Is Record Quarter, $1 Billion Notes, And Storage Push Altering The Investment Case For Ormat (ORA)?

Ormat Technologies, Inc. ORA | 0.00 |

- In the past quarter, Ormat Technologies reported record first‑quarter revenue growth of 75.8% year over year, completed a US$1.00 billion upsized convertible note offering, and advanced its portfolio with the Hoku solar‑plus‑storage acquisition, a new Jersey Valley solar‑plus‑storage PPA, and next‑generation geothermal and enhanced geothermal system initiatives.

- The combination of rapid Energy Storage and Product segment expansion with fresh financing capacity signals an acceleration of Ormat’s shift toward integrated clean power and storage solutions.

- Now we’ll examine how this record quarter and US$1.00 billion convertible note financing might influence Ormat Technologies’ longer‑term investment narrative.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

Ormat Technologies Investment Narrative Recap

To own Ormat Technologies, you need to believe in its ability to build a resilient, capital intensive clean power platform that combines geothermal, solar and storage. The record first quarter and US$1,000,000,000 convertible note increase financial flexibility, but they do not remove the key near term tension between heavy capex needs, high net debt to EBITDA of 4.4x, and the risk that funding costs could tighten.

Among the recent announcements, the upsized US$1,000,000,000 convertible note offering stands out as most relevant here, because it directly affects how Ormat can support its growth projects and manage its balance sheet. This fresh capital sits alongside growing Energy Storage operations, but it also raises questions about dilution, interest coverage and how efficiently future projects can turn that larger capital base into sustainable earnings.

Yet despite this strong quarter and new funding, investors should be aware of how reliant future returns may be on access to affordable capital and...

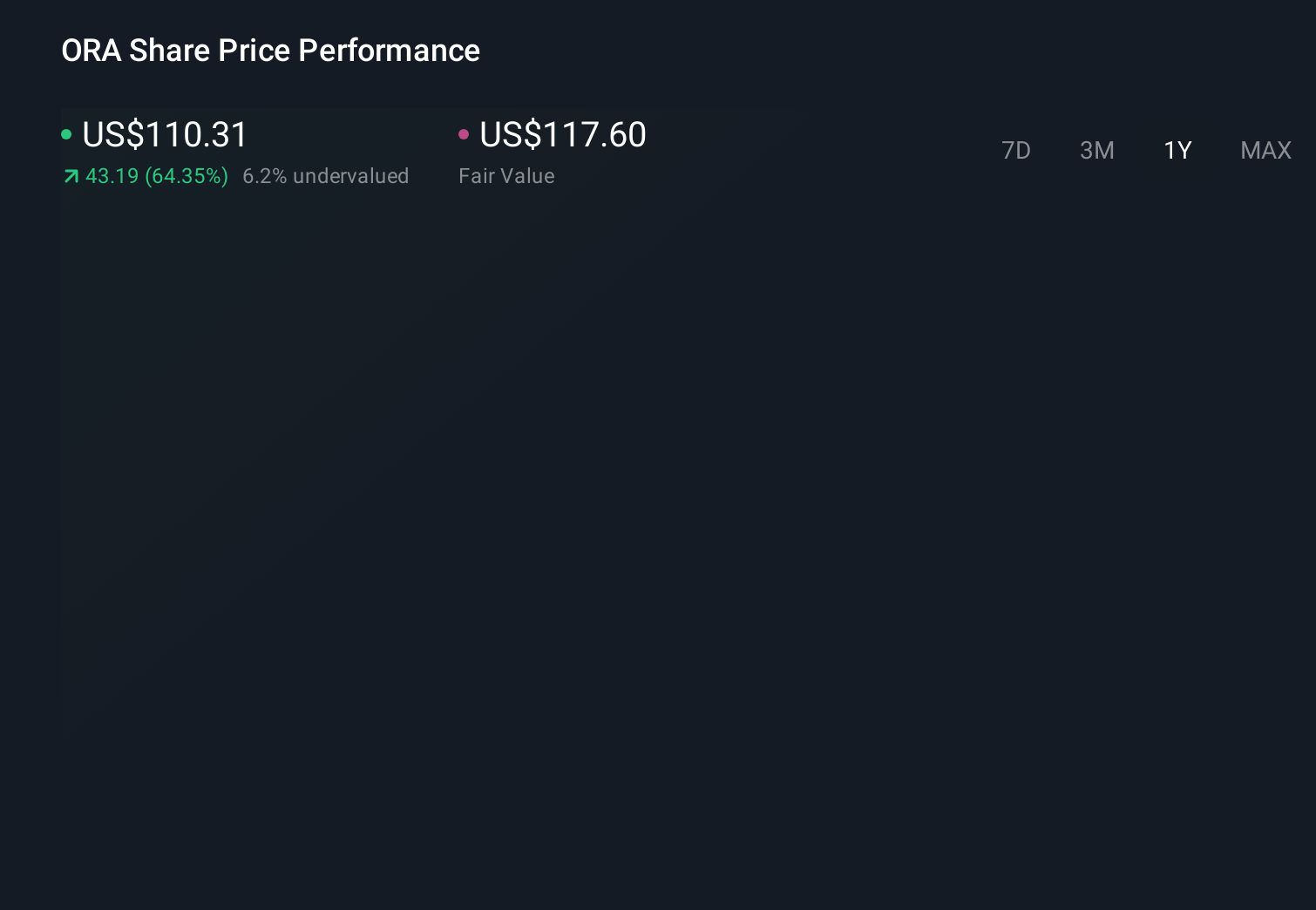

Ormat Technologies' narrative projects $1.3 billion revenue and $194.6 million earnings by 2029.

Uncover how Ormat Technologies' forecasts yield a $135.45 fair value, a 6% downside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community members currently estimate Ormat’s fair value between US$118.26 and US$178.09, underscoring how far opinions can diverge. Against that wide range, Ormat’s heavy capex plans and elevated leverage invite you to weigh how balance sheet risk could shape long term outcomes and to explore several contrasting views before deciding where you stand.

Explore 3 other fair value estimates on Ormat Technologies - why the stock might be worth as much as 23% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Ormat Technologies research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Ormat Technologies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ormat Technologies' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.