هل تؤثر الصدمة الأخيرة في أسعار النفط على جدوى الاستثمار في مجموعة حلول الطاقة Helix Energy (HLX)؟

Helix Energy Solutions Group, Inc. HLX | 0.00 |

- في الأسبوع الماضي، لفتت مجموعة "هيليكس إنرجي سوليوشنز" الأنظار مع ارتفاع أسعار النفط الخام إلى ما يزيد عن 100 دولار أمريكي للبرميل وسط تصاعد التوترات الجيوسياسية ومخاوف بشأن الإمدادات، بما في ذلك هجمات الطائرات بدون طيار على منشأة نووية في الإمارات العربية المتحدة والاضطرابات حول مضيق هرمز.

- أبرزت هذه الصدمة في أسعار النفط مدى حساسية أعمال شركة Helix للتحولات في النشاط البحري وأسواق السلع الأساسية التي يمكن أن تغير بسرعة اقتصاديات العقود وتوقيت المشاريع.

- سندرس الآن كيف يتقاطع هذا الارتفاع الحاد في أسعار النفط والتوتر الجيوسياسي مع سردية الاستثمار طويلة الأجل القائمة على العقود وملف المخاطر الخاص بشركة Helix.

تفوق على العمالقة: هذه الأسهم الـ 15 الناشئة في مجال الذكاء الاصطناعي قد تمول تقاعدك .

ملخص سرد استثمارات مجموعة حلول الطاقة من هيليكس

لامتلاك أسهم في مجموعة Helix Energy Solutions، يجب أن تؤمن بأن عقود التدخل البحري طويلة الأجل، وإيقاف تشغيل المنشآت، وعقود الروبوتات قادرة على تعويض التقلبات قصيرة الأجل في أسعار النفط ونشاطه. صحيح أن الارتفاع الأخير في أسعار النفط الخام فوق 100 دولار أمريكي للبرميل قد عزز سعر السهم، إلا أنه لا يغير جوهرياً المحفز الرئيسي الحالي، وهو اندماج Hornbeck المقترح، أو أكبر المخاطر على المدى القريب، والذي لا يزال يتمثل في تأجيل المشاريع وضغوط الأسعار في قطاعات السوق الفورية الأكثر عرضة للخطر.

أهم إعلان حديث في هذا السياق هو اندماج شركة هيليكس المزمع بالكامل مع شركة هورنبيك للخدمات البحرية، والذي يهدف إلى إنشاء منصة متكاملة أكبر للخدمات البحرية. وبينما قد يدعم ارتفاع أسعار النفط الاستخدام والتسعير على المدى القريب، فمن المرجح أن يكون لنتائج الاندماج تأثيرٌ أكبر على مزيج عقود هيليكس، وكثافة رأس مالها، ومدى تعرضها لتقلبات أسواق النفط الفورية، وذلك في ظل تقييم المستثمرين لكيفية تأثير الأسطول المدمج وحجم الأعمال المتراكمة على جودة الأرباح المستقبلية.

مع ذلك، فإنه تحت وطأة الارتفاع الكبير في أسعار النفط، ينبغي على المستثمرين أن يدركوا أيضاً المخاطر التي قد تواجهها الأصول المعرضة لتقلبات الأسعار الفورية، والتي قد تستمر في مواجهة انخفاض مطول في الاستخدام وضغوط على الأسعار إذا...

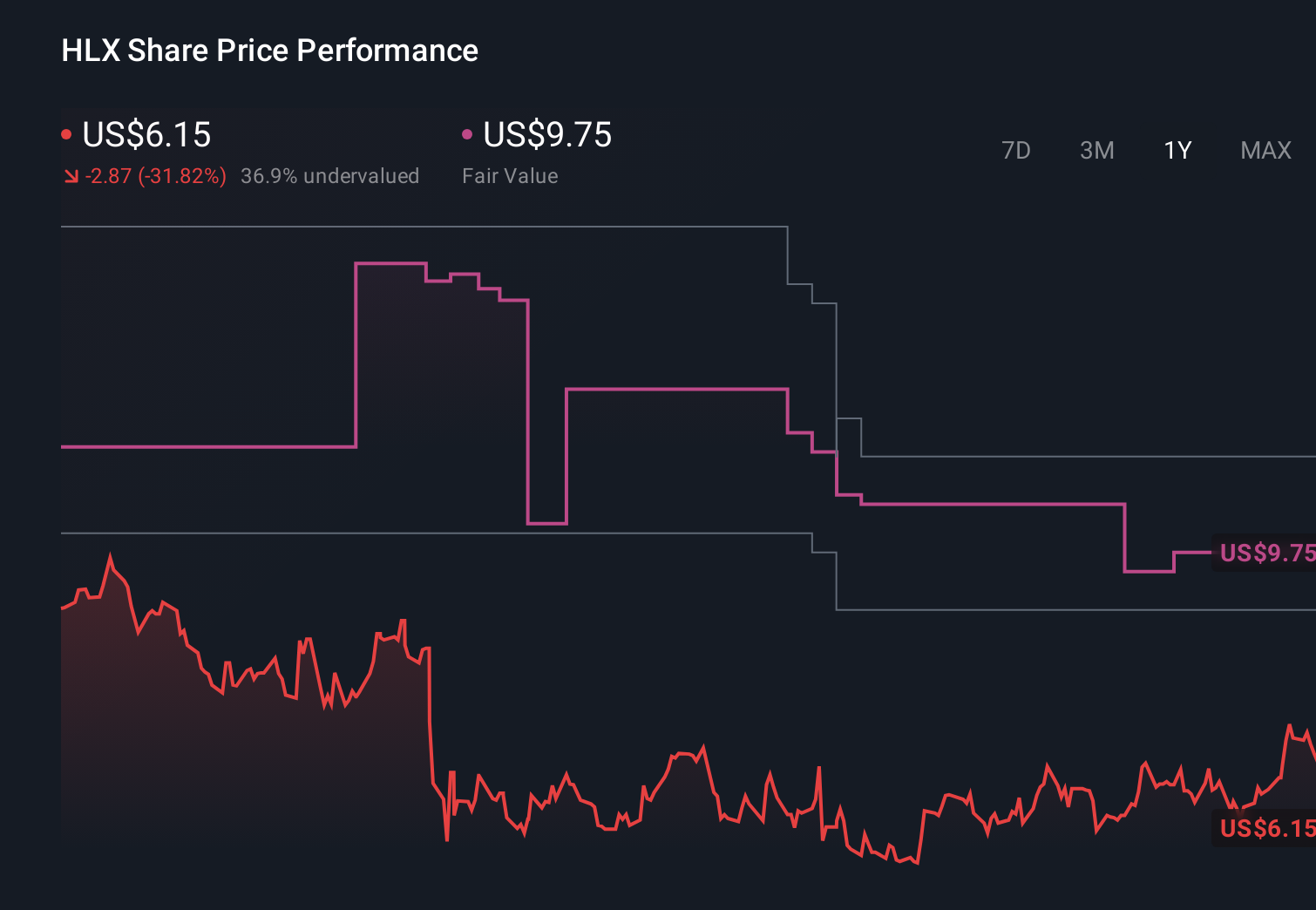

تتوقع مجموعة Helix Energy Solutions Group تحقيق إيرادات بقيمة 1.4 مليار دولار وأرباح بقيمة 103.0 مليون دولار بحلول عام 2028. ويتطلب ذلك نموًا سنويًا في الإيرادات بنسبة 2.9٪ وزيادة في الأرباح بنحو 52.9 مليون دولار من 50.1 مليون دولار اليوم.

اكتشف كيف أن توقعات مجموعة Helix Energy Solutions Group تؤدي إلى قيمة عادلة قدرها 9.75 دولارًا ، أي بانخفاض قدره 5٪ عن سعرها الحالي.

استكشاف وجهات نظر أخرى

كان بعض المحللين الأكثر تفاؤلاً يفترضون بالفعل إيرادات تقارب 1.4 مليار دولار أمريكي وأرباحًا تقارب 88 مليون دولار أمريكي بحلول عام 2029، لذلك بالمقارنة مع المخاوف الأساسية بشأن تقلبات السوق الفورية، فإنهم يخبرونك فعليًا بقصة مختلفة تمامًا عما يمكن أن تصبح عليه شركة Helix بعد صدمات مثل هذه الزيادة الحادة في أسعار النفط.

استكشف 5 تقديرات أخرى للقيمة العادلة لشركة Helix Energy Solutions Group - لماذا قد تكون قيمة السهم أقل بنسبة 32٪ من السعر الحالي!

كوّن رأيك الخاص

لا تكتفِ بمتابعة مؤشر الأسعار - تعمّق في البيانات وابنِ قناعة خاصة بك.

- تُعد تحليلاتنا التي تسلط الضوء على مكافأتين رئيسيتين وعلامتين تحذيريتين مهمتين قد تؤثران على قرارك الاستثماري نقطة انطلاق رائعة لأبحاثك حول مجموعة Helix Energy Solutions Group.

- يقدم تقريرنا البحثي المجاني عن مجموعة Helix Energy Solutions تحليلاً أساسياً شاملاً مُلخصاً في رسم بياني واحد - ندفة الثلج - مما يسهل تقييم الصحة المالية العامة لمجموعة Helix Energy Solutions بنظرة سريعة.

هل تبحث عن فرص بديلة؟

هذه الأسهم تشهد تحركات ملحوظة، وقد رصدها تحليلنا اليوم. سارعوا بالشراء قبل أن يرتفع سعرها.

- استغل دورة البنية التحتية للذكاء الاصطناعي الفائقة من خلال اختيارنا لأفضل 43 "خيارًا وأداة" في طفرة الذكاء الاصطناعي التي تحول الطلب القياسي إلى تدفق نقدي هائل.

- اكتشف الفرصة الكبيرة القادمة مع 27 سهمًا رخيصًا من النخبة يوازن بين المخاطرة والعائد.

- هذه التقنية قد تحل محل أجهزة الكمبيوتر: اكتشف 26 شركة تعمل على جعل الحوسبة الكمومية حقيقة واقعة .

هذا المقال من Simply Wall St ذو طبيعة عامة. نقدم تعليقاتنا بناءً على البيانات التاريخية وتوقعات المحللين فقط، باستخدام منهجية محايدة، ولا يُقصد بمقالاتنا أن تكون نصائح مالية. لا يُشكل هذا المقال توصيةً بشراء أو بيع أي سهم، ولا يأخذ في الاعتبار أهدافك أو وضعك المالي. نهدف إلى تزويدك بتحليلات طويلة الأجل مدفوعة بالبيانات الأساسية. يُرجى ملاحظة أن تحليلنا قد لا يأخذ في الاعتبار آخر إعلانات الشركات الحساسة للسعر أو المعلومات النوعية. لا تمتلك Simply Wall St أي أسهم في أي من الشركات المذكورة.