Is There Now an Opportunity in Ingram Micro After Recent Tech Demand Shift?

Ingram Micro Holding Corporation INGM | 24.25 | +4.03% |

- Wondering if Ingram Micro Holding could be a bargain right now? You are not alone, as investors continue to scout for undervalued opportunities in a rapidly changing tech sector.

- Ingram Micro Holding’s stock has seen some movement lately, rising 3.6% in the last week but dipping 2.9% over the last month. This hints at shifting sentiment and the potential for both growth and caution.

- Market attention has sharpened following industry updates about global supply chain improvements and renewed tech demand. Both of these factors have influenced recent price action. News coverage has also highlighted the company’s strategic partnerships and technology upgrades, adding important context for investors tracking momentum.

- The company earns a 4 out of 6 valuation score, suggesting it is undervalued by several common checks. However, is that the full story? Let’s walk through the different valuation approaches and keep an eye out for a perspective at the end that goes beyond the numbers.

Approach 1: Ingram Micro Holding Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's value by projecting future cash flows and discounting them back to today's value, reflecting the time value of money. For Ingram Micro Holding, recent analysis uses a 2 Stage Free Cash Flow to Equity model. In this approach, cash flow estimates are provided by analysts for the next five years, with longer-term projections extrapolated based on available data.

Currently, Ingram Micro Holding reported a last twelve months Free Cash Flow (FCF) of -$500.9 million. However, forecasts anticipate a significant turnaround, projecting FCF to grow to $653 million by 2028. Over the next decade, annual projections continue upward, reaching $926.9 million by 2035 according to available estimates and expert extrapolation. All figures are reported in US dollars.

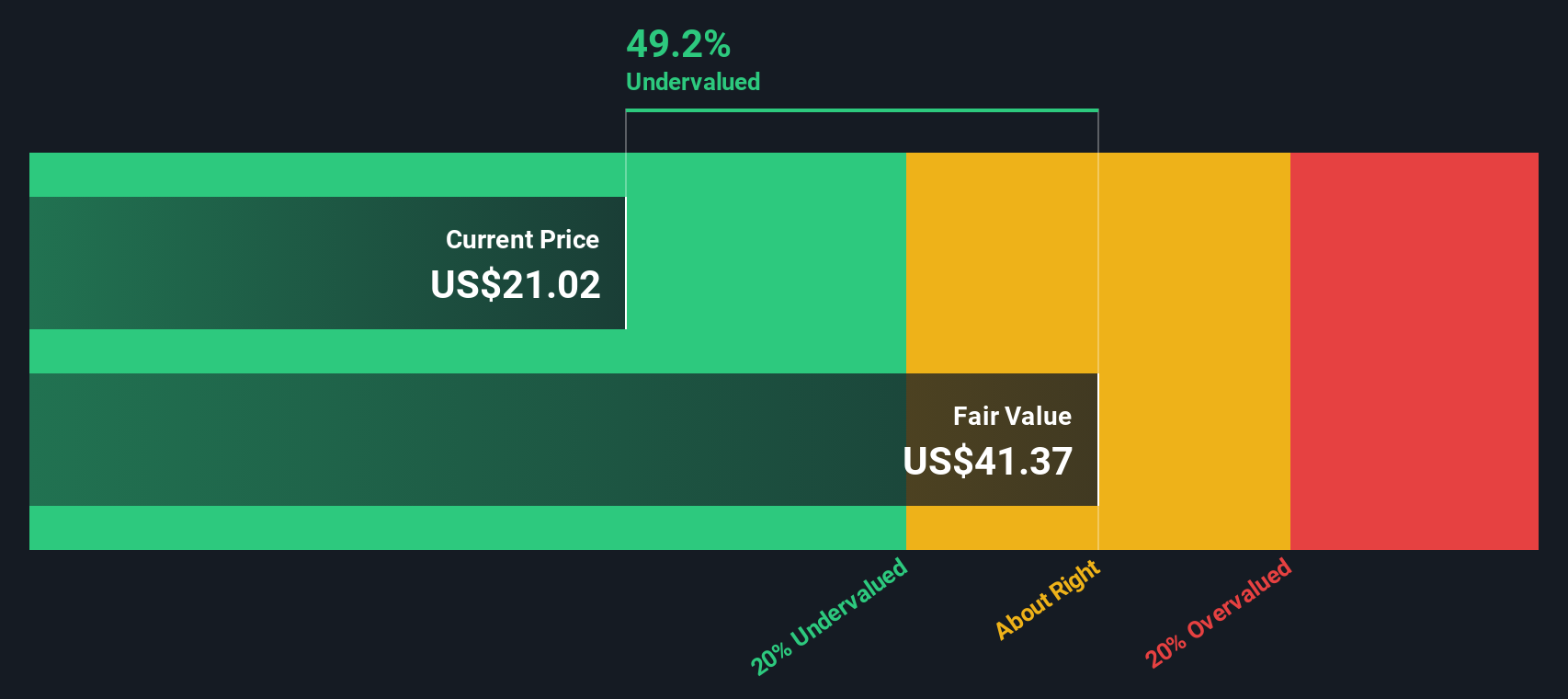

The DCF model calculates an intrinsic value of $37.29 per share. This represents a 42.7% discount to the stock's current price, meaning the stock appears to be substantially undervalued based on the fundamentals and future earnings potential outlined by these cash flow projections.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Ingram Micro Holding is undervalued by 42.7%. Track this in your watchlist or portfolio, or discover 933 more undervalued stocks based on cash flows.

Approach 2: Ingram Micro Holding Price vs Earnings

The Price-to-Earnings (PE) ratio is widely used for valuing profitable companies like Ingram Micro Holding, as it shows how much investors are willing to pay for each dollar of earnings. This measure is particularly relevant for companies generating stable profits, since it quickly highlights how the market weighs earnings potential against market price.

A company’s growth prospects and risk profile both influence what is considered a “normal” or fair PE ratio. Generally, higher growth rates or lower risk would justify a higher PE, while companies with slow growth or higher risk tend to trade at lower multiples. Comparing to industry and peer benchmarks gives additional context.

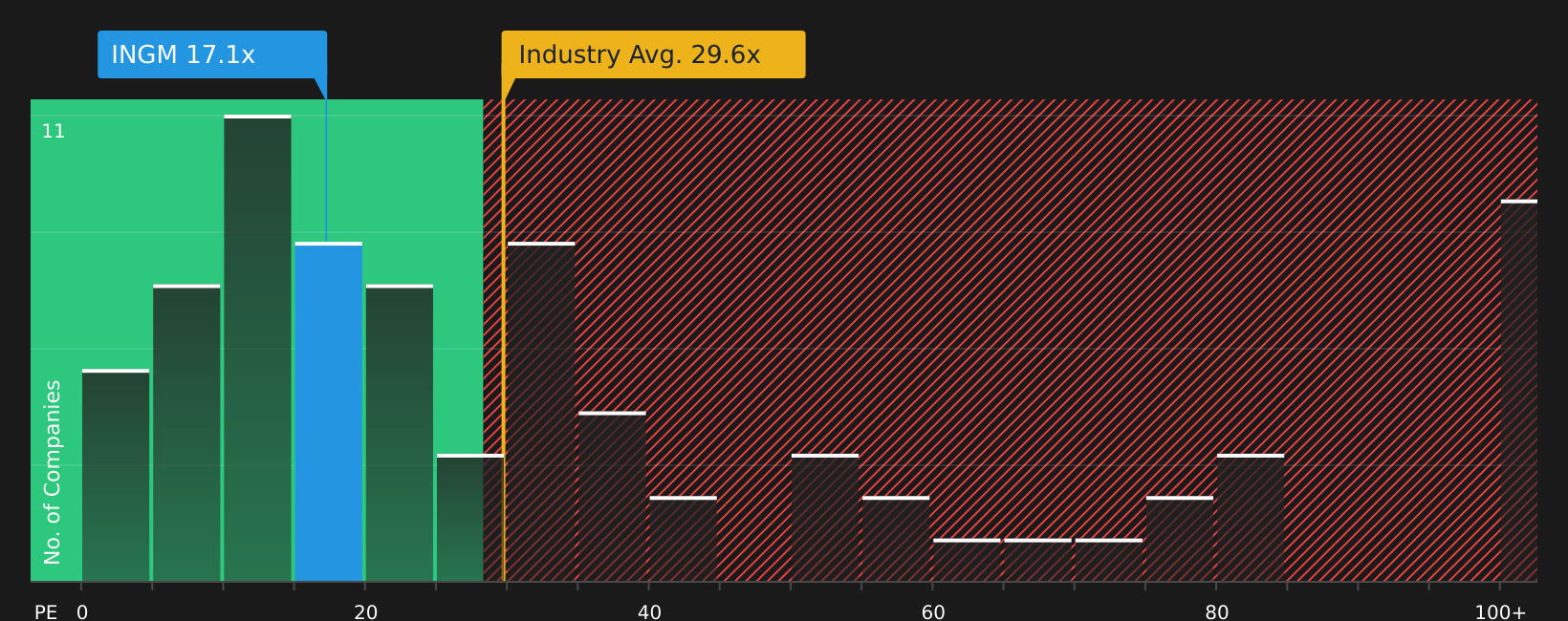

Currently, Ingram Micro Holding trades at a PE ratio of 17.33x. This sits just above the peer group average of 16.32x but is below the electronic industry average of 24.65x, implying that the stock is valued reasonably in context.

To refine the analysis, Simply Wall St’s “Fair Ratio” offers a tailored benchmark based on Ingram Micro Holding’s growth, risks, profits, and size. Unlike simple peer or industry comparisons, this proprietary metric reflects a more nuanced picture by considering the specific qualities of the company and its market position. For Ingram Micro Holding, the Fair Ratio is calculated as 32.83x.

Since the current PE of 17.33x is noticeably below the Fair Ratio of 32.83x, the stock appears undervalued on this basis. This suggests that, even after accounting for company-specific factors, Ingram Micro Holding could be trading at an attractive discount for investors.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1441 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Ingram Micro Holding Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is a simple yet powerful way to describe your unique view on a company, linking a story or perspective to your own financial forecast and a calculated fair value. Rather than relying solely on numbers like cash flows or PE ratios, Narratives connect the company’s journey and context with your predictions for future revenue, earnings, and profit margins.

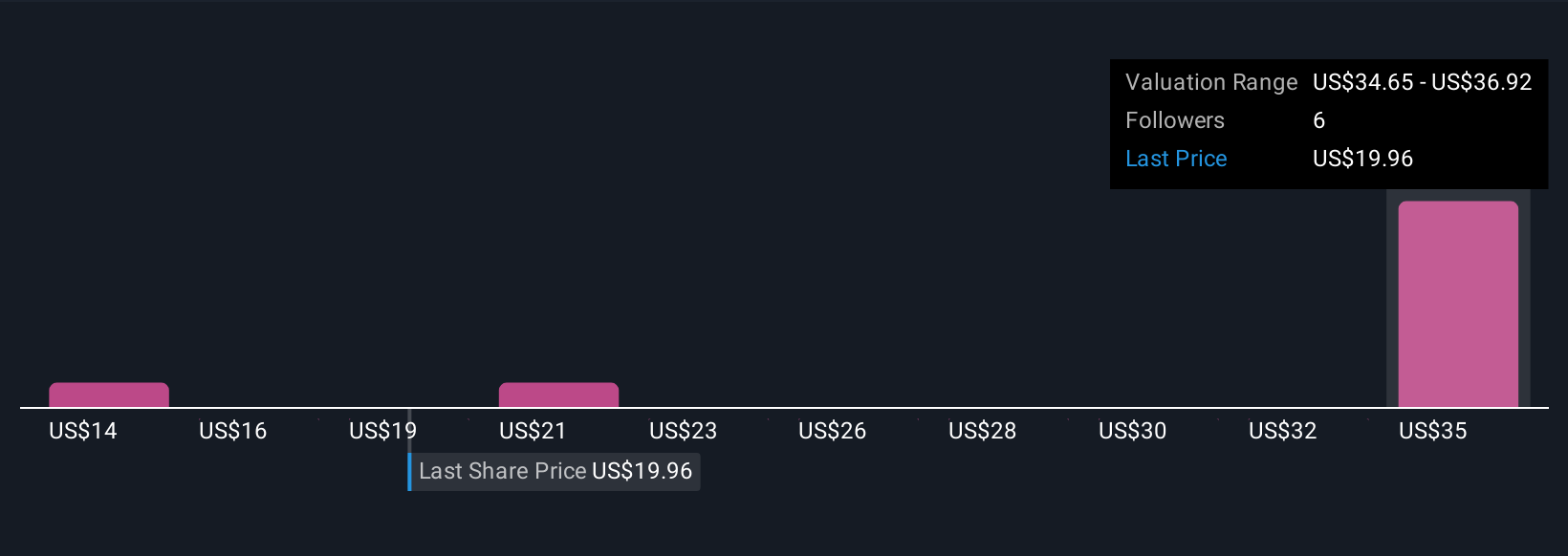

On Simply Wall St’s Community page, which is trusted by millions of investors, Narratives are an accessible tool to express your analysis, update your assumptions, and make smarter decisions. Narratives clearly compare a company's Fair Value (your estimate based on your forecast) with the current Price, helping you decide if now is the right time to buy or sell.

Best of all, your Narrative updates automatically when fresh news or earnings are released, so your outlook stays current. For example, some investors may see Ingram Micro Holding’s Fair Value as high as $42 per share given strong growth assumptions, while others might favor a more cautious view closer to $35, depending on their expectations and risk tolerance.

Do you think there's more to the story for Ingram Micro Holding? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.