Is Strong Quarterly Performance And Rising Institutional Ownership Altering The Investment Case For Customers Bancorp (CUBI)?

Customers Bancorp, Inc. CUBI | 0.00 |

- On 10 June 2026, Customers Bancorp’s CEO Samvir S. Sidhu presented at the Morgan Stanley US Financials Conference in New York, shortly after the bank reported year-over-year growth in both revenue and net profit alongside a high but financially weak health score of 8.24.

- At the same time, institutional ownership climbed to just over the company’s share count, with major investors like BlackRock and Wellington increasing positions even as Customers Bancorp’s valuation score sat mid-pack within the Banking Services industry.

- We’ll now examine how this combination of strong quarterly financial performance and rising institutional ownership could reshape Customers Bancorp’s investment narrative.

The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Customers Bancorp Investment Narrative Recap

To own Customers Bancorp, you need to believe its tech-focused commercial model and cubiX platform can keep attracting sticky deposits and fee income while managing niche risks in digital assets and specialty lending. The standout short term catalyst remains how sustainably the bank can grow earnings from this franchise; the Morgan Stanley conference appearance, paired with strong quarterly revenue and profit growth, supports that story but does not materially change the biggest risk around concentrated digital asset and stablecoin-related deposits.

Against this backdrop, the recent buyback activity, with US$42.3 million of stock repurchased in Q1 2026 under a US$100 million authorization, is particularly relevant. It sits alongside rising institutional ownership and a mid-range valuation score, reinforcing that capital deployment is an active part of the current thesis, even as management balances ongoing investment in technology, compliance, and new banking teams that could pressure margins if revenue growth slows.

Yet in contrast, investors should be aware that heavy spending on technology and compliance could start to weigh on returns if revenue growth...

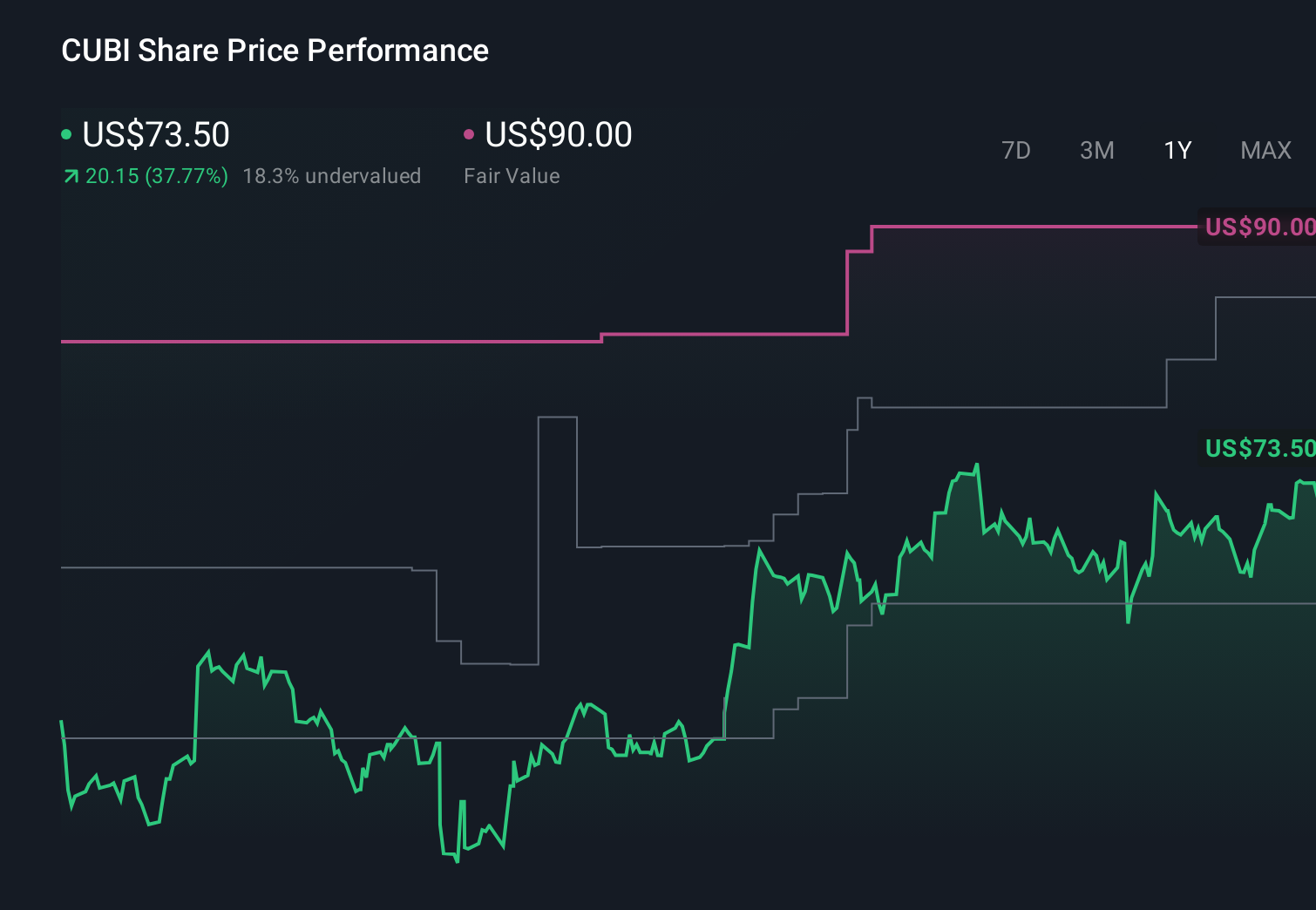

Customers Bancorp's narrative projects $958.3 million revenue and $389.4 million earnings by 2029.

Uncover how Customers Bancorp's forecasts yield a $90.18 fair value, a 19% upside to its current price.

Exploring Other Perspectives

While some of the lowest analysts assumed earnings might reach about US$381.1 million by 2029, they pair that with worries about rising compliance costs and tougher fintech competition, reminding you that views on Customers Bancorp’s future can differ sharply and may shift again after this latest conference spotlight and earnings surprise.

Explore 3 other fair value estimates on Customers Bancorp - why the stock might be worth just $90.18!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Customers Bancorp research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Customers Bancorp research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Customers Bancorp's overall financial health at a glance.

Want Some Alternatives?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.