyst for the stock in the short term: evidence that CACI can translate its contract wins and backlog into consistent revenue and earnings delivery, despite ongoing competition and federal procurement uncertainty.

Yet investors should also be aware of how concentrated exposure to U.S. federal budgets could quickly become a problem if...

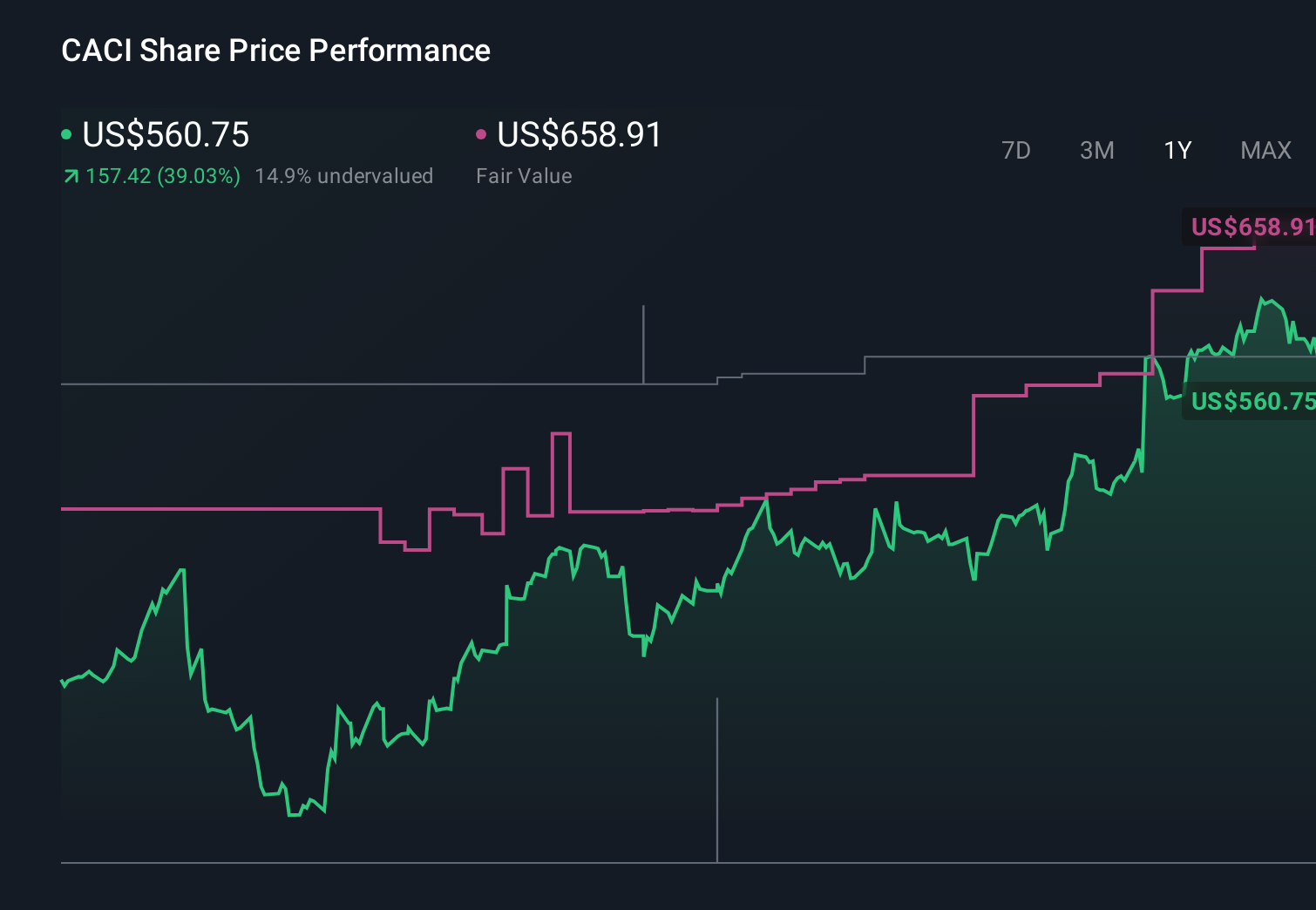

CACI International's narrative projects $11.9 billion revenue and $744.0 million earnings by 2029. This requires 10.0% yearly revenue growth and a roughly $225.6 million earnings increase from $518.4 million today.

Uncover how CACI International's forecasts yield a $709.23 fair value, a 38% upside to its current price.

Exploring Other Perspectives

While recent Q3 strength and higher FY2026 guidance look encouraging, some of the lowest analysts still frame CACI through a harsher lens, assuming revenue of about US$11.8 billion and earnings of roughly US$594 million by 2029, and warning that automation and budget scrutiny could compress margins faster than many expect, which shows how widely views on CACI’s future can differ and why it is worth comparing several perspectives before deciding what you believe.

Explore 3 other fair value estimates on CACI International - why the stock might be worth just $709.23!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your CACI International research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free CACI International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CACI International's overall financial health at a glance.

Seeking Other Investments?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.