Is Trinity’s Expanded Unsecured Credit Line Reshaping the Investment Case for Trinity Industries (TRN)?

Trinity Industries, Inc. TRN | 0.00 |

- On June 16, 2026, Trinity Industries, Inc. entered into a Third Amended and Restated Credit Agreement, replacing its prior facility with a US$600.0 million unsecured revolving line of credit that can be increased by up to US$300.0 million, includes up to US$100.0 million for letters of credit, and extends potential maturity to June 12, 2031, subject to its 7.750% senior notes due 2028 being repaid by April 15, 2028.

- The new facility, which currently has no borrowings and is priced off SOFR or CORRA plus a leverage-linked margin, strengthens Trinity’s access to flexible, unsecured liquidity while reinforcing lender confidence through subsidiary guarantees and financial covenants tied to interest coverage and net leverage.

- Next, we’ll examine how this expanded unsecured revolving credit capacity might influence Trinity’s investment narrative around earnings quality and balance sheet flexibility.

Capitalize on the AI infrastructure supercycle with our selection of the 50 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Trinity Industries Investment Narrative Recap

To own Trinity Industries, you need to believe in a steady, long-term role for rail in North American freight and in Trinity’s ability to convert that demand into consistent leasing and manufacturing earnings. The new US$600.0 million unsecured revolver improves financial flexibility, but it does not materially change the near term picture where the key catalyst remains execution on earnings guidance and the biggest risk is sensitivity to cyclical customer spending.

The credit agreement sits alongside Trinity’s 7.750% senior notes due 2028 and ongoing dividends, tying the capital structure more tightly to covenant tests around leverage and interest coverage. For shareholders watching earnings quality, this facility interacts directly with existing guidance and the company’s use of debt to support both its lease fleet and ongoing share repurchases.

Yet investors should also recognise how tighter leverage and interest coverage covenants could affect Trinity if freight markets or end market demand were to weaken unexpectedly...

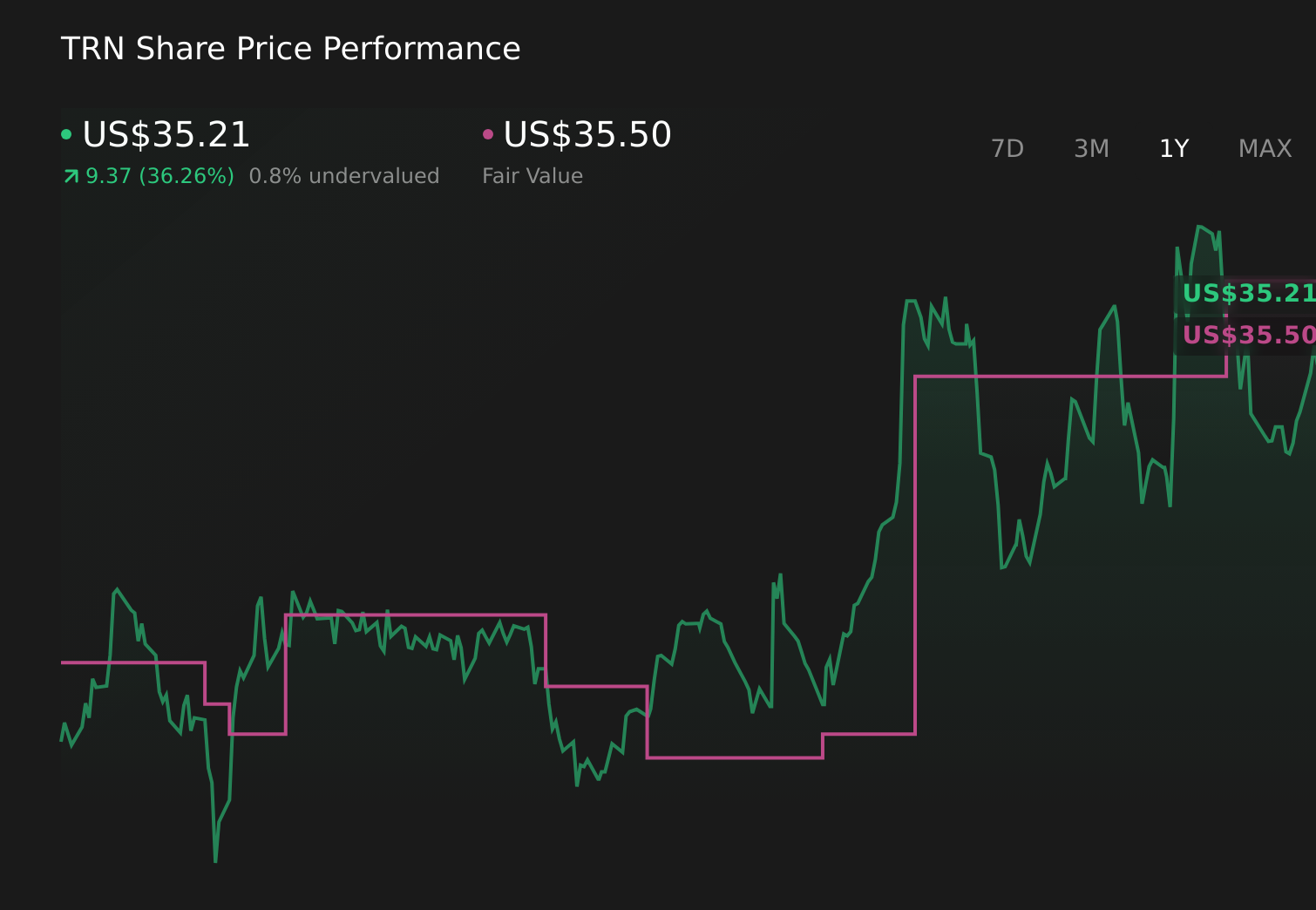

Trinity Industries' narrative projects $2.6 billion revenue and $118.9 million earnings by 2029. This requires 8.3% yearly revenue growth and a $143.4 million earnings decrease from $262.3 million today.

Uncover how Trinity Industries' forecasts yield a $35.50 fair value, in line with its current price.

Exploring Other Perspectives

Two members of the Simply Wall St Community currently see fair value for Trinity Industries between US$21.86 and US$35.50, illustrating a wide spread in expectations. When you set those views against Trinity’s reliance on cyclical energy and agriculture demand, it underlines why examining several independent takes on the company’s risk and return profile can be useful.

Explore 2 other fair value estimates on Trinity Industries - why the stock might be worth 39% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Trinity Industries research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Trinity Industries research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Trinity Industries' overall financial health at a glance.

Seeking Other Investments?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- This technology could replace computers: discover 29 stocks that are working to make quantum computing a reality.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Uncover the next big thing with 22 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.