Is Record FY Profits, EPS Miss And M&A Push Altering The Investment Case For Houlihan Lokey (HLI)?

Houlihan Lokey, Inc. Class A HLI | 0.00 |

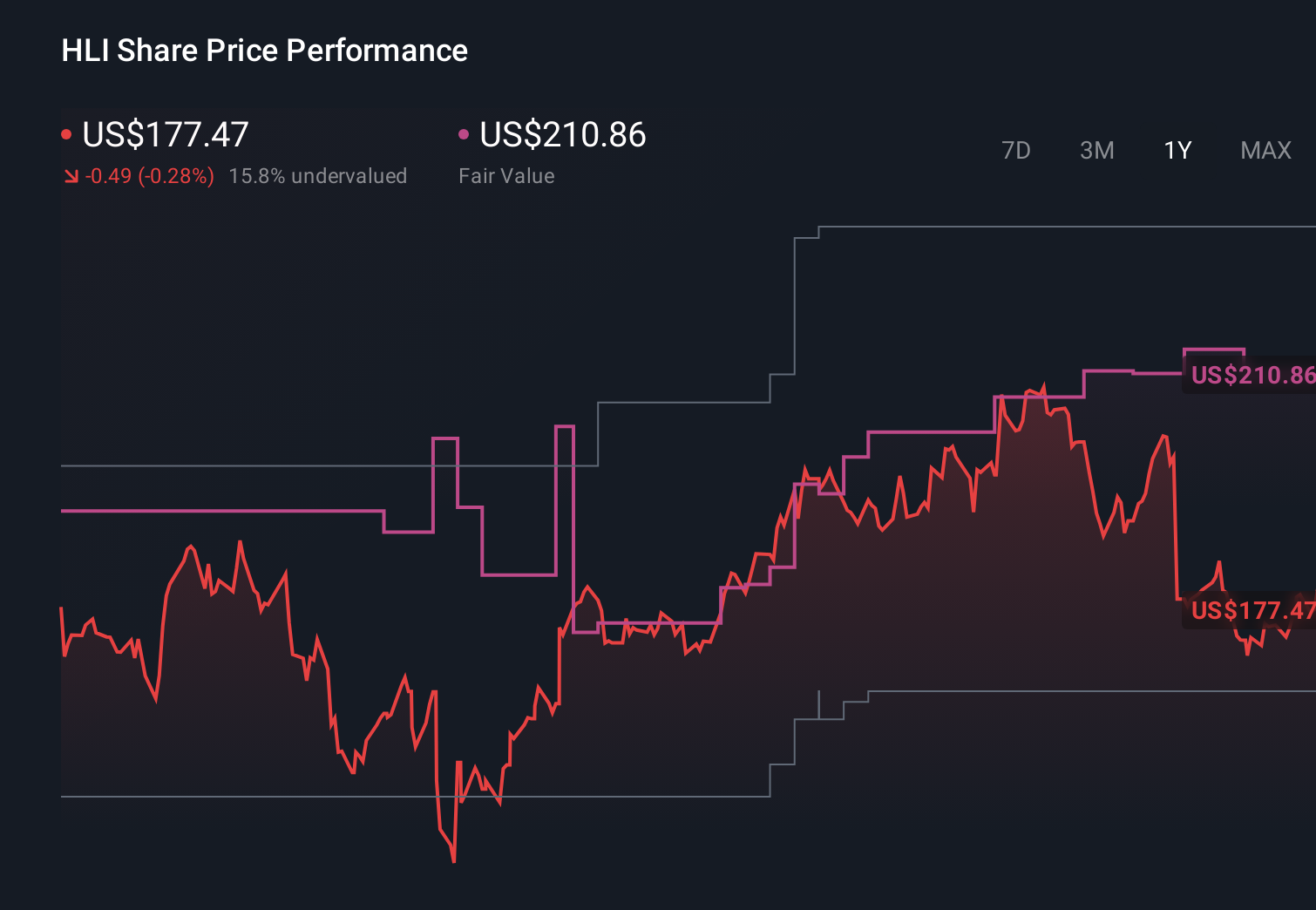

- In early May 2026, Houlihan Lokey reported a year-on-year decline in quarterly earnings per share alongside record full-year profits, raised its quarterly dividend to US$0.70 per share, and highlighted an active acquisition pipeline supported by balance sheet flexibility.

- Despite missing analyst expectations for the quarter, the firm ended fiscal 2026 with record revenue, strong performance across all advisory segments, and plans for further accretive acquisitions to reinforce its global platform.

- Now we’ll explore how softer-than-expected quarterly results and management’s acquisition focus might reshape Houlihan Lokey’s existing investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Houlihan Lokey Investment Narrative Recap

To own Houlihan Lokey, you need to believe that its diversified advisory model and balance sheet strength can offset choppy quarter-to-quarter results. Right now, a key near term catalyst is how quickly deal activity converts from the firm’s record backlog into revenue, while the biggest risk is that elevated costs and weaker-than-expected quarterly execution compress margins. The latest earnings miss and softer quarter do not appear to fundamentally change that risk reward balance in the short term.

The most relevant recent announcement here is management’s emphasis on an “as active as it has ever been” acquisition pipeline, backed by balance sheet flexibility. That matters because it ties directly to Houlihan Lokey’s catalyst of expanding its global advisory platform and fee pool, while also amplifying the existing risk that higher compensation and non compensation costs could weigh on profitability if new acquisitions and hires do not translate into stronger, more stable earnings.

Yet behind the upbeat talk about acquisitions and a record backlog, investors should be aware that concentrated exposure to U.S. driven deal cycles and rising expense levels could...

Houlihan Lokey's narrative projects $3.6 billion revenue and $641.9 million earnings by 2029. This requires 10.8% yearly revenue growth and about a $194 million earnings increase from $447.8 million today.

Uncover how Houlihan Lokey's forecasts yield a $174.50 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Before this earnings miss, the most optimistic analysts were assuming revenue could reach about US$3.8 billion and earnings about US$653 million by 2028, which is far more bullish than the baseline view and assumes Houlihan Lokey overcomes risks such as slower international expansion relative to peers; this contrast shows how widely opinions can differ, and why it is worth comparing several scenarios as fresh results and acquisition plans come through.

Explore 2 other fair value estimates on Houlihan Lokey - why the stock might be worth as much as 14% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Houlihan Lokey research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Houlihan Lokey research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Houlihan Lokey's overall financial health at a glance.

No Opportunity In Houlihan Lokey?

Our top stock finds are flying under the radar-for now. Get in early:

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 33 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.