Is Rising Analyst Optimism Around Earnings Altering The Investment Case For Enterprise Products Partners (EPD)?

Enterprise Products Partners L.P. EPD | 0.00 |

- Earlier this week, Enterprise Products Partners reported that its upcoming earnings release is projected to show year-over-year growth in both earnings and revenue, supported by increasingly optimistic analyst estimates.

- The combination of improved forecasts and recent upward revisions in analyst expectations has drawn attention to Enterprise Products Partners’ near‑term business momentum and profitability outlook.

- We’ll now examine how rising analyst optimism around Enterprise Products Partners’ upcoming earnings could influence its broader investment narrative.

Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

Enterprise Products Partners Investment Narrative Recap

To own Enterprise Products Partners, you have to believe in the durability of its fee-based midstream infrastructure and its ability to manage a high debt load while funding growth projects and distributions. The recent uptick in analyst expectations for upcoming earnings reinforces the near term earnings catalyst around higher volumes and improved plant uptime, but it does not materially change the key risk that operational issues, such as unplanned downtime or tariff shifts, could still pressure cash flows.

In that context, the latest earnings report for Q1 2026, which showed higher net income alongside rising pipeline and marine terminal volumes, is particularly relevant. Those operating trends align with analyst optimism around earnings and revenue growth, while also tying directly into Enterprise’s core catalyst of bringing new processing, pipeline, and export capacity online to support higher throughput over time.

Yet investors should keep in mind that the same leverage which supports growth can quickly become a concern if credit conditions or interest costs move against Enterprise Products Partners...

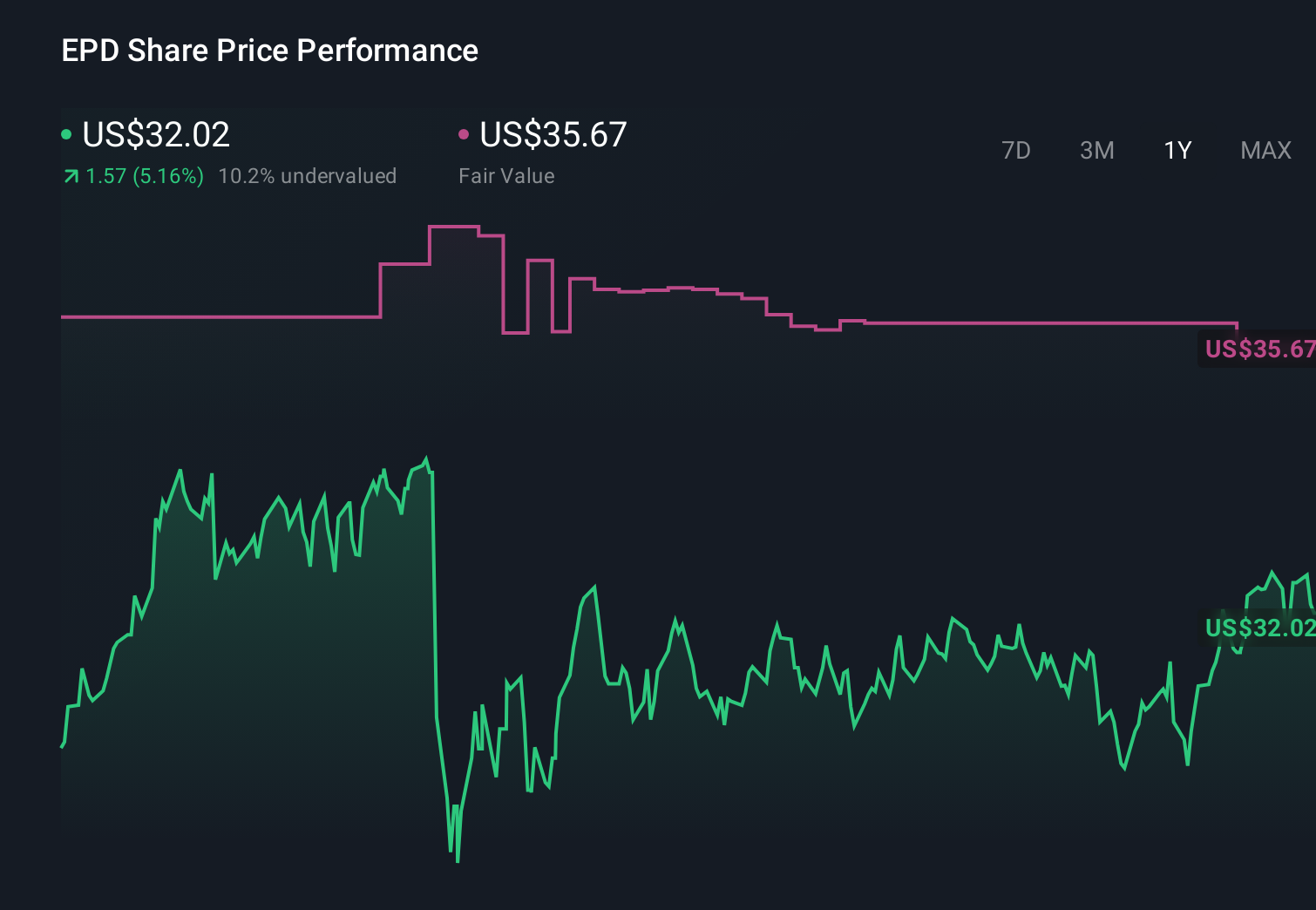

Enterprise Products Partners' narrative projects $61.3 billion revenue and $7.5 billion earnings by 2029. This requires 5.9% yearly revenue growth and about a $1.7 billion earnings increase from $5.8 billion today.

Uncover how Enterprise Products Partners' forecasts yield a $41.25 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Six members of the Simply Wall St Community currently value Enterprise Products Partners between US$35.25 and US$92.25, highlighting a wide spread of individual expectations. When you set those views against the near term focus on earnings growth and the ongoing risk from Enterprise’s sizeable US$31.9 billion debt load, it becomes clear that investor opinions can differ sharply and are worth comparing side by side.

Explore 6 other fair value estimates on Enterprise Products Partners - why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Enterprise Products Partners research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Enterprise Products Partners research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Enterprise Products Partners' overall financial health at a glance.

No Opportunity In Enterprise Products Partners?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.