Is Selective Insurance Group (SIGI) Overvalued Following Slower Growth And Weaker Margins?

Selective Insurance Group, Inc. SIGI | 0.00 |

Fresh concerns about slowing sales growth, weaker efficiency and earnings lagging peers have put Selective Insurance Group (SIGI) under closer scrutiny. This has prompted investors to reassess demand trends and profitability risks around the stock.

At a share price of $94.51, Selective Insurance Group has logged a 26.55% 90 day share price return and a 12.19% 1 year total shareholder return. This suggests momentum has picked up despite concerns around slowing growth and efficiency.

If recent moves in Selective Insurance Group have you reassessing your options, it may be worth broadening your watchlist to include 20 top founder-led companies

So, with Selective Insurance Group posting solid recent returns but facing slower sales growth and efficiency pressures, is the stock still trading below its estimated intrinsic value, or has the market already priced in its future growth potential?

Most Popular Narrative: 2.3% Overvalued

The most followed narrative for Selective Insurance Group puts fair value at $92.43, slightly below the last close at $94.51, which frames a modest valuation gap for investors to assess.

The company's ongoing focus and investments in operational efficiency, including data analytics, digital claims management, and underwriting tools, are expected to drive improved combined ratios and support margin expansion, leading to long-term net margin and earnings growth.

Want the full story behind that margin uplift? The narrative leans heavily on measured revenue growth, firmer profitability and a future earnings multiple that needs careful unpacking.

Result: Fair Value of $92.43 (OVERVALUED)

However, there are still clear warning signs, with casualty claim severity pressures and repeated reserve increases potentially undermining the Selective Insurance Group efficiency and earnings narrative.

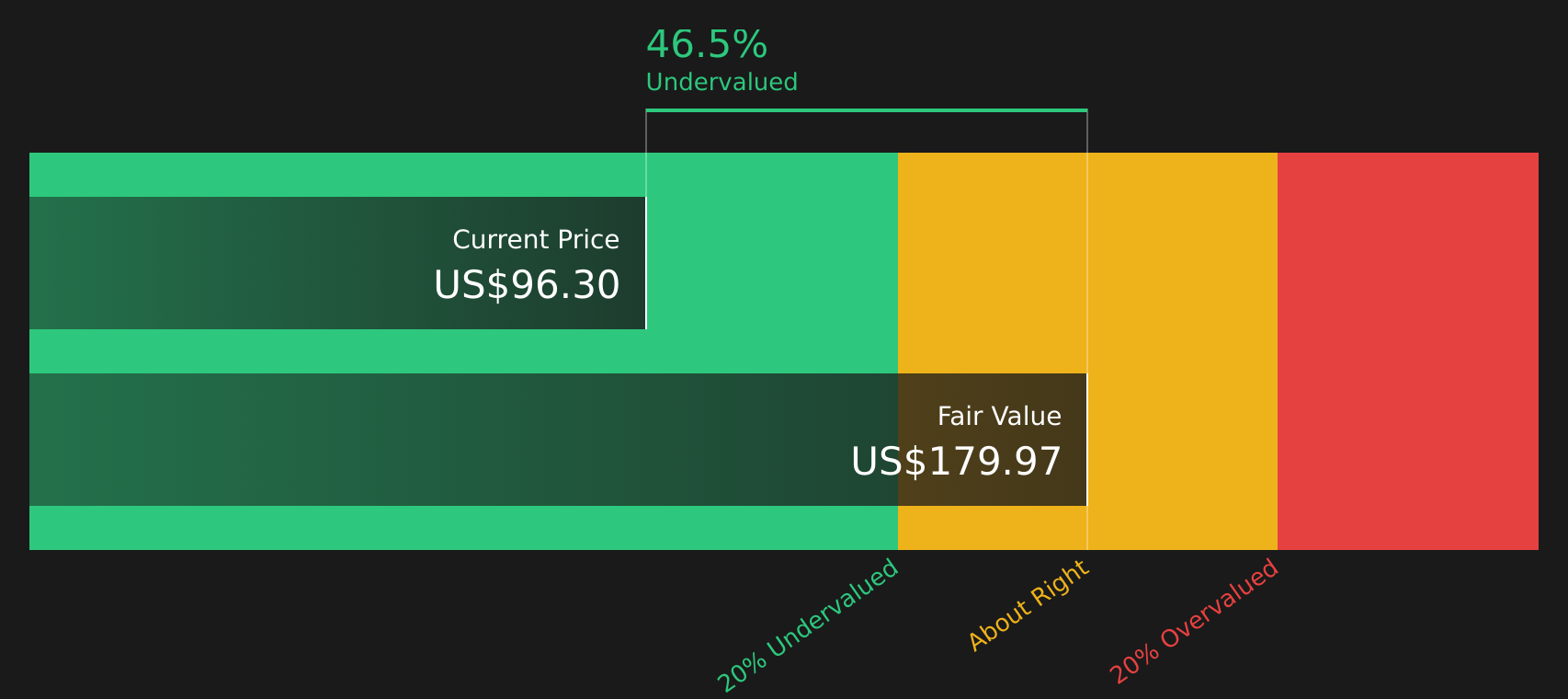

Another View: SWS DCF Points To A Very Different Fair Value For Selective Insurance Group

While the analyst narrative pegs Selective Insurance Group close to fairly valued at $92.43, the SWS DCF model tells a very different story, with a fair value estimate of $179.97. That gap, with the stock at $94.51, raises a simple question: which set of assumptions do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Selective Insurance Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 43 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals around Selective Insurance Group, do you see cautious concern or emerging opportunity, and how quickly do you want to firm up your view? To weigh those trade offs directly against the potential upside that some investors are focused on, take a closer look at the 4 key rewards

Looking for more investment ideas beyond Selective Insurance Group?

If you want a clearer view of how Selective Insurance Group compares, use the Simply Wall St screener to hunt for stocks that better fit your risk and return preferences.

- Target potential mispricing by scanning 43 high quality undervalued stocks that combine solid fundamentals with prices that may not fully reflect their underlying strength.

- Strengthen your income stream by checking out 9 dividend fortresses that focus on higher yields with an eye on sustainability.

- Dial back risk while staying invested by reviewing 67 resilient stocks with low risk scores that aim for resilience when conditions become more uncertain.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.